Banking APIs and API Banking: How to Choose, Integrate, and Scale

July 30, 2026

Summary

Key takeaways

- Treat banking APIs as product infrastructure: orchestration, fallbacks, and consent matter more than a single endpoint demo.

- Classify APIs by access (public, partner, private, composite) and by job (identity, core, payments, cards, open banking)—then shortlist providers.

- Bank API integration succeeds when you own idempotency, webhooks, reconciliation, and provider abstraction—not only the first successful call.

- Open banking APIs and BaaS rails are different commercial and compliance models; do not buy one when you need the other.

- Score banking API providers on coverage, sandbox fidelity, SLAs, exit terms, and event quality before you compare logos.

Banking APIs are how modern financial products move money, prove identity, and read account data without rebuilding a bank. If you are choosing rails for a wallet, marketplace payouts, or a digital bank, the decision is not “do we need APIs?”—it is which bank API model, which providers, and which integration pattern will survive production. API banking is the default delivery shape for those products.

This guide consolidates bank connectivity as a product architecture choice: how banking apis work, which types of api to shortlist, how open banking rails differ from BaaS, and what bank api integration must include beyond a happy-path demo.

What a banking API and the operating model actually are

In banking products, APIs expose regulated financial capabilities as programmable interfaces. A bank api is the concrete contract (endpoints, auth, events). API banking is the business and delivery model of running products on those contracts.

Direct answer: APIs enable apps to create accounts, move funds, fetch balances, and run compliance checks in real time—while the licensed financial institution remains the system of record for money and regulatory duty.

| Term | Meaning for product teams |

|---|---|

| Banking API | Interface to a bank service (accounts, payments, cards, KYC hooks) |

| API banking | Delivering bank services through APIs as the primary channel |

| Open banking API | Consent-based third-party access to account/payment data under local rules |

| BaaS / embedded rails | Partner bank or platform APIs to embed bank services in a non-bank product |

Non-banks use banking apis to offer financial products without holding every license themselves. Banks use the same pattern to reach customers inside partner apps and to modernize internal channels.

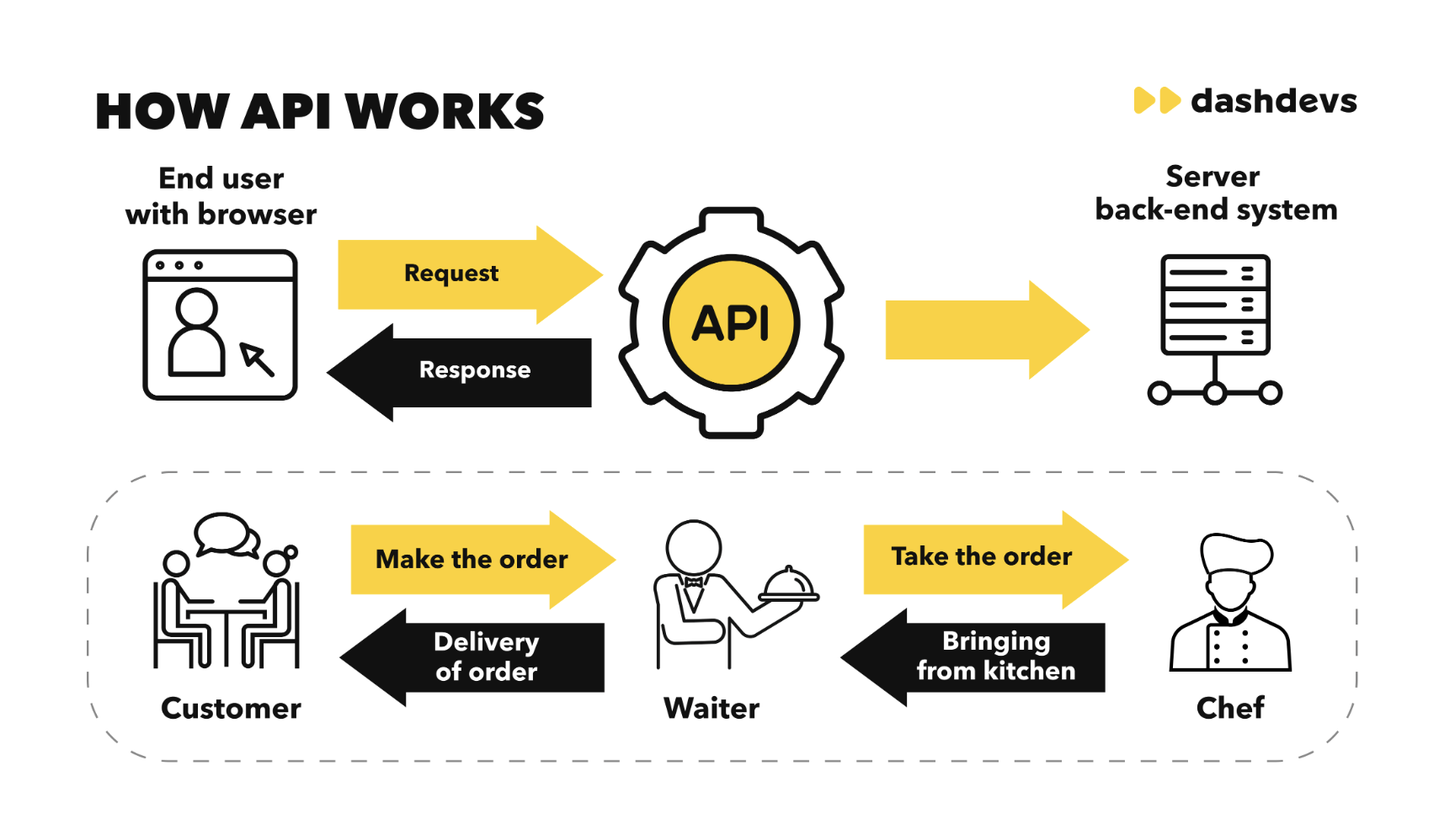

How banking APIs work in a live journey

Banking apis work as authenticated request–response and event flows—not as a single “pay” button.

- The product authenticates (API keys, mTLS, OAuth, or bank-issued credentials).

- The user consents where required (especially open banking).

- The app calls the bank api for a job: create account, initiate payment, fetch transaction data.

- The bank applies risk, ledger, and compliance rules.

- Webhooks or polling return status; your ledger reconciles outcomes.

Example: a wallet app is not a bank. The user taps “open account”; the app calls a licensed partner via banking API; the bank creates the account; the app shows success. Regulated posting stays on the bank side—your product owns UX, orchestration, and support.

Access models and protocols

Teams still ask for types of api catalogs; the useful split is access model first, protocol second.

By accessibility

| Type | Who can call it | Typical use |

|---|---|---|

| Public / open | Approved third parties under published rules | Open banking account/payment access |

| Partner | Contracted B2B clients | Payment gateways, co-branded products |

| Private / internal | Inside the financial institution | Channel apps, internal microservices |

| Composite | Orchestrates multiple calls as one | Onboarding or payment journeys that fan out |

By communication style (decision view)

- REST + JSON — Default for most banking api providers and open banking endpoints; easy tooling, broad talent pool.

- SOAP / XML — Still present in enterprise cores; plan adapters if you inherit it.

- GraphQL — Useful for flexible reads in portals; less common as the regulated edge.

- gRPC — Strong for internal service-to-service latency; rarely the public bank edge.

- Webhooks — Mandatory for real time transaction status; design idempotent consumers.

Pick protocols for the edge you must integrate; do not force GraphQL onto a PSD2-style open banking api that ships as REST.

Banking API landscape by product job

Successful products coordinate several banking apis as workflows—not one mega-endpoint.

| Job | What the API covers | Decision note |

|---|---|---|

| Identity & verification | KYC/KYB, AML screening, biometrics | Multi-vendor with fallback reduces onboarding drop-off |

| Core / ledger | Accounts, balances, posting | Rarely expose raw core to the mobile app |

| Payments | Payouts, A2A, cards settlement hooks | Need retries, idempotency, reconciliation |

| Cards | Issue, freeze, limits, tokenization | Product rules live above the issuer API |

| Open banking & data | Account data, payment initiation | Consent and re-auth dominate UX |

Core choices sit next to top core banking systems. Payment acceptance often pairs with payment gateway integration services. For consent-based data and pay-by-bank, start from open banking API development and compare open banking providers.

Open banking apis are not the same as a full BaaS stack. Open banking reads or initiates with customer consent; BaaS issues products under a partner license. Buying the wrong model wastes a quarter.

Standards and compliance constraints

Banking api standards are corridor-specific: UK Open Banking specifications, Berlin Group-style PSD2 interfaces, CDR in Australia, and market-led bank APIs in the US. Your integration plan must name the standard and the certificates (for example QWAC/QSEAL where required).

API banking solutions that ignore consent management, retention, and audit trails fail the first compliance review—even if the sandbox looks green. Strong banking api integration plans treat consent and audit as first-class requirements, not post-go-live tickets.

Why banks and fintechs invest in bank APIs

For banks: reach customers in partner channels, reduce branch-centric friction, and monetize infrastructure via partners—without owning every UX. That is API banking as distribution, not only as engineering.

For fintechs: launch bank services without becoming a bank, embed finance in non-financial journeys, and iterate product while the license sits with a partner.

Budget reality still includes licensing and capital when you own the institution—see how much does it cost to start a bank—but many products only need bank api access, not a full charter.

Customer experience improves when account balance, transaction data, and financial information update in real time across products and services. That is data sharing with purpose—not open data for its own sake.

How to choose banking API providers

Selecting banking api providers is a coverage and operations decision. Score them the same way you score critical vendors.

| Criterion | What good looks like | Red flag |

|---|---|---|

| Coverage | Live banks/rails for your corridors | “Roadmap” sold as production |

| Sandbox fidelity | Production-like errors and webhooks | Happy-path only |

| Security | OAuth/mTLS, least privilege, audit logs | Shared credentials, unclear key rotation |

| Reliability | Published SLA, incident history | Silent downtime |

| Docs & versioning | Clear deprecation policy | Breaking changes without notice |

| Pricing | Units that match your economics | Surprise overage at scale |

| Exit | Data/connection portability | Irreversible customer re-linking |

Also weigh protocol fit, rate limits, error model, and support quality. For stack-level planning, use DashDevs’ fintech API integrations guide. Delivery partners should look like top banking software development companies on evidence—not on slide count.

Bank API integration: what production requires

Banking api integration is finished only when these are true in production:

- Encryption in transit (and at rest for stored tokens/PII)

- Endpoint and environment separation (sandbox vs live)

- Rate limiting and backoff that match provider quotas

- Idempotent writes for payments and account actions

- Webhook signature verification and replay protection

- Consent management and revocation where open banking applies

- Reconciliation between your ledger and bank statuses

- Observability: latency, error codes, and SLA burn

Connectivity that skips reconciliation creates silent money risk. Banking API integration that skips fallback creates outage risk.

Production patterns that hold

- Provider abstraction so you can swap a KYC or payout vendor without rewriting journeys

- Fallback and retry for high-risk dependencies

- Stateful orchestration so onboarding and funding are resumable

- Monitoring for reconciliation breaks—not only HTTP 500s

API-first platforms: Fintech Core and live programs

Fintech Core packages modular banking architecture as reusable platform building blocks—ledger, orchestration, and provider adapters—so teams do not rebuild the same bank api integration for every product.

In programs such as Dozens / Project Imagine, the hard problem was not “calling APIs,” but orchestrating identity, payments, and compliance so a single vendor outage did not block users. That is the difference between a demo and an operating financial institution-grade product.

When you need white-label shells around those rails, keep module boundaries honest: APIs first, brand second.

Decision checklist before you commit

| Question | If unclear, pause |

|---|---|

| Which jobs need a bank api this quarter (AIS, PIS, ledger, cards)? | Scope before RFP |

| Open banking vs BaaS vs private partner API? | Wrong model wastes months |

| Who owns reconciliation and incidents? | Name a team |

| Can we swap a provider in 90 days? | Fix contracts and abstraction |

| Do sandbox scripts include soft declines and consent expiry? | Demand evidence |

Banking APIs create advantage when they are orchestrated as product infrastructure. The operating model is still API banking; banking api providers are interchangeable only if you designed them that way. Build for failure, consent, and audit—and the customer experience will follow.

Share article