Top Online Banking Platforms for Banks and Fintech Teams in 2026

July 10, 2026

Summary

Key takeaways

- This guide evaluates vendor online banking platforms for banks and fintech builders — not consumer-facing neobanks like Ally or SoFi.

- The best online banking platforms in 2026 are judged on composability, integration flexibility, and scalability — not mobile bill-pay checklists.

- Digital banking platform providers span white-label launch stacks, enterprise digital layers, and modular foundations — category fit matters more than brand.

- AI-assisted cash forecasting, ISO 20022 migration, and open finance connectivity are forcing replacement cycles on legacy internet banking stacks.

- A fit-based evaluation framework — customization depth, ops tooling, provider swap cost — beats feature-matrix RFPs every time.

Search results for the best online banking platforms split into two audiences: consumers hunting for Ally, Axos, or SoFi — and institutions evaluating digital banking platforms like Backbase, Temenos, or Q2. This guide is written for the second group. If you are a bank digital lead, fintech CEO, or product owner comparing online banking platform providers and online banking solution providers for a licensed or sponsor-bank program, you need an architectural buyer’s guide — not a retail bank ranking.

The market is moving. Global treasury and digital banking platforms spend is projected above $7 billion in 2026, with double-digit growth driven by ISO 20022 migration deadlines, AI-assisted forecasting adoption, and banks replacing legacy e-banking layers that cannot iterate at product speed. Ripple’s acquisition of GTreasury and incumbent AI features across enterprise suites signal that 2026 evaluations must include composability, open banking platform connectivity, and integration depth — not just channel UX.

What is an online banking platform?

An online banking platform is the software infrastructure that enables customers and business users to access banking products digitally — through web and mobile — with the workflows, integrations, security controls, and operational tooling required to run in production.

Three distinctions matter before any vendor demo:

- The platform is not the app. The app is one channel; the platform is what makes that channel compliant, auditable, and scalable.

- The platform is not the core. The core holds the ledger; the platform orchestrates journeys on top of it. See what core banking is for the foundation layer, and banking software solutions for how vendors map the market — distinct from the digital delivery layer itself.

- The platform is not the license. BaaS and sponsor-bank partnerships provide regulated rails; the platform is what customers actually experience.

At minimum, production-grade electronic banking software includes account access, payments and transfers, card lifecycle controls, onboarding and authentication, alerts, support tooling, and admin consoles with audit trails. Online banking platforms that skip operations tooling fail under real volume — when disputes, AML reviews, and reconciliation exceptions arrive.

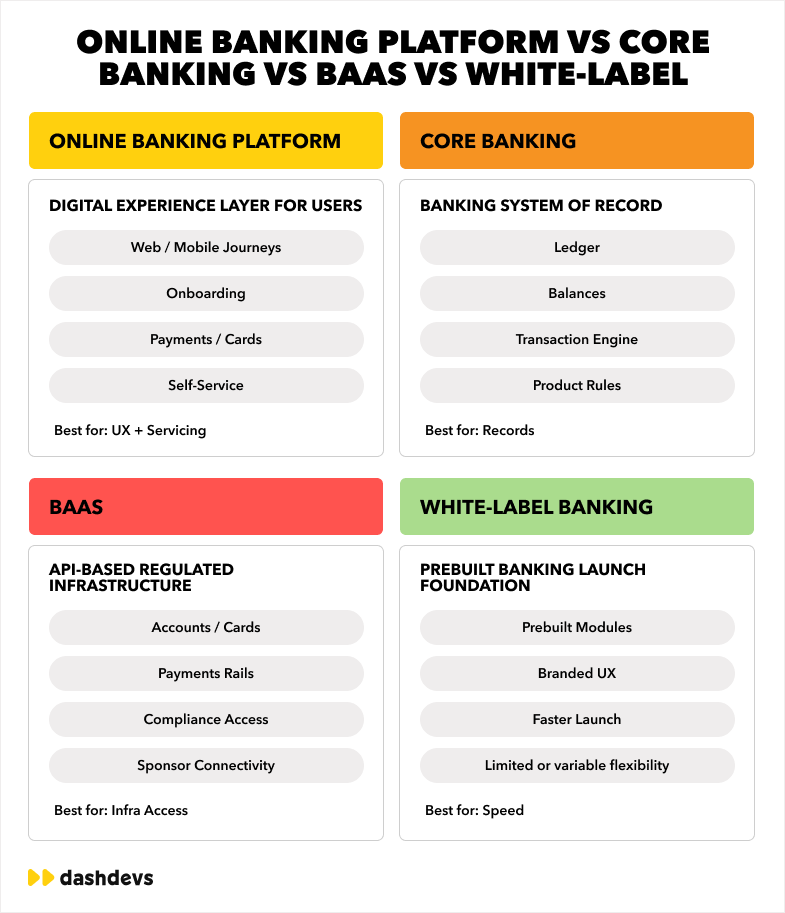

Online banking platform vs core banking vs BaaS

| Layer | What it does | Buyer question |

|---|---|---|

| Core banking | Ledger, balances, product rules | Who owns truth? |

| Online banking platform | Digital experience, orchestration, ops | Who owns journeys? |

| BaaS | Licensed API access to banking rails | Who owns regulation? |

| White-label foundation | Prebuilt modular launch stack | How much future flexibility? |

BaaS compresses licensing time but creates infrastructure dependency — evaluate it as a long-term operating decision, not a SaaS subscription. White-label depth varies from branding-only configs to modular foundations you can extend. The neobank app development company path often combines BaaS rails with a custom or modular digital layer rather than accepting a vendor’s fixed product logic.

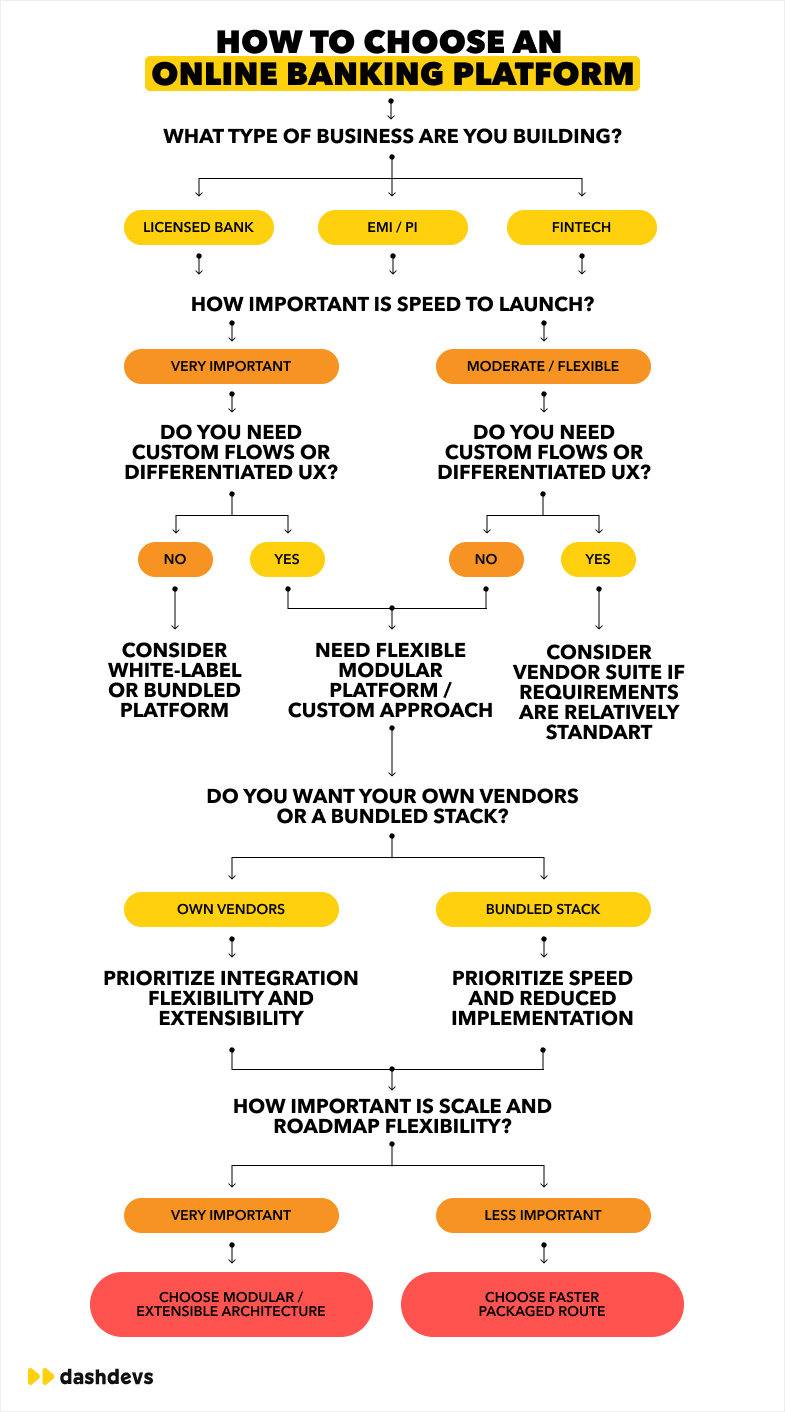

How to choose a digital banking platform in 2026

Top-performing buyer guides share one trait: they give readers a methodology, not just a list. Pages that lead with bill-pay features feel dated; pages that lead with composability, integration flexibility, and scalability earn institutional trust.

Use this framework before shortlisting online banking platform vendors and digital banking platform vendors across leading digital banking platforms:

- Composability — Can you swap KYC, card, or bank connectivity vendors without rewriting core flows?

- Integration flexibility — Does the platform expose APIs and adapters, or hardwire a single vendor stack?

- Time to launch — How fast to a compliant MVP that survives real onboarding volume, not a demo?

- Ops and compliance tooling — Can support and compliance teams resolve cases inside the product?

- Customization depth — Can you change onboarding rules, limits, and approvals — or only colors and logos?

- AI readiness — Does the architecture produce clean event streams for forecasting, fraud triage, and servicing automation?

- Core compatibility — Can it sit on your existing core during modernization, or does it force rip-and-replace?

Roughly half of US corporate treasurers now pilot AI-assisted cash forecasting — accuracy in the high 80s at a 13-week horizon versus ~60% for spreadsheet models. Platforms that cannot feed structured transaction and balance data to analytics layers will fall behind on both retail engagement and treasury adjacency.

For vendor ecosystem mapping beyond the digital layer, open banking solutions and cross-border payment integration solutions belong in the same architecture conversation — modern online banking platforms are a connectivity problem as much as a UX problem. Internet banking at institutional scale is never a front-end project alone.

Pro tip: ask every vendor, “If we need to switch KYC or issuer in 18 months, what breaks and how much work is it?” Unclear answers signal lock-in.

Top 10 best online banking platforms to evaluate in 2026

There is no universal winner among online banking platforms or digital banking platforms. The list below maps what each option is actually good at — for banks, EMIs, fintech banks, and builders — not for retail consumers choosing where to deposit a paycheck. Treat it as a starting shortlist of digital banking platform providers, not a feature-score ranking.

| # | Platform | Category | Best for |

|---|---|---|---|

| 1 | DashDevs Fintech Core | Modular foundation | Neobanks and fintechs needing speed plus workflow ownership |

| 2 | Backbase | Digital engagement layer | Banks modernizing channels without core replacement |

| 3 | Temenos | Enterprise core + digital stack | Multi-market banks running transformation programs |

| 4 | Mambu | Composable core | Teams building API-first stacks with separate digital layer |

| 5 | Thought Machine | Programmable core | Large institutions treating core as infrastructure |

| 6 | FIS | Enterprise digital channels | Established banks under institutional vendor models |

| 7 | Fiserv | Banking ecosystem suite | US community and regional banks |

| 8 | Jack Henry | Segment-aligned digital banking | US banks prioritizing vendor stability |

| 9 | Finastra | Broad financial software suite | Institutions wanting ecosystem breadth |

| 10 | Custom build + orchestration partner | Composable architecture | Teams where differentiated workflows are the product |

1. DashDevs / Fintech Core

Fintech Core is a modular neobank platform and foundation for digital banking and payment products — online and mobile channels with provider choice across KYC, cards, and open finance APIs. Best for neobanks, EMIs, and challengers that need launch speed without surrendering workflow control. Proven delivery includes Dozens and Tarabut Gateway. Trade-off: requires proper discovery and delivery discipline — not a two-week SaaS click-to-launch.

2. Backbase

Backbase is a digital engagement layer for banks — high-end omnichannel delivery on top of existing cores. Best for incumbent banks modernizing web and mobile without immediate core migration. Strength: mature banking UX at scale. Trade-off: you still own orchestration, ops tooling, and integration boundaries around the experience layer.

3. Temenos

Temenos spans core and digital banking in many enterprise deployments. Best for multi-market banks with budget and appetite for transformation programs. Strength: broad functional coverage. Trade-off: timeline and complexity — not a fast fintech launch path.

4. Mambu

Mambu is a cloud-native composable core. In vendor evaluations across digital banking platforms, remember it is primarily a core decision — you still need a digital layer for customer experience and operations. Strength: API-first core posture. Trade-off: not a ready-made internet banking product.

5. Thought Machine

Thought Machine targets programmable core infrastructure for large-scale programs. Best when core modernization is the strategic initiative. Pair with a separate digital channel decision for internet banking delivery.

6. FIS

FIS serves established banks with enterprise digital channel and servicing capabilities. Best when institutional governance, vendor continuity, and long-term support models matter more than startup iteration speed.

7. Fiserv

Fiserv offers broad ecosystem coverage for US banking segments. Best for community and regional banks aligned with enterprise vendor operating patterns. Less suited for product-led fintech teams needing deep workflow customization.

8. Jack Henry

Jack Henry fits US bank segments that prioritize stability and segment-specific digital offerings. Best for channel modernization inside a bank-shaped operating model — not embedded finance products treating banking as an extensible layer.

9. Finastra

Finastra provides suite breadth across financial software categories. Best when procurement prefers fewer vendor relationships — accepting program complexity in return.

10. Custom build with orchestration partner

Not a vendor SKU — a composable route: experience layer, orchestration, core (own or vendor), and integrated specialists. Makes sense when onboarding logic, business banking workflows, or risk posture is the competitive moat. DashDevs supports this path through fintech software development and modular cores — launch on proven blocks, extend what differentiates.

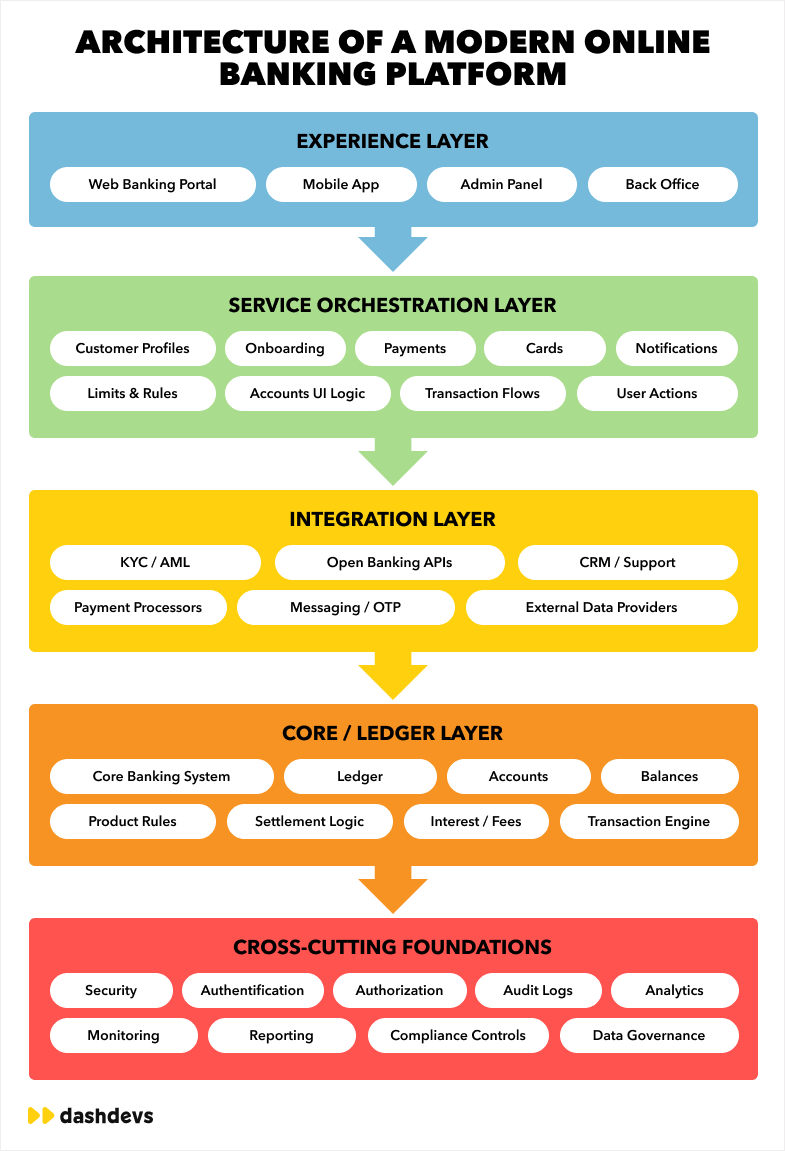

Architecture-first evaluation criteria

The best digital banking platforms in 2026 — and the online banking platforms built on composable cores — separate concerns into layers that can evolve independently:

| Layer | Components | Why it matters |

|---|---|---|

| Experience | Web, mobile, admin console | Brand and conversion — should stay thin |

| Orchestration | Workflows, limits, approvals, notifications | Where differentiation lives |

| Integration | Core, KYC/AML, cards, fraud, open finance | Determines provider swap cost |

| Data + security | Audit trails, IAM, event streams | Compliance evidence and AI readiness |

Designed as a monolith, every change is risky. Designed with clear seams, change becomes a capability — which is what composability actually means in procurement conversations.

Digital banking platform providers that hardwire vendors into flows create commercial lock-in: you accept the pricing and roadmap you are given. Adapter-based integration preserves optionality — the same principle behind fintech API integrations for scalable, compliant products.

For banks connecting legacy cores to modern channels, see bank APIs in context and open banking infrastructure patterns — both clarify where the digital layer sits relative to connectivity and compliance.

Who needs which type of platform

| Buyer | Primary need | Platform bias |

|---|---|---|

| Licensed digital bank | Auditability + channel modernization | Enterprise digital layer or modular custom |

| Fintech bank / challenger | Speed + iteration | Modular neobank stack, foundation layer, or white-label with escape plan |

| Virtual bank (no branches) | Lean ops + digital-only CX | Mobile banking platform plus orchestration layer |

| EMI / payment institution | Fraud ops + evidence trails | Platform with strong admin and monitoring |

| SME / corporate banking | Entitlements, approvals, bulk pay | Workflow-depth platforms — not retail-only |

| Embedded finance | Compliance-ready minimal UX | Orchestration-first architecture |

| Regional bank | CX upgrade without core swap | Digital layer on existing core |

Consumer online banking examples — direct-to-consumer neobanks and retail apps — illustrate what good UX looks like, but they are not vendor platforms you license. Other online banking examples in the SERP cover personal deposit accounts; this guide covers institutional software. Confusing the two produces RFPs that compare Chase Mobile to Backbase.

Build vs buy vs white-label: practical filter

| Route | Best when | Watch for |

|---|---|---|

| White-label | Market validation, standard workflows | Vendor constraints on provider choice |

| Enterprise vendor platform | Bank modernization, stable ops model | Program length, slower iteration |

| Modular / custom | Differentiation in workflows | Upfront architecture investment |

| Hybrid | Speed now, flexibility later | Clear plan for what you extend vs replace |

Teams launching a digital bank often start hybrid: modular foundation, prove economics, extend onboarding and risk logic as markets prove. See how to build a digital bank and how to start a neobank with vendors and APIs for how this maps to licensing paths.

For white-label market context, compare top white-label digital banking software solutions — category depth varies more than pricing suggests.

Common mistakes when choosing a platform

- Treating UI polish as platform strength — ask how support resolves disputes without engineering.

- Ignoring integration lock-in — assume you will swap KYC, issuer, or connectivity vendors within 24 months.

- Underestimating compliance workflows — KYC is not a one-time step; monitoring and case management are ongoing.

- Choosing for MVP only — the platform shapes cost-to-serve at 100k+ users.

- Assuming all white-label stacks are equal — some are branding-only; others are modular foundations.

63% of users abandon fintech bank onboarding when the process is too complex — a reminder that platform choice affects conversion and wasted acquisition spend, not just engineering timelines.

Security, business banking, and what comes next

Security in online banking platforms means auditability under pressure — MFA, device binding, immutable logs, fraud monitoring wired to ops workflows — not marketing claims about being the most secure electronic banking stack.

Business banking raises the bar: multi-user entitlements, approval chains, bulk payments, reconciliation exports, and treasury-style connectivity views. A retail-only internet banking platform cannot be retrofitted cheaply when SME accounts arrive.

Forward-looking digital banking platforms assume embedded finance distribution, AI-assisted operations, stronger identity primitives, composable cores, and multi-rail money movement. Online banking platforms that cannot abstract rails and produce evidence trails will feel dated within one product cycle.

Onboarding remains the hinge — see from digital onboarding to daily banking for why KYC orchestration is a unit-economics decision. Operationalize with KYC services and structured product discovery before engineering locks scope.

In Summary

The best online banking platforms in 2026 are not the ones with the longest feature slide — they are the ones that match how your institution runs: composable enough to swap vendors, deep enough in ops tooling to scale without linear headcount, and architected for ISO 20022, open finance, and AI-assisted operations.

If you are a bank or fintech builder, shortlist digital banking platform providers and online banking platform providers by category fit first, then run the seven-point framework above. If you are a consumer looking for the best place to open a personal account, this is the wrong guide — and the SERP has plenty of those.

Choose the platform that makes change cheaper over time, not the one that demos best on day one.

Share article