How to Integrate BLIK Payments: Architecture and Use Cases | DashDevs

March 11, 2026

Summary

- BLIK is Poland's leading bank-app-based payment method. It covers e-commerce payments, POS acceptance, phone-number transfers, ATM operations, one-click checkout, and recurring payment models under one domestic scheme.

- For merchants and fintechs, the commercial case is simple: better checkout relevance in Poland, less dependence on international card rails, strong customer familiarity, and access to a payment habit already built into mobile banking apps.

- For engineering teams, BLIK is more than another checkout button. A solid rollout needs payment orchestration, asynchronous status handling, mobile UX design, reconciliation, refunds, monitoring, and clear ownership between merchant, PSP, and bank-side players.

- Most companies do not connect to BLIK directly. They usually integrate through a PSP, acquirer, or orchestration provider that offers BLIK alongside other payment methods.

- The hardest part of a BLIK launch is rarely the API call itself. It is choosing the right product variant, getting the customer flow right, and making sure operations are ready before live traffic starts.

If you’re building payment experiences for Poland, BLIK is not just another local method sitting next to cards. For a lot of customers, it is the familiar way to pay.

That has both business and technical consequences.

On the business side, BLIK is well past the point of being a niche option for early adopters. According to the official 2025 results published by BLIK, users completed 2.9 billion transactions worth PLN 441.5 billion, and the system ended the year with 20.7 million active accounts. E-commerce was still the biggest channel, but in-store payments, P2P transfers, and recurring use cases also kept growing. In plain terms, Polish consumers already know the flow, trust it, and often expect to see it at checkout.

On the technical side, BLIK is easy to underestimate. From the outside, it can look simple: show the BLIK option, collect a code, wait for confirmation, finish the order. In reality, a proper rollout touches much more than the checkout page. You need to choose the right integration model, design a smooth mobile flow, normalize asynchronous events, handle expirations and retries, reconcile settlements, and make sure your support team knows what to do when the customer approved the payment in their banking app but your system has not yet received the final success webhook.

In this article, we aim to pierce the veil on what BLIK is, how it works, and most importantly, our understanding of how to integrate BLIK from a practical perspective. This will include the pros and cons of this unique payment ecosystem, its applications, why it succeeded in Poland, its drawbacks, and a technical breakdown of its integration process.

What is BLIK? How Does it Work?

Let’s start by explaining what BLIK actually is. BLIK is a payment method that is (for now) exclusive to the Polish market. BLIK acts as an alternative to usual payment methods like international wallets and cards. The way it works is essentially, at checkout, a customer is prompted to choose a payment method, and BLIK would be one of the options. The customer would then be prompted to enter a BLIK code.

To retrieve a BLIK code, the customer must open their local Polish banking app, request a BLIK code, and then copy it into the designated field on the merchant’s website or app. From then on, the transaction would happen directly through the customer’s banking app, as they would subsequently receive a payment confirmation, which they may choose to confirm or decline.

Practical Applications for BLIK

As opposed to a plethora of online payment tools out there, BLIK boasts a long list of practical applications in both physical and digital ecosystems.

Using BLIK in Poland, users can complete online purchases, pay at physical point-of-sale terminals, withdraw cash from ATMs, and transfer money to other individuals. The ecosystem not only opens itself to a wide range of applications users may need, but also removes the need for third-party payment processing companies or applications.

Why BLIK Matters to Developers

BLIK, over the years, has positioned itself as the primary payment method in Poland. Merchants and developers who seek to enter the Polish market will most likely need to integrate BLIK into their payment scheme, which is a common requirement during fintech app development. Pls link fintech app development. Failing to do so may result in encountering lower payment conversion rates when serving Polish customers.

Why BLIK Dominates Payments in Poland

The Polish banking system boasts some of the most advanced mobile banking and payment solution ecosystems across Central and Eastern Europe. Due to a robust modern banking infrastructure, mobile banking adoption rates in Poland are among the highest around the world. This is due to early investments from the Polish central bank, alongside other banks, in the mobile banking ecosystem.

As a result, customers are rather comfortable and feel safe using mobile banking apps on a daily basis for a variety of purchases. This is where BLIK’s competitive edge shines; it has integrated itself with the local banking structure, allowing BLIK to work seamlessly through local banking apps.

Checkout Experience Advantage

As mentioned above, BLIK works with local mobile banking apps, removing the need for external apps or user interfaces. Users can simply use mobile banking apps that they’re already familiar with to commence any purchases or transfers. This not only enhances efficiency in steps.

The major factor at play here is trust. Since users/customers move on with payments using mobile banking apps that they use for other operations, the fear of scams or phishing attempts is reduced, rendering these customers more likely to commit to purchases. On top of that, each customer is sent a confirmation prompt where they may choose to accept or decline the payment/transfer, adding another layer of security without slowing down the process. In the meantime, there is absolutely no need for the disclosure of any card information.

How BLIK Payments Work

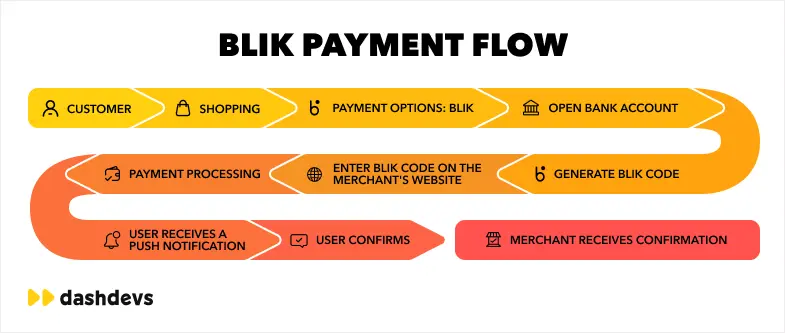

BLIK transactions rely on a simple authentication model built around temporary authorization codes generated within banking applications. Instead of entering card credentials, users open their bank’s mobile app and generate a six-digit BLIK code associated with the transaction. This code functions as a short-lived authorization token that allows the payment request to be linked directly to the user’s bank account.

A typical e-commerce BLIK payment follows a predictable sequence. During checkout, the customer selects BLIK as the payment method. The user then opens their banking application and generates a six-digit code. This code is entered into the merchant’s payment form, which sends the payment request to the processing system. The issuing bank then sends a push notification to the user’s banking app requesting confirmation of the transaction.

Once the user approves the payment in the banking application, the transaction is authorized, and the merchant receives confirmation that the payment has been completed. Because the authorization happens directly within the banking environment, the process typically takes only a few seconds.

Several characteristics distinguish BLIK payments from card transactions. The authorization codes are single-use and expire quickly, usually within a couple of minutes. Every payment requires explicit user confirmation through the banking app, and sensitive financial information such as card numbers is never shared with the merchant.

While this code-based interaction represents the most recognizable BLIK flow, the system supports several variations designed to reduce checkout friction and improve the experience for repeat customers.

Types of BLIK Payments

Although many users associate BLIK primarily with the six-digit authorization code used during checkout, the system supports several different payment implementations. These models are designed to support different transaction scenarios, ranging from one-time ecommerce purchases to repeat payments and tokenized payment flows.

Each implementation uses the same underlying infrastructure but differs in how the user authenticates the transaction and how the merchant stores payment credentials.

Standard BLIK (Code-based payments)

The standard BLIK payment flow is the most widely used implementation. In this model, the user opens their banking application and generates a temporary six-digit code associated with the transaction.

During checkout, the user enters this code into the merchant’s payment form. The bank then sends a confirmation request to the user’s banking app, where the transaction must be approved before the payment is completed.

Because the code is temporary and single-use, each transaction requires a new authorization code. This model works particularly well for one-time ecommerce purchases and is the most common BLIK integration supported by merchants.

BLIK OneClick

BLIK OneClick is designed to simplify repeat purchases by reducing the number of steps required during checkout.

During the first transaction, the user completes the payment using the standard code-based flow. The merchant can then be saved as a trusted merchant within the user’s banking application. Once this relationship is established, future payments can be approved directly through the banking app without requiring a new BLIK code.

This model reduces checkout friction for returning customers and improves the overall payment experience for frequent transactions.

Tokenized BLIK

Tokenized BLIK represents a more advanced implementation used primarily by platforms with ongoing customer relationships.

In this model, the merchant stores a BLIK payment token associated with the user’s account. When a payment is initiated, the system sends an authorization request directly to the user’s banking application, allowing the user to confirm the transaction without entering a code.

Tokenized payments allow platforms to streamline repeat transactions while maintaining strong authentication through the banking app.

BLIK Technical Architecture

Behind the user-facing checkout flow, BLIK payments involve several infrastructure components similar to those implemented in a modern payment orchestration platform. These include the merchant initiating the payment request, the payment service provider responsible for routing the transaction, the BLIK network coordinating authentication, the issuing bank verifying the payment, and the customer approving the transaction.

When a BLIK payment is initiated, the merchant’s system sends the payment request to its payment service provider. The provider communicates with the BLIK network, which forwards the request to the customer’s bank. The bank then prompts the user to confirm the transaction through the banking application. Once the user approves the payment, the authorization response travels back through the same chain to confirm the transaction for the merchant.

For most companies, the complexity of this infrastructure is handled by payment service providers. Platforms such as Stripe, Adyen, and regional PSPs manage communication with the BLIK network, allowing merchants to enable BLIK as another payment method without building their own payment routing infrastructure.

However, companies with their own payment orchestration layers or acquiring platforms may choose to integrate BLIK more directly. In these cases, developers must manage payment requests, authentication flows, and transaction confirmations themselves, which requires a deeper understanding of the underlying architecture.

BLIK Integration Methods

There are two ways of approaching the process of integrating BLIK integrations: companies and merchants can opt for integrating BLIK through PSPs or directly integrating BLIK through their own payment channels. Each approach offers its own set of pros and cons.

Integrating BLIK through a pre-existing payment service provider, utilizing their API, relies on their own communication channels to process any payment, cancellation or refund. While this approach seems both easier and faster, it renders merchants completely reliant on the PSP’s ability to continuously update their compliance, security, and settlement mechanisms.

On the other hand, merchants and companies can opt for direct BLIK integration. In a general sense, this approach is reserved for companies operating their own payment platforms or acquiring systems. To achieve this, developers interact with BLIK APIs directly, manage authentication flows, process webhook notifications, and handle transaction lifecycle events such as refunds and cancellations. Clearly, this approach requires more engineering efforts. However, the result is more control over payment orchestration and platform architecture.

Challenges of Integrating BLIK

BLIK is clearly widely used across Poland. However, it comes with its own set of challenges. Most of these challenges stem from the way the BLIK ecosystem evolved alongside traditional banking infrastructure. Developers may face several challenges during payment gateway integration, especially when working with legacy banking infrastructure.

Limited public documentation

Unlike many modern payment systems, BLIK documentation is not always publicly available. In many cases, technical documentation is provided only to approved partners or through payment service providers that already maintain integrations with the BLIK network.

This means that development teams often need to rely on onboarding processes, partner portals, or direct communication with BLIK support teams to access detailed technical specifications. While this approach helps maintain tighter ecosystem control, it can slow down early discovery and evaluation during the integration phase.

Legacy infrastructure and communication protocols

Parts of the BLIK ecosystem still rely on older infrastructure components that differ from modern REST-based payment APIs. Certain transaction operations (such as refunds, transaction queries, or cancellations) may require communication with SOAP-based endpoints.

These interactions can involve additional requirements such as encrypted requests, signed messages, and specific authentication mechanisms. Implementing and testing these integrations may therefore require additional development effort compared to newer payment systems.

Complex redirect and authentication flows

Due to particular browser behavior (such as cookie handling and redirect chains), some payment processes may require multiple redirects and browser-based interactions during payment authorization. As a result, they may not always be executed purely from backend services.

Our Hands-on Experience with BLIK

DashDevs encountered several of these complexities while integrating BLIK into our client’s payment orchestration platform. The client operates in the Polish market, where BLIK is one of the dominant payment methods, making support for the system essential for providing a complete payment experience to users.

One of the primary goals of the integration was to support BLIK payments within the client’s existing acquiring architecture without introducing inconsistencies across payment providers. The platform already supported multiple payment methods through a unified interface, so BLIK needed to fit into the same orchestration layer used for other payment services.

A major technical challenge involved implementing the BLIK redirect payment flow. The payment process required sending a POST request that triggered multiple redirects before reaching the final BLIK payment page. Because the request required secure parameters that could not be exposed to the client side, it could not be executed directly from the browser.

At the same time, executing the request purely on the backend was not possible either, because the payment flow depended on browser behavior such as cookie handling and redirect chains. To resolve this, the DashDevs team implemented an intermediate web page generated by the backend. When the client opened this page, it automatically executed the necessary request and redirected the user to the BLIK payment page, allowing the payment to proceed without exposing sensitive credentials.

Another architectural challenge involved differences between BLIK’s payment model and the client’s existing payment flow. The platform’s acquiring infrastructure expected transactions to follow a traditional authorization-and-capture sequence, while BLIK performs the full payment in a single step. To maintain compatibility with the existing architecture, the system had to simulate authorization and capture stages while the payment itself had already been completed.

The Future of BLIK

As things stand, BLIK only operates fully in Poland. However, it has lately entered the Slovakian market through its acquisition of the Slovak mobile payment company VIAMO. It is now available for customers of Tatra banka, one of Slovakia’s largest banks.

BLIK is also on its way to start its operations in Romania. The operator of BLIK received authorization from the National Bank of Romania to launch services in the country, although the expansion mainly focuses on payments within the e-commerce sector.

As BLIK expands across Central and Eastern Europe, it may become part of broader embedded finance platforms used by digital banks and fintech apps.

Summing up

As fintech platforms expand into new markets, supporting local payment methods becomes a critical part of building a successful financial product. In Poland, BLIK has become one of the dominant payment methods, offering a fast and secure way for users to complete transactions without sharing card details. For fintech platforms, enabling BLIK payments can significantly improve payment conversion rates and customer trust when operating in the Polish market.

However, integrating BLIK into a fintech platform is not always straightforward. The ecosystem involves several infrastructure components, including payment service providers, banking integrations, authentication flows, and transaction lifecycle management. In some cases, legacy infrastructure, limited public documentation, and complex redirect flows can make implementation more challenging than modern API-first payment systems.

For many fintech teams, the key challenge is not simply enabling a new payment method but integrating it into a broader payment architecture that can support multiple providers, payment types, and markets. A well-designed payment orchestration layer allows platforms to add new payment methods like BLIK while maintaining a unified infrastructure for processing transactions.

Share article