Fintech is hitting a new gear in 2025, and the stakes have never been higher. AI is set to revolutionize back-office operations, quantum computing will redefine security, and Central Bank Digital Currencies (CBDCs) are about to shake up global finance. These aren’t just trends—they’re the future.

In this article, we’ll explore what these trends mean for businesses, how they’re set to transform the financial landscape, and what you can do to stay ahead. If you’re ready to adapt, innovate, and lead, you’re in the right place. Let’s dive in.

Fintech Trends to Watch Out For in 2025

The fintech market will exceed $340bn in 2025, and by 2032, this figure will increase almost fourfold to reach $1,152 billion. Such rapid growth will provide a staggering compound annual growth rate (CAGR) of 16.5% and will push the rise of new fintech sectors and banking services.

Investors are increasingly valuing the decentralization and autonomy of fintech products. At the same time, fintech companies are collaborating more and becoming more selective about projects. Only businesses offering competitive, in-demand solutions can attract funding, making it essential to stay on top of fintech trends.

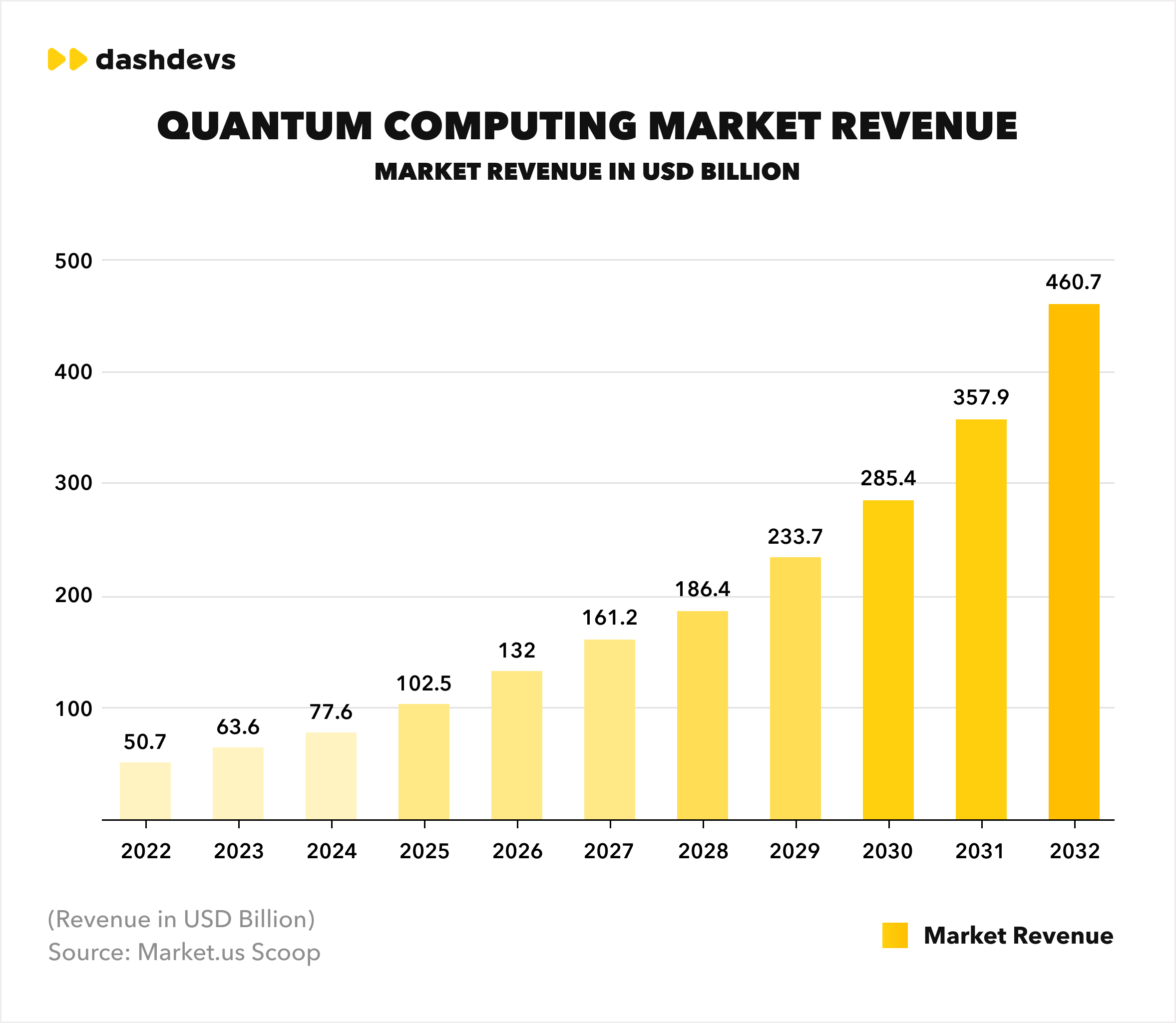

#1 Quantum Computing: The Next Frontier in Fintech

Quantum computing is a technology that processes information using the principles of quantum mechanics. Unlike traditional computers, which use bits (0s and 1s), quantum computers use qubits that can represent multiple states simultaneously. This enables them to solve highly complex problems much faster than traditional systems.

While still in its early stages, quantum computing is expected to significantly impact industries like finance, healthcare, and logistics in the coming years.

Key applications of cloud computing in fintech:

Risk management and portfolio optimization: Quantum algorithms can analyze vast datasets to optimize investment portfolios and improve risk assessments, enabling better decision-making for asset managers and hedge funds.

Fraud detection and prevention: Quantum computing’s processing power can detect fraud patterns in real-time, even across massive transaction volumes.

Cryptography and security: Quantum-resistant cryptography is becoming essential as quantum computers could potentially break current encryption standards. Financial institutions are now preparing for post-quantum security measures to safeguard sensitive data.

High-frequency trading (HFT): Quantum computing’s ability to process information at unprecedented speeds can improve high-frequency trading algorithms, giving firms a competitive edge in split-second decision-making.

Businesses investing in quantum computing early can achieve faster data processing, stronger security through quantum-resistant encryption, and enhanced decision-making capabilities, giving them a decisive competitive edge in addressing complex financial challenges and staying ahead of cybersecurity threats.

#2 Growing Adoption of Embedded Finance

Embedded finance is transforming how businesses operate, enabling them to integrate financial services directly into non-financial platforms. This fast-growing trend allows companies to handle monetary operations seamlessly within their ecosystems. With the embedded finance market projected to reach $7.2 trillion by 2030, its potential is undeniable.

Here’s how embedded finance is changing:

Seamless payments: Platforms like Netflix, Spotify, and Udemy streamline transactions directly within their services.

Diverse offerings: Beyond payments, embedded finance includes insurance, lending, banking, and wealth management.

For businesses, adopting embedded finance isn’t just an upgrade—it’s a competitive edge. By offering these integrated services, companies can:

Enhance the customer experience.

Increase client retention and loyalty.

Drive significant ROI through modernized financial solutions.

Staying ahead in this market means meeting customer expectations and leveraging embedded finance to thrive in 2025 and beyond.

#3 AI in Personal Finance: A Growing Market

The AI in fintech market is on an incredible growth trajectory, projected to expand from $11.8 billion in 2023 to $76.2 billion by 2033, with a CAGR of 20.5%. This surge is driving innovation across the personal finance sector, creating a prime opportunity for businesses to deliver AI-driven solutions.

AI tools are reshaping personal finance management, creating opportunities for businesses in these areas:

Smart budgeting: AI analyzes income and spending to help users plan realistic budgets, factoring in preferences and market trends.

Expense tracking: Tools categorize spending, highlight areas to save, and provide insights to optimize financial habits.

Investment support: AI offers personalized investment advice, helping users choose areas to invest, forecast returns, and manage risks.

Bill management: AI apps track bills, send timely reminders, and help users avoid late fees and penalties.

Financial planning: From short-term goals to long-term strategies, AI provides tailored advice, such as planning for a big move or retirement.

AI is simplifying money management for users while opening new avenues for fintech businesses. Companies that focus on delivering these AI-driven solutions can meet growing demand, enhance user experiences, and gain a competitive edge in this booming market.

#4 Central Bank Digital Currencies (CBDCs): Still on the Rise in 2025

Central Bank Digital Currencies (CBDCs) are creating exciting opportunities for businesses by introducing new ways to make payments, transfer money, and invest. These digital currencies, issued by central banks, are set to change how the financial world works.

According to Juniper Research, payments made using CBDCs will grow from 307.1 million in 2024 to 7.8 billion by 2031—an incredible 2,430% increase. This growth is driven by central banks protecting their control over money as digital currencies like stablecoins and card networks gain popularity. What CBDC means for businesses in 2025:

New opportunities: Businesses can expand by offering services that work with CBDCs in regions adopting them.

Global growth: Over 130 countries, including the USA and UK, are developing CBDCs, creating chances for fintech innovation.

Simplified processes: CBDCs make money management easier by removing the need for extra paperwork, like verifying where funds come from.

CBDCs are reshaping global payments and trade. Companies that adapt early can stay ahead of the curve and deliver better services to their customers.

#5 AI in the Back Office: Simplifying Operations in 2025

AI is transforming back-office operations, making them faster, smarter, and more efficient. By automating repetitive tasks and delivering real-time insights, AI helps businesses save time, cut costs, and focus on what truly drives growth. How AI adds value:

Cuts costs: Automating tasks like invoice processing and compliance checks reduces errors and operational expenses.

Improves decisions: AI-powered analytics provide actionable insights for better, faster decision-making.

Keeps you compliant: AI ensures adherence to regulations with automated monitoring and reporting.

Scales with your needs: AI adapts to your business needs, allowing you to grow without proportional overhead.

And now, let’s look at where AI can be used in the back office to enhance operational efficiency:

Document management: AI tools extract and organize data from contracts, invoices, and customer forms, saving hours of manual work.

Fraud detection: AI monitors transactions for unusual patterns, alerting teams to potential risks in real time.

Customer support operations: AI-powered chatbots handle routine queries, routing complex issues to the right teams for faster resolution.

Payroll processing: AI ensures accurate salary calculations, tax compliance, and timely payments, reducing HR workload.

In 2025, AI is more than a back-office tool—it’s a competitive advantage. By streamlining operations and opening new opportunities, AI helps businesses work smarter, not harder.

#6 Reincarnation of Decentralized Finance (DeFi)

After a sharp decline in 2023, decentralized finance is set for a comeback in 2025 and beyond. The DeFi market was valued at $14.35 billion in 2023 and is projected to grow at an impressive CAGR of 46.8% from 202 to 2032. This growth reflects rising trust in DeFi’s transparency and independence from central authorities.

Key opportunities for fintech:

Develop innovative DeFi products: Platforms for decentralized lending, yield farming, or exchanges.

Diversify offerings: Attract new users by providing alternatives to traditional finance.

Tap into new revenue streams: Leverage DeFi’s growing popularity and potential for higher yields.

Fintech companies that embrace DeFi can capitalize on this renewed momentum, expand their market reach, and position themselves at the forefront of decentralized finance innovation.

Regulatory Compliance Trends in Fintech Industry 2025

As the fintech industry grows, so does its responsibility to ensure security, transparency, and compliance with evolving regulations. The increasing accessibility of personal data and sophisticated cyber threats demand strict adherence to regulatory standards.

In 2025, several key regulations will shape fintech operations and trends:

The AI Act

Set to take effect in the European Union by 2025, the AI Act will classify AI applications into high, limited, and minimal risk zones. Fintech companies using high-risk AI must ensure:

Comprehensive risk management systems

Data governance to eliminate bias and errors

Robust documentation and human oversight This regulation aims to secure responsible AI use and protect consumer rights.

PSD3

Expected by 2025, PSD3 will introduce stricter rules for fintech operations, focusing on:

Strengthened client authentication and fraud prevention

Improved transparency in user terms and conditions

Enhanced data protection and reporting standards PSD3 will refine how fintech companies manage customer interactions and security.

Though DeFi operates outside traditional financial systems, 2025 will bring more detailed, country-specific regulations. DeFi companies must ensure compliance with:

Securities classifications and trading laws

Anti-Money Laundering (AML) directives

Tax obligations on virtual currencies

This evolving regulatory framework will guide DeFi growth while maintaining legal integrity.

Adapting to these regulations is critical for fintech businesses to thrive in 2025. By prioritizing compliance, companies can build trust, mitigate risks, and drive innovation in a highly competitive market.

Below is a list of the most common regulations that DeFi businesses should take into account:

What is regulated

Regulation in the USA

Regulation in the EU

DeFi tokens classified as securities, crypto-assets trading

Securities and Exchange Commission (SEC)

Markets in Financial Instruments Directive (MiFID), Prospectus Regulation

5th and 6th Anti-Money Laundering Directive (AMLD)

Smart contracts and electronic signatures

Uniform Commercial Code (UCC)

Electronic Identification, Authentication and Trust Services (eIDAS)

Taxation of virtual currencies

Internal Revenue Service (IRS) Guidance on virtual currencies

Value Added Tax (VAT) and income tax regulations

How a Fintech Development Provider Can Help You Keep Up With Fintech Trends in 2025

Navigating the fast-evolving fintech landscape in 2025 can be challenging. A fintech development provider offers expertise and resources to keep your business competitive while addressing technical, regulatory, and security requirements.

Access specialized expertise: Gain access to fintech professionals with deep knowledge of the latest technologies and trends. Get tailored advice on strategies, tech stacks, and market insights to achieve your business goals.

Accelerate time to market: Speed up your product launch with ready-made frameworks like FintechCore. Maintain your software’s uniqueness while benefiting from faster, efficient development processes.

Ensure compliance and security: Stay aligned with regulations like GDPR and PSD3. Implement cutting-edge anti-fraud measures and security protocols to safeguard your product and user data.

Flexible ddevelopment control: Choose your level of involvement—from hands-on collaboration to full project delegation. Benefit from real-time updates and transparency throughout the development process.

DashDevs brings a proven track record in fintech development. Our portfolio spans digital banking, payment apps, trading platforms, and more. Some of the recent fintech projects we developed are:

MuchBetter, an award-winning e-wallet preferred by global gaming sites

Downing, a sustainable investment management platform focused on renewable energy

Chip, an AI-based app that helps customers manage their savings and investments

Tarabut, an open-banking app that connects banks and fintech in MENA region

With access to industry expertise, faster time-to-market solutions, and robust compliance measures, you can focus on scaling your operations and delivering innovative financial products that resonate with your audience.

Summing Up

The fintech landscape in 2025 presents both opportunities and challenges. Staying competitive means leveraging advanced technologies, adhering to complex regulations, and ensuring secure, innovative solutions.

Partnering with a fintech development provider can help businesses navigate this complex landscape, ensuring faster time-to-market, adherence to compliance, and access to cutting-edge technologies. By doing so, companies can unlock new opportunities, meet customer expectations, and secure a leading position in the fintech space.

The future of fintech is being written now—are you ready to be part of it? Let’s build it together!

The forecast for fintech is associated with continued growth driven by technological advancements. Fintech will also see new regulatory changes and increasing consumer demand for digital financial solutions. In the future, fintech will continue shaping the future of financial services. It will offer more innovative and accessible solutions to consumers worldwide.

How fintech is shaping the future of financial services?

Fintech leverages new technologies to offer financial services in innovative formats. Through fintech applications, users can transfer money, make payments, invest, budget, take out loans, and conduct other financial operations via their smartphones instead of visiting traditional brick-and-mortar financial institutions. Additionally, fintech encourages traditional banks to adapt and collaborate with non-banking entities to remain relevant in an increasingly digital financial landscape.

What is the fintech industry outlook for 2024?

The fintech industry outlook for 2024 is promising. We will see continued growth in industries such as embedded finance, personal finance, CBDC, open banking, and DeFi. Additionally, we will see the emergence of new industry regulations that will shape the fintech industry landscape.

Is the fintech industry growing?

Yes, the fintech industry is growing at a rapid pace. If in 2023 the volume of the fintech market reached $340 billion, then by 2032 this figure will almost quadruple to reach $1,152 billion

What is the trend in fintech industry?

A trend in the fintech industry is the emergence of specific technologies or regulatory documents that change the products and services of fintech companies. Fintech businesses must monitor these trends to remain competitive and meet the demands of modern users.

Igor Tomych, fintech expert with

17+ years of experience. He launched 20+ fintech products in the UK, US and MENA region. Igor led the development of 2 white label banking platforms, worked with 10+ financial institutions over the world and integrated more than 50 fintech vendors. He successfully re-engineered the business process for established products, which allowed those products to grow the user base and revenue up to 5 times.