Best Online Banking Platforms in 2026 for Banks and Fintechs

A CEO-level guide to online banking software: what it is, how it differs from core banking and BaaS, which platforms to evaluate, and how to choose without vendor lock-in.

March 17, 2026

Summary

Online Banking in a nutshell:

- An online banking platform is the digital software layer that lets banks and fintechs deliver account access, payments, onboarding, and self-service through web and mobile channels.

- It is not the same as core banking, though it typically connects to a core banking system.

- The strongest online banking platforms in 2026 are modular, API-first, mobile-ready, and integration-friendly.

- White-label banking platforms speed up launch, but they vary widely in customization depth.

- Buyer decisions should be based on architecture flexibility, compliance readiness, integration options, and long-term scalability.

- DashDevs is best suited for teams that want launch speed without being trapped in a rigid vendor box.

Online banking has a naming problem. When a buyer says “online banking platform,” they might mean:

- the customer experience layer (web/mobile UI + basic account features),

- the digital banking servicing layer connected to a core,

- a white-label launch platform that comes with a ready product,

- or a vendor ecosystem for connectivity: onboarding, payments, cards, support tooling, and account servicing.

Vendors don’t help here. Many deliberately blur these boundaries in marketing — because “platform” sounds bigger than “product,” and bigger usually sells better.

This article does three things:

- Clarifies what an online banking platform actually is (and isn’t).

- Compares the leading online banking platform options to evaluate in 2026.

- Gives you a practical selection framework based on architecture, compliance readiness, integration flexibility, and scalability — not just a feature checklist.

What is an online banking platform?

This section is the foundation. If your team defines “platform” differently from a vendor, you will compare the wrong things, buy the wrong thing, and pay for it later through rework, compliance debt, or vendor lock-in.

Online banking platform definition

An online banking platform is the software infrastructure that enables customers (and business users) to access and manage banking products digitally — through web and mobile interfaces — with the workflows, integrations, security controls, and operational tooling required to run it in production.

For a fintech CEO or a bank executive, here’s the framing that matters:

- The platform is not “the app.” The app is one channel. The platform is the system that makes the channel safe, compliant, and scalable.

- The platform is not the core. The platform reads and writes to the core. It doesn’t replace the ledger that is the system of record.

For the cleanest explanation of core banking, start with what is core banking?.

At a business level, the platform is where your unit economics and risk posture are shaped. If onboarding is slow, CAC is wasted. If ops tooling is weak, support headcount grows linearly. If integrations are rigid, expanding to a new market becomes a program instead of an iteration.

For a practical map of what “integration-friendly” actually means in fintech (KYC, payments, open banking, fraud, cards, support tooling), see the essential fintech API integrations for a scalable and compliant financial platform.

What an online banking platform typically includes

Think of this as the minimum set of capabilities that turns “internet banking software” into an operating system you can actually run in production — including the parts your customers never see but your compliance and ops teams depend on.

In real deployments, “online banking software” tends to include:

- Account access: profiles, accounts, balances, statements

- Transaction history: categorization, search, receipts, exports

- Transfers and payments: internal transfers, bank transfers, scheduled payments, limits

- Card controls: freeze/unfreeze, PIN, virtual cards, spend controls, disputes (where applicable)

- Onboarding and authentication: registration, identity checks, MFA, device binding, session control

- Alerts and notifications: push, email, SMS, risk alerts, payment status updates

- Support and self-service: in-app support, knowledge base, ticketing, “lost phone/card” flows

- Admin / operations tooling: customer service console, compliance case management, audit trails

At regulated scale, “admin tooling” is not optional. It’s where the unit economics of customer service and compliance either work — or don’t.

Here’s a practical way to separate “feature list” from “platform readiness”:

| Layer | What it includes | Why it matters commercially |

|---|---|---|

| Customer experience | Web + mobile UI, self-serve journeys | Conversion, retention, trust |

| Workflow + orchestration | Onboarding, payments, limits, approvals | Speed of change, differentiation |

| Integrations | Core, payments, cards, KYC/AML, fraud, CRM | Expansion speed, switching cost |

| Operations tooling | Support console, case management, audit trails | Cost-to-serve, compliance productivity |

| Security + compliance | IAM, logging, evidence, reporting | Regulatory survivability, fraud reduction |

When you turn this into an implementation plan, the fastest way to reduce expensive rework is to align scope, licensing path, and integrations before engineering starts. That’s exactly what DashDevs’ product discovery service is built for.

Online banking platform vs online banking app

This is the most common buying mistake: teams benchmark UI and assume they’re benchmarking the platform. In regulated finance, that’s like test-driving the dashboard and ignoring the engine.

An online banking app (mobile or web) is the UI: the screens your customers touch.

An online banking platform includes:

- the workflows (onboarding, payments, disputes),

- the orchestration (how systems and vendors are stitched together),

- the security architecture (roles, tokens, auditability),

- the integrations (core, cards, payments, KYC/AML, CRM),

- and the operating model (back office tools, compliance flows, support queues).

In other words: the app is what customers see; the platform is what makes it work when regulators, fraudsters, outages, and growth show up.

Buying only an “app” still leaves you needing to build a platform; buying a platform (or a solid foundation) lets you ship channels faster, run operations with less headcount, and keep the option to evolve your vendor stack over time.

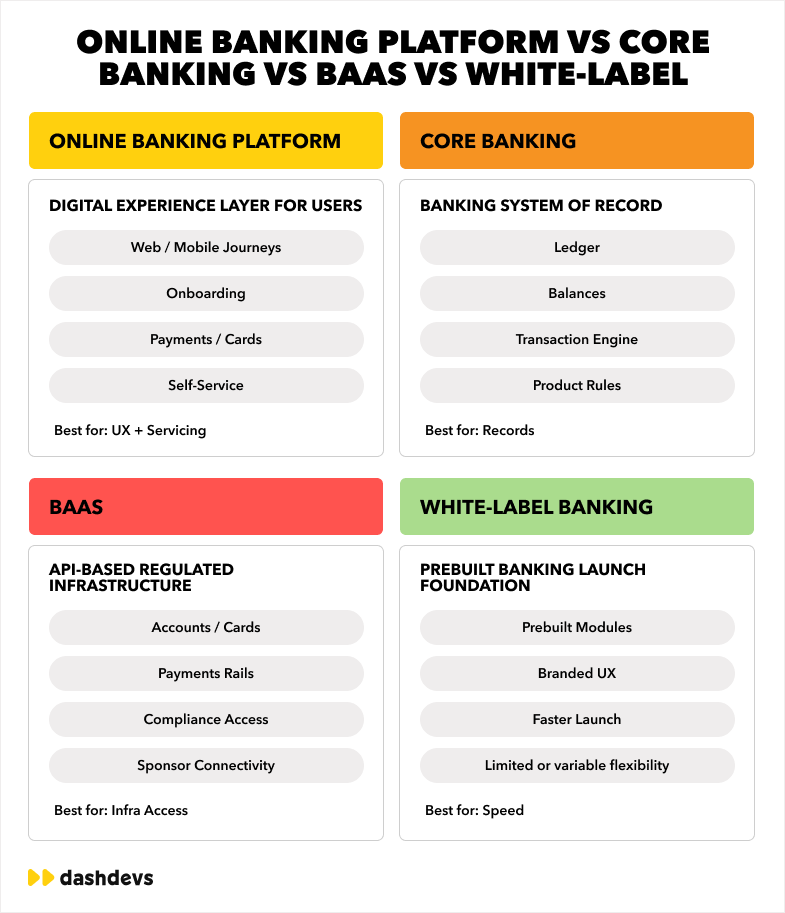

Online banking platform vs core banking vs BaaS vs white-label banking

These terms are often thrown into the same bucket. For a buyer, they represent different “centers of gravity” in the stack — and each one implies a different cost structure, control model, and timeline.

Core banking

Core banking is the system of record: the ledger, balances, account lifecycle, and product rules. It’s where truth lives. If you want a business-friendly view of what core banking really does (and why it’s not a UI decision), read what is core banking?.

For banks, core banking is non-negotiable. For fintechs, core banking is either something you operate (rare early) or something you consume via a bank/BaaS partner (common early). Either way, your digital experience inherits its constraints: real-time vs batch, limits flexibility, reporting depth, and how easy it is to reconcile issues.

Treat core as “truth infrastructure,” not a UI component — because the cost of being wrong here compounds for years.

Online banking platform

The online banking platform is the digital experience and servicing layer connected to the core and third parties. It orchestrates journeys, enforces access control, handles integrations, and provides the self-service experience.

This is where most differentiation happens in 2026: onboarding conversion, payment UX, card controls, business banking entitlements, and cost-to-serve. It’s also where most teams discover their first serious bottleneck: “We can’t change that because the vendor stack is hardwired.”

Think of core as the “record of truth,” and the online banking platform as the “system of action.”

BaaS (Banking-as-a-Service)

BaaS is licensed access to banking rails via APIs. It’s often the fastest way for fintechs to launch, but it comes with infrastructure constraints and dependency. If you’re building embedded finance, it’s easy to confuse “BaaS” with “online banking platform” — but they’re not interchangeable.

For a clean separation of these concepts, listen to Fintech Garden podcast — episode 108 (it’s one of the few explanations that doesn’t turn into vendor marketing).

In Episode 108 the framing is blunt and useful:

“Instead of building a bank from scratch (which requires licenses, regulatory approvals, and heavy infrastructure), companies can partner with BaaS providers to access pre-built banking infrastructure.” — Fintech Garden episode 108

BaaS can be the fastest path to market, but it is also a long-term dependency decision — evaluate it like infrastructure, not like a SaaS tool.

White-label banking platform

A white-label banking platform is a prebuilt foundation that speeds up launch. The important nuance: “white-label” varies wildly.

Some vendors offer branding and configuration only (fast, but rigid). Others provide a modular foundation you can extend without re-platforming (slower than “instant,” but far more survivable at scale).

The business trade-off is simple: white-label can reduce initial build cost and timeline, but some models increase lifetime cost by limiting provider choice, workflow customization, and operational automation.

White-label is a spectrum — treat flexibility as an architecture property, not a marketing promise.

Why buyers confuse these categories

The confusion is structural: each category touches the customer experience, and vendors often bundle components to sell “the whole bank.” That’s why buyers end up comparing incompatible options in the same short list.

Because many vendors deliberately blur them.

“Platform” is used as a catch-all for:

- digital channels,

- core banking,

- payments infrastructure,

- and sometimes the license itself.

As a buyer, the only way to cut through this is to ask one question:

What parts of this stack do we control — and what parts do we rent?

One more question I recommend using in vendor calls:

“If we need to switch KYC, issuer, or bank connectivity, what breaks — and how much work is it?”

When a vendor can’t answer those questions clearly, you’re not evaluating a platform — you’re evaluating a black box.

Why demand for online banking platforms is rising

Demand is not rising because banks suddenly love “digital transformation.” It’s rising because mobile-first behavior, new rails, and new fraud/compliance expectations have made legacy digital layers uneconomical to run and too slow to evolve.

Customer expectations became mobile-first

For customers, the “bank” is now the mobile experience — with web as a secondary channel. Your online banking platform is the engine behind both channels, and customers judge it on speed, reliability, and trust.

From a business lens, this pushes three pressures onto the platform:

- Always-on availability: outages and delayed balances are instant trust erosion.

- Real-time servicing: instant notifications, card controls, and payment status visibility are baseline expectations.

- Shorter time-to-first-value: onboarding must get customers to their first successful action quickly (funding, transfer, card usage), or CAC leaks.

Mobile-first expectations don’t just change UX — they change your architecture and ops model, because the “branch workaround” is gone.

Legacy bank interfaces are too slow to evolve

Legacy digital layers are often tied to legacy cores, legacy release processes, and legacy operating models. That’s why many banks modernize the experience layer first, before touching core replacement programs.

In practice, the issue isn’t “banks can’t build features.” It’s that they can’t change safely and frequently. When releases become quarterly, competitors ship weekly. When onboarding is brittle, compliance teams push back on change. That creates a loop: slower releases → higher risk per release → even slower releases.

Modernizing the online banking platform layer is often the fastest way to regain product velocity without taking core migration risk on day one.

Fintechs need faster launch without sacrificing flexibility

Fast launch is a survival requirement — but so is the ability to change vendors, expand markets, and evolve onboarding and fraud controls. The real challenge is avoiding the “fast MVP, slow everything else” trap.

This is where Episode 122’s “complexity vs complication” lens becomes practical. Complexity is unavoidable as you add rails, markets, and products. Complication is optional — and it’s often created by rigid vendor stacks and brittle integrations.

“As fintechs evolved, their once-simple models became multi-layered ecosystems.” — Fintech Garden episode 122

Choose a platform that makes change cheaper over time — not more expensive.

Open banking and third-party ecosystems increased integration pressure

More rails, more providers, more ecosystems: open banking, card issuing, KYC vendors, fraud engines, CRM, analytics. That integration pressure is exactly why modern internet banking platform designs are API-first and adapter-based.

Business insight: integrations aren’t just “technical work.” They are commercial optionality. The ability to add a second bank partner, introduce a new payment rail, or swap an IDV provider is what lets you renegotiate terms and expand geography without a rewrite.

A flexible integration layer is what turns ecosystem complexity into leverage rather than overhead.

Compliance, onboarding, and fraud controls now need to be built into digital journeys

In 2026, compliance isn’t something you bolt on after launch. It’s part of the product. A useful reference is from digital onboarding to daily banking, because it explains why onboarding is a trust and unit-economics problem, not just a “KYC step.”

Operational reality: onboarding is where compliance, conversion, and fraud collide. The platform must support risk-based routing, evidence capture, and manual review queues for edge cases — otherwise you either block good customers or onboard bad ones.

One hard number worth remembering: according to Innovatrics, 63% of users abandon digital bank onboarding when the process is too complicated or time-consuming. That’s not just a UX problem — it’s wasted acquisition spend.

The platforms that win are the ones that make compliance and speed compatible, not adversaries.

Demand drivers at a glance

| Driver | What changes for buyers | What changes for the platform |

|---|---|---|

| Mobile-first expectations | Lower tolerance for outages | Real-time events, resilient ops, observability |

| Vendor ecosystem growth | More providers and rails | Orchestration + adapters, clean seams |

| Compliance pressure | More evidence and audit demands | Logging, case management, policy-driven flows |

| Business banking growth | More multi-user workflows | Entitlements, approvals, bulk ops, reconciliation |

Demand is rising because online banking is now the primary product surface — and buyers need systems that scale operationally, not just aesthetically.

Who actually needs an online banking platform?

For business owners, the point is simple: you need an online banking platform whenever digital channels are not just “access,” but the primary way customers onboard, transact, and get support. Different buyer types need different platform strengths — and that’s where many RFPs go wrong.

Licensed digital banks

For licensed institutions (or those becoming licensed), the online banking platform is your control plane: customer journeys, support workflows, and operational evidence. You’re not just shipping software — you’re shipping a regulated operating model that must be auditable under pressure.

For banks (or teams becoming banks), the online banking platform is the customer-facing operational layer. The question isn’t “do we need it?” but “how do we keep it modular so we can evolve without breaking compliance?”

Licensed institutions should prioritize auditability, resilience, and change control — because your platform will be judged under stress, not in demos.

Neobanks and challenger banks

Neobanks win (or lose) on velocity and product clarity. That speed only survives if your platform can orchestrate vendors reliably and your ops team can handle edge cases without escalating everything to engineering.

Neobanks need fast iteration and strong vendor orchestration. If you’re building under a sponsor bank or EMI model, the online banking platform is what prevents your vendor stack from turning into technical debt. If you’re in that lane, see how to start a neobank: regulatory and technology roadmap.

Optimize for “launch speed + switching cost” as a combined metric; it’s not enough to ship, you need the ability to evolve.

EMIs and payment institutions

From a customer perspective, EMIs are treated like banks. From a regulatory perspective, you still need tight controls, evidence, and operational maturity. That tension shows up inside the platform.

EMIs often ship “banking-like” products (accounts, cards, payments) without being banks. The online banking platform becomes the place where onboarding, fraud controls, and operational workflows have to be mature — because the product will be treated like a bank by customers even if the license is different.

EMIs should prioritize fraud operations, dispute handling, and monitoring tooling early — that’s where cost-to-serve usually spikes first.

Corporate banking and SME banking providers

Business banking is a different sport. The buyer is not just a human user — it’s a finance process with approvals, roles, and audit requirements. That’s why “best business banking platforms” is a separate intent category.

Business banking raises the bar: multi-user roles, approvals, bulk payments, reconciliation views. Many “best online banking platform” lists ignore this, then buyers get surprised six months later.

Teams planning to serve SMEs should evaluate entitlements and approvals from day one — retrofitting them later is expensive.

Fintechs adding banking features (embedded finance)

Embedded finance teams often think they don’t need an “online banking platform” because the banking UI is secondary. That’s true — until a dispute, chargeback, or compliance request forces you to produce evidence and audit trails quickly.

When banking sits inside a marketplace or SaaS product, the online banking platform may be “invisible,” but the same requirements still apply: identity, entitlements, auditability, and operational support tooling.

Embedded finance products need platform-grade operations even when the UI is minimal — otherwise the “banking feature” becomes an operational liability.

Regional banks modernizing customer experience without replacing the core immediately

This is one of the most pragmatic modernization paths in 2026: modernize what customers touch (and what ops teams run) while minimizing core migration risk.

This is one of the most practical paths: modernize the experience and orchestration layer first, and run it against the existing core while you de-risk longer-term core modernization.

Done well, this gives immediate CX wins and future-proofs your core replacement decision instead of forcing it.

Buyer types and what to optimize for

| Buyer type | Primary goal | What to optimize for first |

|---|---|---|

| Licensed bank | Modernize channels safely | Auditability, resilience, integration with existing core |

| Neobank/challenger | Ship and iterate fast | Orchestration, onboarding conversion, switching cost |

| EMI / PI | Operate “bank-like” reliably | Fraud ops, disputes, monitoring, evidence trails |

| SME/corporate banking | Support finance workflows | Entitlements, approvals, bulk payments, reconciliation |

| Embedded finance | Add banking features without distraction | Compliance-ready workflows + minimal UX friction |

You don’t choose a platform for “features.” You choose it for the operating model you need to run.

Once you’re clear on buyer type, the rest of the evaluation becomes dramatically simpler — you stop optimizing for generic checklists and start optimizing for fit.

Types of online banking platforms in the market

Before you compare vendors, compare categories. “Platform” can mean white-label launch product, enterprise digital engagement suite, or custom build. The category determines timeline, cost, and what you will (and won’t) be able to control later.

White-label digital banking platforms

White-label platforms exist because time-to-market is a real constraint. The strategic question is not “white-label or not,” but “how much of our future are we renting?” and “what happens when our roadmap diverges from the vendor’s defaults?”

Best when you need speed, want a proven foundation, and you’re willing to trade some flexibility for time-to-market — with the big caveat that white-label depth varies. If you want a broader market view on white-label, see the top white-label digital banking software solutions in 2026.

When you choose white-label, define your “escape plan” upfront — switching providers, extending workflows, and owning the parts that become differentiators.

Core-bundled banking platforms

Core-bundled platforms can reduce integration burden early, but they also increase dependency. If your bank partner, issuer, or KYC vendor is bundled, it’s harder to renegotiate terms or swap later without re-platforming.

These can be useful when you want a single vendor relationship — but they can also create deep dependency. It’s a trade: fewer integration points today, fewer degrees of freedom tomorrow.

Bundled can be a good choice when your operating model is standard and stable; it’s risky when you expect rapid product evolution.

Custom-built digital banking platforms

Custom builds make sense when the platform is your moat — not a commodity layer. This is often true in business banking and niche fintechs, where workflow design is the product and “out-of-the-box” becomes a ceiling.

Highest flexibility and differentiation, but more complex and slower. This makes sense when digital banking is your moat — not just a channel.

Custom is more expensive upfront, but can be cheaper long-term if it prevents lock-in and reduces manual operations at scale.

Modular platforms with reusable blocks

This is the category many scale-minded fintechs actually want: start with a foundation, then extend based on traction. Modularity is how you avoid “rewrite at Series B” while still launching fast.

The middle ground most scale-minded fintechs want: launch speed plus extensibility. Modular doesn’t mean “microservices everywhere.” It means your system has clear seams: adapters, orchestration, and the ability to evolve parts without rewriting everything.

The real test of modularity is provider switching and adding new markets without breaking core flows.

Online banking platforms for retail vs business banking

This is worth stating explicitly: retail and business banking have different “must-haves.” Mixing them in one evaluation produces bad decisions and missed requirements.

Retail banking platforms optimize for:

- onboarding conversion,

- speed and trust,

- everyday money movement.

Business banking platforms must additionally handle:

- entitlements and role hierarchies,

- approvals and policies,

- bulk operations and reconciliation,

- and more complex customer support workflows.

For SME or corporate clients, treat this as a separate product class — not a “nice-to-have later.”

Teams serving both retail and SMEs should design entitlements and approvals early — it’s far harder to bolt them onto a retail-only foundation later.

Selecting the right platform type is about choosing your constraints consciously; if you pick the wrong category, you will either overpay for enterprise complexity or underbuy and hit limits the moment you scale.

How we evaluated the best online banking platforms in 2026

I’m not going to pretend there’s a single “top 10 digital banking platforms” list that fits everyone. There isn’t.

So we use a buyer-aligned evaluation framework.

Customization depth

Can you change onboarding flows, approvals, limits, and product rules — or only colors and logos?

Business lens: customization depth determines whether you can build a differentiated product, or whether you’re running “the vendor’s product” with your logo on top. If you’re aiming for a niche (SME finance ops, cross-border workers, youth banking), shallow customization becomes a strategic ceiling.

Don’t ask “can we customize?” Ask “what can’t we customize without vendor work?”

Time to launch

How fast can you go live with a compliant MVP that survives real usage (not a demo)?

Time-to-launch is not “screens shipped.” It’s “first customers onboarded successfully, with support and compliance workflows running.” Treat vendor timelines as marketing until you see the integration plan and operational readiness checklist.

The fastest launch is the one that doesn’t require rebuilding the first month after go-live.

Mobile and web readiness

Is it truly mobile-first, or is mobile a wrapper around web flows?

Mobile-first matters because it changes friction. Small UX differences create large conversion differences in onboarding. If your mobile flow is a wrapper, you’ll pay for it in drop-off rates and support tickets.

Evaluate key journeys on mobile first — not desktop — because that’s where customers decide.

Integration flexibility

Can you integrate your own KYC/AML, open banking, card issuing, fraud, and CRM stack without rewriting the platform?

Integration flexibility is also a negotiation power. If switching providers is hard, you accept the pricing and terms you’re given. If switching is easy, you can optimize commercial contracts over time and expand coverage without re-platforming.

Integration flexibility is a business lever, not a technical preference.

Security and compliance support

Does it provide auditability, access control, and operational workflows that compliance teams can actually use?

Compliance teams don’t want “a secure system,” they want a system that produces evidence quickly and consistently. If your platform can’t show who did what, when, and why, you’ll end up building shadow processes outside the product.

Auditability is the difference between scalable compliance and manual compliance.

Ability to work with existing core/vendors

Can it sit on top of your current core while you modernize, or does it force a rip-and-replace program?

This matters most for banks: you often need to modernize the experience layer before you touch core replacement. A platform that assumes a fresh core can become a blocker and extend timelines dramatically.

Treat “works with existing core” as a first-class requirement, not an afterthought.

Scalability and long-term extensibility

Does the platform become cheaper to run as you scale (because operations are automated), or more expensive (because everything is manual and vendor-priced)?

At scale, the biggest cost drivers are: support tickets, compliance cases, disputes, reconciliation exceptions, and vendor fees. A strong platform reduces those through automation, better tooling, and cleaner flows that create fewer exceptions.

Scalability isn’t just TPS — it’s “can we grow without doubling headcount?”

Best fit by buyer type

Banks, EMIs, and embedded finance teams should not buy the same “internet banking software” for the same reasons. Fit matters more than brand.

To reinforce fit-based evaluation, here’s a simple weighting model you can use internally:

| Criterion | Weight (Fintech launch) | Weight (Bank modernization) | Weight (Business banking) |

|---|---|---|---|

| Time to launch | High | Medium | Medium |

| Integration flexibility | High | High | High |

| Ops + compliance tooling | Medium | High | High |

| Entitlements + approvals | Low | Medium | High |

| Customization depth | High | Medium | High |

“Best” is contextual; what matters is choosing a platform that matches your operating model and growth path.

Pro tips (how CEOs avoid platform regret)

- Ask for the “provider swap story.” If switching KYC or issuer sounds like a rewrite, treat that as lock-in.

- Measure cost-to-serve early. Track support tickets per active user and compliance cases per 1,000 onboardings. That’s your future margin.

- Treat admin tooling as a product. The best digital banks ship internal tools with the same rigor as customer apps.

- Make vendor accountability explicit. “Vendor relationships can make or break a product’s success.” — Fintech Garden episode 110

Best online banking platforms to evaluate in 2026

This is the shortlist I’d put in front of a fintech CEO or a bank digital lead — with enough context to avoid superficial comparisons. The goal here is not to crown a universal winner. It’s to show you what each option is really good at, what it will constrain later, and how to avoid comparing incompatible categories (core vs digital layer vs white-label).

One practical rule: if a vendor can’t clearly explain which layer they own (core, digital, orchestration, license), assume you’ll discover the gaps the hard way after launch.

1) DashDevs / Fintech Core

Overview

Fintech core is DashDevs’ modular foundation for building digital banking and payment products — including online banking experiences — with an architecture designed for customization and provider choice.

Best for

- neobanks and challenger banks that need launch speed and flexibility,

- EMIs and fintechs building “banking-like” products,

- banks modernizing digital channels without getting trapped in a rigid platform.

Strengths

- Modular white-label foundation: start from proven blocks, not a blank repo.

- Custom flows are first-class: onboarding, payments, limits, and operations aren’t constrained to a fixed “SaaS journey.”

- Provider choice: integrate your preferred KYC/AML/fraud/open banking vendors instead of being forced into one stack.

- Designed for orchestration: a practical response to the reality that modern online banking products are vendor ecosystems.

- Proven delivery DNA: DashDevs built complex regulated platforms such as Dozens (UK challenger bank) and Tarabut Gateway (regulated open banking platform).

Trade-offs

- Not a “two-week SaaS click-to-launch.” You’re building a real product with room to evolve, which means you need proper discovery and delivery discipline.

Deployment model

Modular platform + product engineering. (If you need a self-hosting or specific deployment approach, that’s part of the architecture conversation.)

Customization level

High — including the ability to build differentiated workflows instead of operating inside a vendor’s fixed logic.

Notes on integrations / architecture

The practical advantage is vendor abstraction: you can swap or add providers as your regulatory footprint and commercial contracts evolve — which is often the difference between “we shipped” and “we can scale.”

2) Mambu

Overview

Mambu is a composable, cloud-first core banking platform. In an online banking platform context, it’s most relevant as the system your digital layer connects to.

When teams evaluate Mambu inside “internet banking platform” searches, the key is remembering: it’s primarily a core engine decision. You will still need a digital layer (build or buy) to deliver the online banking experience, operations workflows, and customer support tooling.

Best for

- teams modernizing or launching with a modern core, then layering a digital experience on top.

Strengths

- strong core capabilities and API-first posture (as cores go),

- works well in composable architectures.

Trade-offs

- it’s not a ready-to-run digital experience layer; you’ll still need an online banking platform or build one.

Treat Mambu as a core decision, then evaluate the online banking platform as a separate decision — or you’ll end up comparing mismatched categories.

3) Thought Machine

Overview

Thought Machine is a modern core banking platform designed for programmability and large-scale transformation programs.

It’s most relevant when the institution wants to treat core banking as programmable infrastructure. That’s powerful — but it’s a different kind of program than “launch online banking in months.”

Best for

- banks and large-scale fintechs undertaking serious core modernization with a long horizon.

Strengths

- strong “core as programmable infrastructure” narrative,

- suitable for institutions that want deep product logic control in the core.

Trade-offs

- it’s not an out-of-the-box online banking experience platform.

Evaluate Thought Machine when core modernization is the strategic initiative; pair it with a digital platform decision for online banking delivery.

4) Finastra (digital + ecosystem angle)

Overview

Finastra is a broad financial software suite vendor. The relevance here is often in the ecosystem: integration options, vendor coverage, and compatibility with institutional environments.

Business insight: suite vendors can reduce procurement complexity for large institutions, but they rarely reduce transformation complexity. You’re trading vendor count for program management.

Best for

- institutions that want a suite approach and can manage enterprise implementation.

Strengths

- breadth, partner ecosystem, enterprise fit.

Trade-offs

- breadth can also mean complexity; the “platform” decision often becomes a program.

When you buy a suite, plan for a program — and make sure your operating model can run it.

5) Backbase

Overview

Backbase is best known as a digital engagement layer for banks — essentially, a high-end digital experience layer sitting on top of core systems.

For banks, that’s often exactly the point: modernize the experience without ripping out core. But you still need orchestration, operations tooling, and clear integration boundaries to avoid creating a “beautiful front end on top of spaghetti.”

Best for

- banks modernizing their digital channels without replacing the core immediately.

Strengths

- strong digital channel capabilities,

- proven in banking environments where omnichannel delivery matters.

Trade-offs

- you still need to design the integration, operations tooling, and the rest of the ecosystem around it.

Backbase can solve the experience layer, but you still need to own the architecture that makes the experience reliable and auditable.

6) Temenos (digital banking stack)

Overview

Temenos operates across core and digital banking layers in many deployments. It’s commonly evaluated in large institutional modernization programs.

Temenos tends to show up when institutions need breadth and multi-market support. From a buyer perspective, treat it as an enterprise stack decision — not a quick “online banking software” purchase.

Best for

- banks that need enterprise-grade breadth and multi-market capabilities.

Strengths

- broad functional coverage, strong presence in banking.

Trade-offs

- typically not a “fast fintech launch” tool; it’s a program.

When Temenos is the right answer, you’ll know because you’re staffing and budgeting for transformation, not “shipping an app.”

7) FIS (digital banking and channel platforms)

Overview

FIS is a large financial technology provider used by many established banks. In the context of an “online banking platform,” FIS typically shows up when an institution wants a proven enterprise vendor for digital channels and servicing — and is willing to run a structured implementation program to get there.

For a buyer, the practical value is less about flashy features and more about enterprise fit: governance, scale expectations, institutional support, and long-term vendor continuity.

Best for

- established banks and large financial institutions modernizing online and mobile banking channels under an enterprise vendor model.

Strengths

- enterprise-grade delivery expectations and banking market maturity,

- strong compatibility with institutional operating models (process, controls, change management).

Trade-offs

- typically not optimized for “launch a new fintech in months” timelines,

- customization often looks like a program (and budget) rather than configuration.

Consider FIS when you’re buying a long-term enterprise digital channel capability — not when your main constraint is speed-to-market.

8) Fiserv (digital banking ecosystems)

Overview

Fiserv is another major incumbent in bank technology, often selected by institutions that want a wide ecosystem footprint and an enterprise delivery model for digital banking, payments, and customer-facing services.

The business lens here is “operating model alignment.” If your organization already runs on enterprise vendor governance and wants a large-vendor ecosystem, Fiserv can be a natural fit in the online banking platform evaluation set.

Best for

- retail and community banks that prioritize vendor ecosystem coverage and established operational patterns.

Strengths

- broad institutional presence and ecosystem maturity,

- strong fit for banks that need predictable vendor-backed roadmaps and support models.

Trade-offs

- less suitable for fintech teams seeking deep workflow ownership and fast iteration,

- channel modernization can become a multi-stream program depending on integrations and legacy constraints.

Fiserv belongs on the shortlist when a bank wants a broad, enterprise ecosystem — and accepts the programmatic nature of change.

9) Jack Henry (digital banking for US bank segments)

Overview

Jack Henry is a well-known provider in the US banking technology landscape, especially in segments where institutions want a proven vendor for digital banking experiences, servicing, and operational reliability.

For business owners, the key point is segmentation: some platforms win because they map well to specific bank categories and operating models — not because they’re the most customizable. Jack Henry is often evaluated on that basis.

Best for

- banks looking for a vendor-aligned digital banking experience layer with established operating patterns and institutional support.

Strengths

- strong positioning for bank segments that value stability, support, and predictable delivery,

- clear relevance to digital channel modernization conversations (web/mobile/servicing).

Trade-offs

- not a “build anything you want” foundation; customization is typically bounded by the vendor’s model,

- not designed for embedded finance teams that want to treat online banking as an extensible product layer.

Jack Henry is most appropriate when you’re modernizing a bank channel stack inside a bank-shaped operating model — not when you need product-led flexibility.

10) Custom-build route with an orchestration partner

This is not “build everything yourself.” A modern custom-build route is usually:

- a digital experience layer (web/mobile/admin),

- an orchestration layer (workflow + policies + adapters),

- a core/ledger layer (own or via vendor),

- plus integrated vendors (KYC/AML/cards/open banking/fraud).

When differentiation is your business model, this can be the best route — but only when operations and compliance are designed in from day one.

Custom-build is smartest when workflows are your moat — but only if you build internal tooling and compliance evidence as first-class deliverables.

The right “best platform” shortlist is the one that matches your buyer type and your intended operating model — not the one with the most features on a slide.

Where DashDevs fits among online banking platform providers

We are not trying to be every platform for every buyer. The strength is combining launch speed with architectural freedom — which is exactly where many teams get stuck between “SaaS lock-in” and “custom build from scratch.”

Here’s the honest positioning:

DashDevs is for teams that want a real product — launched fast — without signing away their future flexibility.

Not just a skin on top of someone else’s roadmap

When your platform provider owns the roadmap, you’re building your business on someone else’s priorities. That’s survivable for standard products — and painful for differentiated ones.

Episode 110 frames the risk of unclear accountability in vendor relationships:

“Vendor relationships can make or break a product’s success.” — Fintech Garden episode 110

Choose partners that let you own the product direction — and make accountability explicit.

Modular architecture instead of rigid package logic

Rigid package logic is what kills iteration later: every non-standard onboarding rule or payment policy becomes a “vendor request.” Modular architecture turns those into product decisions again.

Business consequence: modular architecture protects your roadmap. It’s what keeps you from redesigning pricing, onboarding, or risk logic around vendor constraints.

When your business model changes (and it will), modularity is the difference between iteration and re-platforming.

Better fit for products that need differentiated UX and workflows

If your competitive advantage is:

- a better onboarding funnel,

- a smarter risk flow,

- or a business banking workflow that actually matches how finance teams operate,

then you need an architecture that treats workflows as your asset — not the vendor’s.

When your differentiation is in “how the bank works,” not just “how it looks,” you need workflow ownership.

Works for launch today without locking tomorrow

The most sustainable approach I see across fintech is hybrid:

- launch on a modular foundation,

- then extend in the directions your market proves.

That’s the “buy now, build later” strategy in practice — not as a slogan.

You reduce risk by avoiding a two-year all-or-nothing build, while also avoiding a rigid vendor box.

Supports vendor choice instead of forcing one stack

Provider contracts change. Regions change. Fraud patterns change. Regulators change.

So if you’re serious about scale, your online banking platform should assume vendor change is normal — not exceptional.

Vendor choice is not a nice-to-have; it’s how you keep commercial leverage as you scale.

DashDevs is best for teams that want to launch fast and still keep the ability to evolve integrations and workflows as the business grows.

Must-have features in a modern online banking platform

Below is a CEO-friendly view of “features” that actually behave like systems. Each one touches ops, compliance, fraud, and unit economics — which is why feature checklists are never enough on their own.

Real-time account and balance visibility

Delayed balances undermine everything else. Real-time visibility isn’t just UX — it’s trust.

You also need operational clarity: pending vs settled, transfer status, and a reliable dispute trail. If customers can’t understand their balance, support volume rises. If support can’t explain it, escalations rise.

Treat “real-time visibility” as both a customer capability and an internal support capability.

Payments and transfers

Transfers, schedules, limits, receipts, and operational support for failed/returned payments are where “online banking products” become real.

Business insight: payments are where margin and risk meet. Your platform should support fee logic, limits, approvals (for business banking), and post-transaction evidence for disputes and AML review.

The best payments UX is the one that also reduces exceptions, not just clicks.

User authentication and role management

Strong authentication plus flexible role-based access control becomes critical the moment you support business banking users.

For retail, the core is MFA + session integrity. For business banking, it’s entitlements: who can initiate, approve, view, export, and administer — with audit trails attached.

For teams planning to go upmarket, role management needs to be a platform primitive, not an afterthought.

Card lifecycle controls

Freeze/unfreeze, PIN, virtual cards, spend controls, disputes: card operations are one of the highest-leverage engagement drivers — and one of the most failure-sensitive.

Card controls also reduce fraud losses and support tickets. If customers can freeze a card instantly and see the impact immediately, you avoid panic calls and lower operational load.

Card lifecycle controls are both a customer feature and a fraud/ops control.

Digital onboarding and KYC orchestration

Onboarding is your growth engine. Treat it as such. A good starting point is from digital onboarding to daily banking.

Onboarding needs risk-based routing, evidence capture, and manual review queues for edge cases — otherwise you either block good customers or onboard bad ones. This is where your conversion rate and fraud rate are negotiated in real time.

From a cost perspective, automation is the unlock: McKinsey notes digital onboarding can cut KYC costs by up to 50% and reduce onboarding time dramatically when implemented well.

To operationalize that in your roadmap, connect this section to execution resources: KYC services, fintech integrations, and fintech software development.

Great onboarding is not “less KYC.” It’s smarter KYC plus operational tooling.

Notifications and alerts

Notifications are a security control (fraud) and a retention tool (habit). They’re also an operational obligation: they must be explainable and auditable.

Business insight: notifications define perceived trust. A delayed alert after a card transaction feels like a breach even if everything is fine. Conversely, too many alerts creates fatigue and disabled notifications, which reduces the value of the channel.

Design notifications as a product system with policy, not as a UI add-on.

Personal finance or business finance tools

Retail: categorization, budgets, goals. Business: cash flow views, invoices, approvals, reconciliation exports.

These tools are retention drivers because they create reasons to open the app beyond transfers. In business banking, they also become workflow anchors: approvals, exports, and reconciliation patterns.

Finance tools are not vanity features — they’re habit and workflow builders.

Admin back office and compliance workflows

Without this layer, you don’t scale — you hire. And hiring is rarely the best scaling strategy in regulated finance.

Admin tooling should support customer support, compliance reviews, disputes, evidence capture, and audit exports. If ops can’t resolve issues in minutes, customers feel friction and the business pays twice (support cost + churn).

The best online banking platforms treat back office as a first-class product.

APIs and third-party integrations

Your platform is only as flexible as its integration layer. If your integrations are hardwired, your business becomes hardwired too.

This is where “platform providers” diverge. If integrations are adapter-based, swapping vendors is feasible. If integrations are embedded deep in flows, switching becomes a rewrite.

Integration architecture is where you either preserve optionality or create lock-in.

Analytics and event tracking

Track:

- onboarding drop-off,

- payment failures,

- fraud signals,

- support tickets per active user,

- and the cost of servicing customers.

That’s how you turn digital banking into a business, not a feature set.

Also track: onboarding step timings, card control adoption, and where compliance creates friction. Those are the levers that improve conversion without increasing risk.

Analytics should power decisions weekly, not post-mortems quarterly.

Must-have features at a glance

| Capability | Why customers care | Why the business cares |

|---|---|---|

| Real-time balances | Trust and clarity | Lower support load, fewer disputes |

| Payments | “Make money move” | Revenue, fee logic, risk controls |

| Cards | Control and safety | Interchange, fraud reduction, retention |

| Onboarding/KYC orchestration | Fast access | Conversion + compliant scaling |

| Admin/back office | (Invisible) | Cost-to-serve, auditability |

| Integrations | “It works everywhere” | Optionality, expansion speed |

The “must-haves” are the features that reduce exceptions and operational load while increasing trust and engagement.

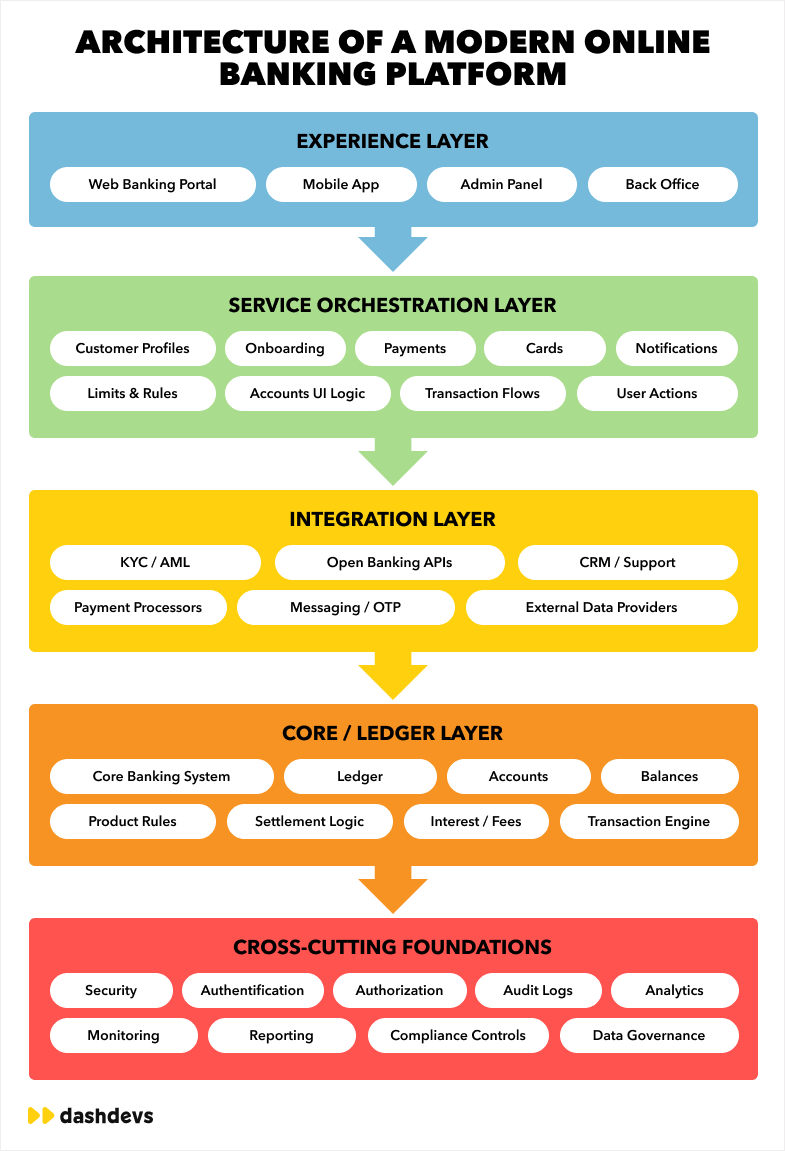

Architecture of a modern online banking platform

You’ll see many “banking platform diagrams.” Most are marketing. Here’s the version that matters operationally.

Experience layer

- Web online banking

- Mobile banking apps

- Admin / back office console

This is where your brand lives — but it’s not where your bank is. Treat the experience layer as thin: it should consume APIs, not embed business logic. That separation is what lets you ship quickly without destabilizing regulated flows.

Thin clients keep your platform governable and your teams faster.

Orchestration and service layer

- customer profile and entitlements

- payments orchestration and limits

- cards orchestration

- workflow engine (onboarding, approvals, disputes)

- notifications service

This is where product differentiation usually lives: how onboarding works, how limits are enforced, how approvals happen, how exceptions are handled. If you can’t change this layer safely, your roadmap becomes hostage to your initial vendor choices.

Invest in orchestration early — it’s the layer that makes composable banking real.

Integration layer

- core banking / ledger

- KYC / AML vendors

- fraud / monitoring

- card issuer / processor

- open banking / bank connectivity

- CRM / support tooling

The integration layer determines whether adding a new provider is “a few weeks” or “a rebuild.” Architecturally, the goal is to isolate providers behind adapters and normalized domain models, so the rest of the platform doesn’t speak vendor dialects.

A good integration layer keeps your platform stable even when vendors change.

Data and analytics layer

- audit trails and immutable logs

- event streams for analytics

- dashboards for ops and compliance

This layer is your evidence engine. It’s also your growth engine: cohort analysis, onboarding drop-offs, fraud anomaly patterns, and support cost drivers all live here when implemented properly.

In regulated products, data architecture is operational architecture.

Security and compliance layer

- IAM, MFA, device binding

- encryption in transit/at rest

- key management and secrets

- access logging and reporting

Security controls must be policy-driven and auditable. If you can’t prove a control exists (and was enforced), it effectively doesn’t exist during audits.

Security becomes a growth enabler when it reduces fraud and speeds up compliant change. Designed as one monolith, every change is risky. Designed as a layered system with clear seams, change becomes a capability.

Architecture isn’t an engineering preference — it’s the mechanism that determines speed, safety, and long-term cost.

What makes an online banking platform secure?

Security is not a section you skim. In online banking, “security” is a product promise, an operational cost driver, and a regulatory survival requirement. The goal is to embed controls that reduce fraud and disputes without turning UX into a false-positive factory.

Authentication and access control

MFA is table stakes. The real security differentiator is access control that matches reality:

- consumers vs business users,

- operators vs support teams,

- and least privilege across services.

For business banking, access control is a product feature. It’s what allows CFOs and finance teams to trust the platform with approvals, payroll, and high-value payments without creating a single “super admin” risk.

The strongest platforms treat entitlements as core infrastructure, not a later add-on.

Encryption and auditability

Encryption is expected. Auditability is what keeps you alive during disputes, regulator questions, and incident response.

Auditability includes consistent event logging, immutable trails for critical actions, and the ability to answer “who did what and when” without pulling engineers into a week-long forensics exercise.

Auditability is the difference between a contained incident and a reputational crisis.

Fraud monitoring and anomaly detection

Fraud isn’t solved in one place. It’s a system: device signals, behavioral patterns, transaction monitoring, and operations workflows.

Episode 138 nails the direction of travel: fraud is increasingly identity-centric, and the platform has to treat identity as a continuous trust layer rather than a one-time onboarding step.

“Criminals don’t steal money. They steal identities.” — Fintech Garden episode 138

Fraud monitoring only works when it’s connected to operations workflows (holds, reviews, evidence, escalation), not just dashboards.

Vendor governance

In a vendor-heavy stack, your security posture is the security posture of your vendors. Vendor governance is not procurement — it’s architecture and operations.

That means clear data boundaries, audit evidence, incident response expectations, and fallback plans for vendor outages. If one vendor outage breaks onboarding, you have a single point of failure you don’t control.

To strengthen security before launch, pair architecture with execution assets: penetration testing services and an SDLC discipline (see secure software development life cycle). For regulated expansion planning, it also helps to align your platform governance to your target market realities (see fintech regulations for businesses: US, EU, UK, MENA).

Governance is how you turn vendor ecosystems from risk into leverage.

Regulatory logging and reporting

Regulated products require logging that is:

- complete,

- consistent,

- and retrievable under pressure.

Logging must be designed for reality: disputes, AML requests, and regulator questions happen under time pressure. If you can’t retrieve evidence quickly, risk escalates.

Build regulatory logging as a product requirement, not an engineering afterthought.

Why “secure UI” is not the same as secure platform design

Pretty UX can hide fragile architecture. Secure platforms survive:

- outages,

- fraud spikes,

- vendor failures,

- and compliance reviews.

That’s the bar.

For a strong “identity layer” lens on where security is going, Fintech Garden episode 138 is one of the more practical discussions about identity being the missing layer as banking becomes real-time.

Security controls at a glance

| Control | What it prevents | Business impact |

|---|---|---|

| MFA + device binding | Account takeover | Lower fraud losses, fewer support calls |

| Least privilege + RBAC | Insider risk, unauthorized actions | Better audit outcomes, safer operations |

| Immutable audit trail | Evidence gaps | Faster investigations, lower compliance cost |

| Transaction monitoring + workflows | Fraud escalation failures | Reduced loss, improved customer trust |

| Vendor governance + fallbacks | Single points of failure | Higher availability, safer scaling |

Security is not a checkbox — it’s a platform design discipline that protects trust and unit economics.

A platform that can’t produce evidence quickly (audit logs, decisions, approvals, device history) will be “secure in theory” and expensive in reality.

Online banking platforms for business banking and corporate finance use cases

For SME or corporate clients, you’re not building “mobile banking platform software.” You’re building a finance operations product with banking rails. That changes everything: identity becomes multi-user, payments become policy-driven, and retention becomes tied to reconciliation workflows.

Multi-user roles and permissions

Business banking needs entitlements: roles, policies, teams, departments, and what they’re allowed to do.

The business reason is simple: finance operations are multi-person workflows. Without entitlements, you can’t serve real SMEs; you can only serve “a single founder with a debit card.”

Roles and permissions are your entry ticket to corporate-grade accounts.

Approval flows

Approvals are the difference between “consumer app with business pricing” and “business banking.”

Approvals also reduce risk: two-person rules, thresholds, and audit trails. They’re a control mechanism and a product feature at the same time.

For higher-value accounts, approvals are the price of admission.

Bank connectivity and treasury-style views

Businesses want consolidated views: accounts, cash position, and connectivity — especially if you support open banking aggregation.

This is where “bank connectivity platform” and “finance management” intent comes from: finance teams want a dashboard, not just a list of transactions. Aggregation also changes support: when a connection fails, you need clear UX and operational visibility.

Connectivity is only valuable when it’s reliable — and explainable to users.

Bulk payments and recurring transactions

Payroll-style bulk payments and recurring runs change how your platform must be designed (limits, controls, operational support, reconciliation).

Bulk capabilities also change compliance and fraud requirements: batching evidence, approval logs, and safeguards against account takeover. This is not just “send money,” it’s “operate a finance process.”

Bulk payments turn your platform into a finance tool, not just a banking interface.

Reconciliation and finance operations support

Exports, audit trails, receipts, and integrations with finance tooling are not optional in business banking. They are the product.

This is where retention often comes from in SME banking: once reconciliation is embedded into a workflow, switching costs increase (in a good way) because your platform becomes part of operations, not just a utility.

Painful reconciliation makes churn easy. Smooth reconciliation makes you sticky.

Business banking capabilities at a glance

| Capability | SME value | Platform implication |

|---|---|---|

| Entitlements | Team governance | RBAC, policy engine |

| Approvals | Risk control | Workflow engine + audit trails |

| Bulk payments | Operational efficiency | Limits, batching, monitoring |

| Reconciliation exports | Finance workflow integration | Data model + integrations |

| Connectivity views | Cash visibility | Open banking adapters + status tooling |

Business banking success is mostly about workflows and controls — not UI.

Business users don’t pay for “nice UI.” They pay for control, auditability, and fewer operational headaches.

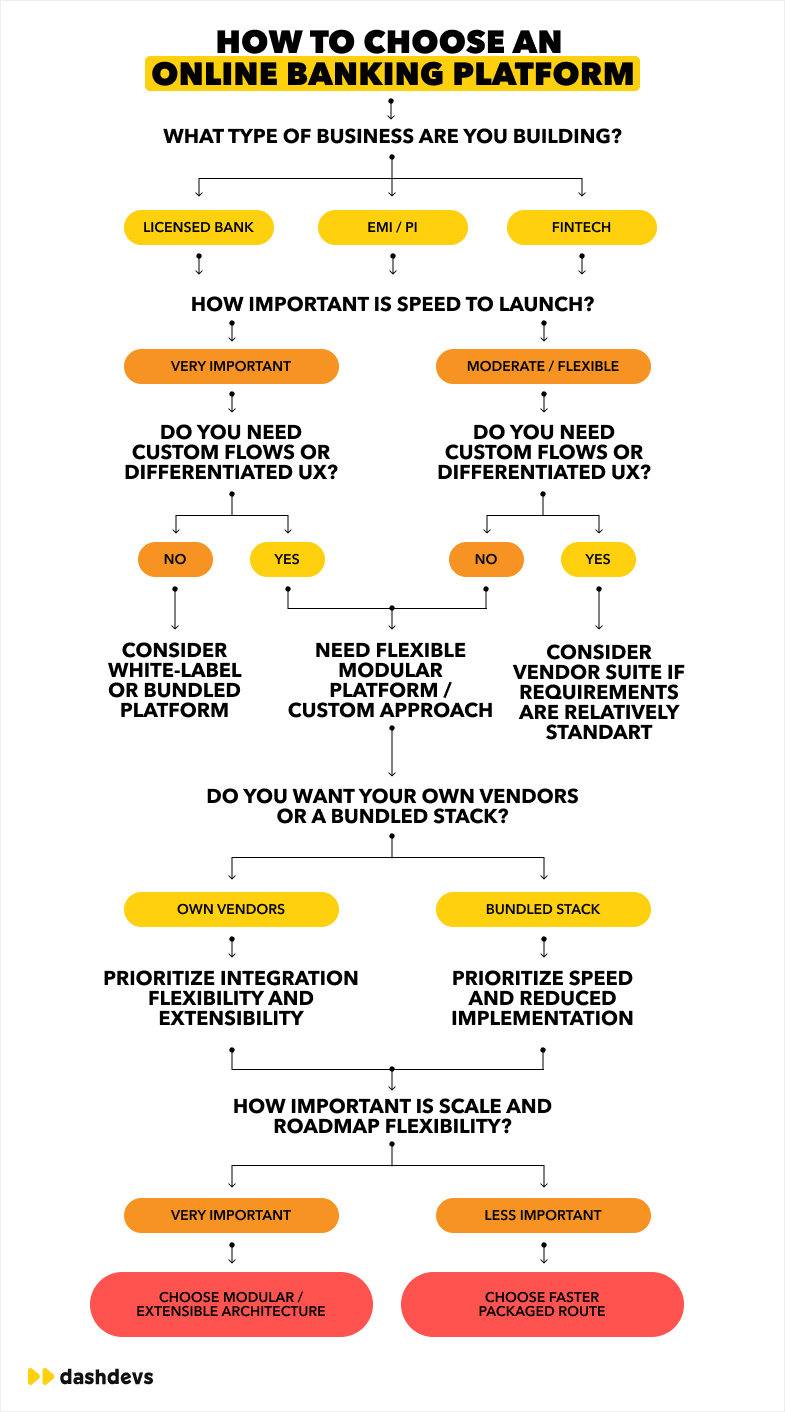

Build vs buy vs white-label: which route should you choose?

There’s no moral high ground here — only trade-offs. The right route depends on your timeline, your differentiation strategy, and how much vendor dependency you can accept before it starts limiting growth. The most expensive mistake is picking the fastest path without understanding the long-term switching cost.

Choose white-label when speed matters most

White-label is great when:

- you need to validate the market,

- you need a compliant foundation quickly,

- and your workflows are relatively standard.

But be honest about your roadmap. If you expect to add markets, change onboarding logic, or serve SMEs with approvals and entitlements, pressure-test flexibility early. Fast launch is valuable — rebuilding later is not.

Choose white-label when speed is the constraint and differentiation can come later.

Choose a vendor platform when operating model is relatively standard

When you’re not differentiating on unique workflows and want an enterprise vendor relationship, vendor platforms can make sense — especially for banks modernizing channels.

This route also makes sense when the organization values procurement stability, institutional vendor support, and established implementation ecosystems. The cost is slower change and more program management.

Enterprise vendor platforms are strongest when your operating model is stable and your governance model fits enterprise delivery.

Choose modular/custom when differentiation matters

If your business model requires:

- custom onboarding logic,

- a unique risk posture,

- business banking workflows,

- or a product you can evolve across markets,

then modular/custom is often cheaper over time because you avoid lock-in.

This is the CEO trade-off: you invest more attention into architecture upfront, but you protect your ability to evolve the product without renegotiating your roadmap with vendors.

Choose modular/custom when workflows and experience are how you compete.

Hybrid route: launch fast, extend later

This is the route I recommend most often:

- launch on a modular foundation,

- prove your distribution and economics,

- then extend what makes you different.

For teams building a digital bank, this aligns well with the strategy described in how to build a digital bank.

Hybrid is the most pragmatic path when you need speed now and flexibility later.

Decision matrix (practical filter)

| Question | If “yes” | Bias toward |

|---|---|---|

| Do we need to go live in months (not a year)? | You need speed | White-label or modular foundation |

| Do we expect provider changes (KYC/AML/cards/open banking) in 12–24 months? | You need flexibility | Modular/custom with adapters |

| Are we building business banking (roles/approvals/bulk/recon)? | You need workflow depth | Modular/custom or enterprise digital layer |

| Are we modernizing a bank without replacing core now? | You need integration with legacy | Digital layer + orchestration on top of existing core |

| Is differentiation central to our model? | You need control | Modular/custom (hybrid launch) |

Build vs buy vs white-label at a glance

| Route | Best when | Hidden cost to watch |

|---|---|---|

| White-label | MVP speed is priority | Vendor constraints on workflows and provider choice |

| Enterprise vendor | Bank modernization programs | Program complexity, slower iteration |

| Modular/custom | Differentiation is core | Upfront architecture + ops tooling investment |

| Hybrid | Speed now, flexibility later | Clarity on what you will replace/extend and when |

Make the decision with your future roadmap in mind. The cheapest launch is often the most expensive scale.

Common mistakes when choosing an online banking platform

Most platform mistakes are not technical. They are category mistakes: confusing UI for platform, confusing platform for license, and confusing “launch speed” for “ability to scale.” This section is a checklist of avoidable pain.

Confusing frontend polish with platform strength

A beautiful UI can sit on a fragile backend. Ask about operations tooling, auditability, and failure modes.

For a simple test, ask how a support agent resolves “chargeback + missing push notification + delayed balance” without calling engineering. That’s platform strength.

Customers won’t forgive “pretty and broken.” They’ll just switch.

Ignoring integration lock-in

With hardwired vendors, switching becomes a re-platforming project. Assume you will need to change providers.

Contracts change. Pricing changes. Coverage changes. You should be able to swap providers the way you renegotiate cloud spend — not the way you migrate cores.

Lock-in is not only technical — it’s commercial.

Underestimating compliance workflows

Compliance is not only KYC. It’s ongoing monitoring, case management, evidence, and reporting.

When compliance isn’t embedded into the platform, it ends up in spreadsheets and manual queues — which is how cost-to-serve and risk quietly grow.

Compliance workflows are product workflows in regulated finance.

Choosing for MVP only, not scale

The platform you choose will shape your cost base at scale. Optimize for survivability, not just launch.

Episode 122’s “complexity vs complication” lens is a useful guardrail: scale introduces complexity; your platform choice determines whether that becomes manageable or painful.

Choose a platform that gets easier to run as you grow, not harder.

Assuming all white-label platforms are equally flexible

They’re not. Some are “branding-only.” Some are modular foundations. Treat this as a structural difference, not a pricing difference.

“White-label” is a marketing term; flexibility is an architecture property.

Common mistakes and their business cost

| Mistake | How it shows up | Business cost |

|---|---|---|

| UI-first evaluation | Great demo, weak ops | Support headcount growth, churn |

| Hardwired vendors | Provider can’t be swapped | Higher fees, slower expansion |

| Weak compliance tooling | Manual reviews everywhere | Higher opex, audit risk |

| MVP-only decisions | Rebuild at scale | Lost velocity, missed markets |

The best platforms are the ones that make the messy 5% of cases (exceptions, disputes, reviews) cheaper to handle — not just the happy path prettier.

Future of online banking platforms

The next phase of online banking is less about new screens and more about new primitives: identity, orchestration, and multi-rail money movement. If you’re choosing a platform in 2026, you’re choosing whether you’ll be able to adopt these shifts without re-platforming.

Embedded finance inside broader ecosystems

Online banking will increasingly be distributed: banking capabilities embedded inside SaaS, marketplaces, and vertical ecosystems.

For platforms, that means better APIs, stronger entitlements, and better developer experience — because your “online banking” surface will often be someone else’s product.

The platforms that win will embed cleanly without losing governance.

AI-assisted servicing and operations

AI will show up first in operations: support deflection, anomaly detection, and compliance case triage — not as a chatbot gimmick.

The ROI path is clear: fewer support tickets per active user, faster compliance handling, and earlier detection of fraud patterns. But it only works if your platform produces clean event streams and evidence trails.

AI needs data discipline first — otherwise you automate noise.

Stronger identity and trust layers

Identity is becoming the real moat. Regulation and fraud pressure will push stronger identity primitives into the platform layer.

Episode 138 frames the core gap: money is moving in real time, but trust and identity are still too often “digitized paper.”

Identity will move from “KYC step” to continuous trust layer across journeys.

More modular cores and orchestration

The market is moving away from monoliths toward composable stacks — where the online banking platform is the orchestrator, not just a UI.

This is not ideology — it’s survival. As you add vendors, rails, and features, orchestration prevents a brittle web of point integrations.

Composability is a response to ecosystem reality, not a buzzword.

Multi-rail money movement across fiat, cards, and digital assets

Customers will expect money movement across rails without caring which rail is underneath. Platforms will need to abstract that complexity while keeping compliance and auditability intact.

This pushes platforms toward a policy-driven routing mindset with strong observability. Multi-rail failures can be subtle, so the platform needs clear states, evidence, and reconciliation tooling.

Multi-rail experiences will become normal; platforms that can’t abstract rails cleanly will feel outdated.

Future trends at a glance

| Trend | What customers notice | What operators need |

|---|---|---|

| Embedded finance | “Banking everywhere” | Strong APIs, entitlements, governance |

| AI in ops | Faster support and safer payments | Event streams, evidence, clean data |

| Identity evolution | Less friction, fewer fraud incidents | Continuous trust layer, consent models |

| Composable stacks | Faster product iteration | Orchestration + adapters |

| Multi-rail payments | Seamless movement | Policy-driven routing + observability |

Future winners will combine great UX with platforms that can evolve safely under regulation and ecosystem complexity.

Choose a platform that assumes the world will change — because it will.

Summing up

In 2026, the “best online banking platform” is the one that fits how you run the business: who you serve, how you make money, and which partners you must plug in (core/ledger, KYC/AML, cards, payment rails, open banking).

When you compare providers, don’t get stuck on feature lists. Ask what happens after launch: how many cases still go to manual ops, how hard it is to swap a vendor later, and how quickly you can prove decisions with logs and approvals when an audit or incident happens.

For a practical buyer filter, focus on three things that show up on your P&L: (1) cost to serve (exceptions, disputes, manual reviews), (2) change cost (new rails, new markets, new vendors), and (3) governance cost (security, access control, evidence for audits). Platforms that score well here usually feel “boring” in a demo — but they stay profitable when volume, fraud pressure, and regulatory scrutiny increase.

Finally, be clear about what you need to own vs outsource. If your differentiation is in workflows (onboarding, limits, approvals, risk policies), choose a provider that lets you control those flows without waiting on a vendor roadmap; if your operating model is standard and stability is the priority, an enterprise ecosystem can be the right trade-off as long as you budget for a program, not just an implementation.

Share article