How to Build a Fintech App in 2026: The Definitive Guide

March 5, 2026

Summary

- The market is enormous and accelerating. The global neobanking market hit $992.85B in 2025. Embedded finance is on track for $454B by 2031. Digital wallets now account for 32% of all point-of-sale transactions globally. The opportunity is real, but so is the competition.

- "Fintech app" is not one thing. Digital banks, wallets, EMI-based neobanks, and embedded finance infrastructure each have different regulatory paths, partner stacks, and build timelines. Your architecture must match your product category from day one.

- Compliance is a design constraint, not a launch checklist. Teams that embrace auditability, reporting, and partner abstraction into their backend from the start move faster and spend less overall. Retrofitting compliance is one of the most expensive mistakes in fintech.

- The MVP must be regulation-ready. A fintech MVP without KYC, audit logs, and compliance reporting is not a real MVP, but a prototype that cannot go live.

- Tech stack decisions are business decisions. Your choice of backend architecture, integration patterns, and BaaS vendors directly affects your licensing options, scaling speed, and acquisition readiness.

- The market is shifting from standalone apps to embedded finance. Distribution now matters more than features. Your product may need to function as infrastructure for partners, not just as a consumer-facing app.

- Future-ready means acquisition-ready. Clean domain separation, data portability, and documented compliance controls are due diligence requirements that shape your exit options in 2027–2029.

Building a fintech app in 2026 is fundamentally different from building one five years ago. The infrastructure is more commoditised. The regulatory frameworks are more mature. The users are more demanding. And the competition is no longer coming from startups alone: incumbent banks, e-commerce giants, and SaaS platforms are all racing to embed financial services directly into their products.

What has not changed is that how to build a fintech app is still one of the most complex product and engineering questions a founder or CTO can face. Get the architecture wrong early, and you will spend years unwinding it. Get the compliance design wrong, and you will not launch at all.

This guide is designed for teams that are serious about building regulated fintech products: digital banks, wallets, EMI-based neobanks, lending platforms, and embedded finance infrastructure. It is not a generic app development tutorial. It draws on DashDevs direct experience building fintech platforms across Europe, MENA, and beyond, and on the real patterns that separate fintech products that scale from those that stall.

What Is a Fintech App

The term “fintech app” is often used loosely to describe anything with a payment button or a bank-branded colour scheme. That is a mistake that leads to badly scoped projects and underestimated builds.

For the purposes of this guide — and from the perspective of teams who actually build them — a fintech app is a regulated or semi-regulated digital product that handles financial flows, accounts, payment instruments, lending decisions, or investment activity. This includes:

- Digital banking and neobank apps (full or EMI-licensed)

- Wallets and account-based payment apps

- Lending and BNPL (Buy Now, Pay Later) platforms

- Investment, trading, and crypto custody apps

- Embedded finance infrastructure (APIs and orchestration layers for non-financial platforms)

A fintech app is not just a mobile UI. It is a regulated distributed system with compliance, orchestration, and integration layers that determine how fast you can grow, scale, and exit. Treating it as a standard app development project is one of the most common — and expensive — mistakes we see.

Fintech Market Overview: What the Numbers Actually Mean for Builders

Before diving into how to build a fintech app, it is worth understanding the market forces shaping why certain architecture decisions now matter more than others.

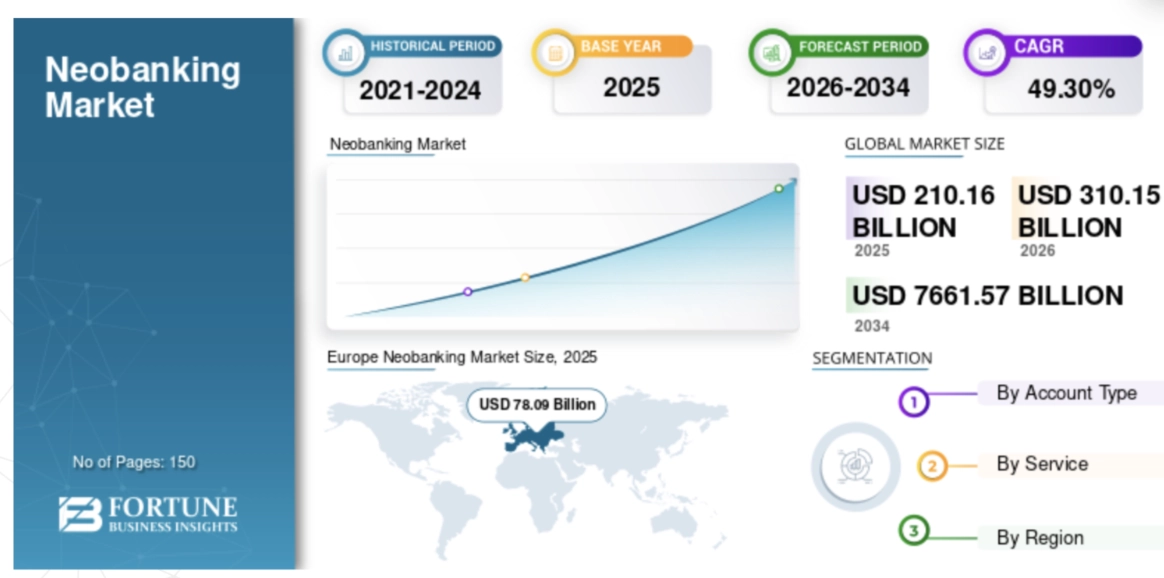

Neobanking: From Feature Race to Infrastructure Play

Global neobanking market projected to grow at 49.30% CAGR through 2030. Source: Fortune Business Insights.

The scale of this growth reflects a structural shift in consumer behaviour, not a temporary trend. Over 78% of consumers now prefer mobile banking services, with 65% of those users falling into the Gen Z and millennial segments. Meanwhile, 52% of businesses have adopted digital-only financial tools, and 45% of new bank accounts are opened via digital platforms.

What does this mean for product architecture? Teams cannot afford to build single-purpose digital banks and expect them to remain competitive. Modular architecture — the kind that allows you to layer investment, crypto, and embedded finance capabilities on top of core banking — is no longer a “Phase 2” consideration. It is a launch-day requirement.

Digital Wallets: Crossing the Majority Threshold

4.5 billion digital wallet users worldwide in 2025 — representing 54.9% of the global population, projected to reach 6 billion (70%+) by 2030 (Juniper Research)

Digital wallet adoption has crossed from experimentation into primary payment status. In 2025, 69% of US adults had used digital wallets in the past 30 days, with 38% using them weekly. Globally, digital wallets now account for 32% of all point-of-sale transactions — more than any other payment type.

Regional differentiation matters here. India leads global adoption at 90.8%, followed by Indonesia at 89.8% and Thailand at 89.0%. The US sits at 46.7%. For fintech builders, this creates a genuine strategic fork: teams targeting mature Western markets must architect for seamless integration with card infrastructure and gradual displacement, while teams building for high-adoption Asian or emerging markets must go wallet-first from day one.

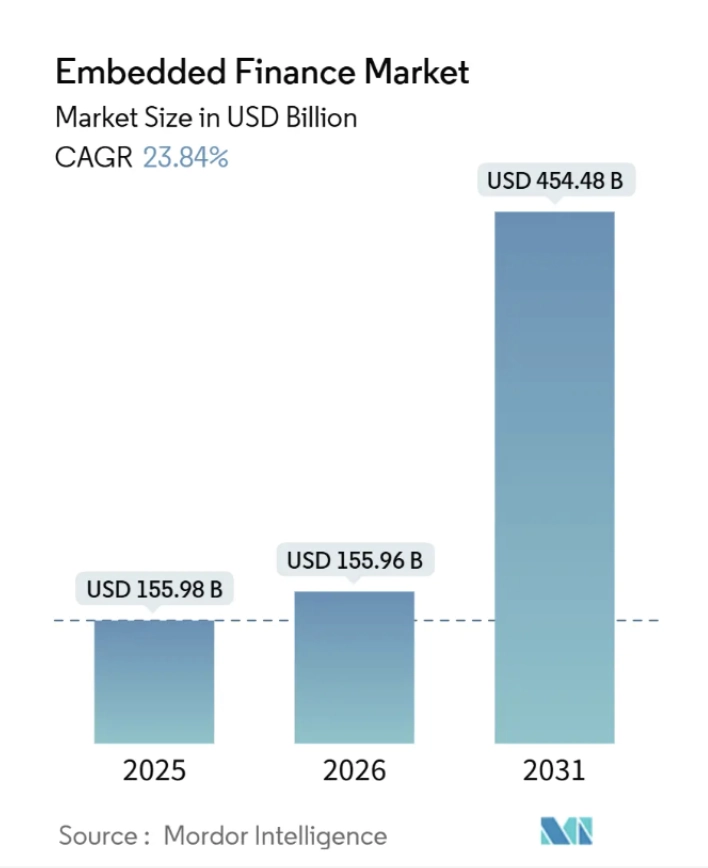

Embedded Finance: The Biggest Structural Shift in the Market

Embedded finance market projection by 2031, growing from USD 125.95B in 2025 at a 23.84% CAGR (GlobeNewswire)

Embedded finance — financial services integrated into non-financial platforms like e-commerce, SaaS, and marketplaces — is reshaping the entire logic of fintech product strategy. Distribution now matters more than feature completeness. Your product may need to function as infrastructure for partners, not just as a consumer-facing app. APIs and orchestration layers are no longer backend details; they are first-class product components.

Embedded finance market growth 2025–2031. Payments dominate at 43% share. Source: Mordor Intelligence.

AI in Fintech: From Enhancement to Operational Necessity

$30B AI in fintech market size in 2025 — with 88% adoption among top-performing fintech companies (WEZOM)

AI-powered fraud detection is reducing losses by 40% for teams that deploy it properly. 60% of digital lending decisions are now powered by AI, and 78% of customer queries are handled without human intervention. But this rapid adoption is creating new regulatory pressure: the EU AI Act is setting global precedent, with risk-based frameworks for model documentation, bias controls, and explainability expected to follow worldwide.

Teams building regulatory-ready AI architectures today — with audit trails and explainability from day one — gain an 18-24 month competitive advantage over those retrofitting compliance later.

Banking-as-a-Service: Consolidation and Compliance

BaaS market projection by 2031 is USD 65.78B, up from USD 28.96B in 2026 at a 17.83% CAGR (Mordor Intelligence)

The era of “growth at all costs” in Banking-as-a-Service is ending. Regulators are tightening scrutiny. ISO 20022 adoption is standardising payment messaging and compressing integration timelines, but also raising the bar for compliance documentation. Teams locked into single BaaS vendors face increasing switching costs and platform dependencies. Those architecting with provider abstraction layers maintain optionality and acquisition-readiness.

Main Fintech Trends Shaping Product Architecture in 2026

Understanding which trends are reshaping fintech app development architecture is not just interesting context — it directly informs the technical decisions you make on day one.

AI-powered fraud detection and personalisation have moved from optional features to operational infrastructure. Teams that skip this in their MVP often find themselves scrambling to retrofit it under live regulatory scrutiny.

Open banking and data portability are becoming default expectations. API-first architecture is no longer an advanced pattern — it is the baseline. Products that do not expose clean APIs cannot participate in the embedded finance ecosystem.

Modular platforms vs all-in-one vendors remain one of the most consequential decisions in fintech app development. All-in-one BaaS platforms offer speed in the short term but create deep vendor lock-in that limits licensing flexibility and exit options.

Compliance-as-code and automation are emerging as differentiators, not just efficiency tools. Teams that automate regulatory reporting, KYC workflows, and audit trail generation reduce operational overhead and reduce the surface area for compliance failure.

Multi-region licensing models are increasingly common for fintech products targeting more than one geography. Architecture that supports regional data isolation, multi-currency ledgers, and jurisdiction-specific compliance logic from day one avoids costly rebuilds later.

Architecture must be composable from day one. The teams that avoid platform dead-ends are the ones that design their integration layer as a business asset, not a technical afterthought.

Types of Fintech Apps: How the Build Differs

Not all fintech apps are built the same way. The product category you choose — digital bank, wallet, EMI-based neobank, or sustainability-focused platform — fundamentally shapes your architecture, regulatory scope, partner dependencies, and speed to market.

Digital Banking Apps

Digital banking apps aim to replicate core retail banking functionality in a fully digital experience: onboarding, accounts, cards, payments, and compliance workflows. They are infrastructure-heavy products that require robust core banking logic, high availability, regulatory reporting, and deep integration with banking rails and card processors.

In the Nexus digital banking platform case, DashDevs built a modular foundation for launching multiple digital banks across markets. The focus was on composable backend services, partner orchestration, and regulatory-ready architecture that allows new banking products to be rolled out without locking teams into rigid vendor stacks.

Wallets and Account-Based Apps

Wallets and account-based fintech apps focus on storing value, facilitating payments, and enabling transactional flows. They often have simpler regulatory exposure compared to full digital banks — but come with high operational complexity: payment processing, reconciliation, fraud prevention, and user expectations around speed and reliability.

In DashDevs’ digital banking platform case, the team built an account-based financial product with a strong emphasis on transactional integrity, real-time processing, and partner integrations with PSPs, KYC providers, and card networks.

EMI and Hybrid Neobank Models

EMI-based and hybrid neobank models sit between wallets and full digital banks. They often start under an e-money licence, partner with sponsor banks for safeguarding and accounts, and evolve toward deeper banking functionality over time. This creates a moving architectural and regulatory target.

In the Dozens (Project Imagine) case, DashDevs supported the development of a challenger banking product built on an EMI model, where product functionality, compliance requirements, and partner dependencies evolved as the business scaled. Hybrid models benefit from a modular backend that allows teams to swap providers and expand regulated scope without re-architecting the entire system.

Sustainable and ESG-Focused Fintech Products

Sustainability-driven fintech products combine financial functionality with environmental or social impact goals. This adds new data layers and reporting requirements on top of standard fintech infrastructure: ESG metrics, carbon impact tracking, sustainability-linked incentives, and additional transparency obligations.

In the sustainable banking platform case, DashDevs worked on a platform where financial features were tightly connected to sustainability goals and reporting, requiring careful data modelling and integration with third-party sustainability data providers alongside standard compliance and security requirements.

App type determines licensing path, compliance scope, partner stack, and time-to-market. Many fintech teams struggle not because of feature complexity, but because their initial architecture does not match the regulatory and partnership reality of their chosen product category.

Core Fintech App Features: MVP vs Scale

One of the most common mistakes in fintech app development is conflating “MVP” with “minimal compliance.” A regulation-ready MVP is not a feature-light product — it is a product that handles the critical flows correctly and can be demonstrated to regulators and partners from day one.

MVP (Regulation-Ready)

- Secure onboarding — KYC and KYB flows with identity verification and sanctions screening

- Account and transaction logic — ledger integrity, balance management, transaction history

- Payments, cards, and transfers — PSP and card processor integrations with real-time processing

- Ledger or balance logic — double-entry accounting patterns that support audit and reconciliation

- Audit logs and compliance reporting — structured logging and regulatory output from day one

Scale Stage

- AI fraud detection and real-time monitoring

Multi-tenant architecture for serving multiple markets or white-label partners from a single platform

High availability and fault tolerance — the engineering patterns that keep your product running under load and regional failure

- Partner orchestration layer — the ability to add, swap, and manage providers without rewiring your core

- Admin and operations tooling — internal dashboards for compliance, operations, and customer support

Tech Stack for Fintech App Development: What Actually Matters

Technology stack decisions in fintech are not just engineering choices — they are product, compliance, and business decisions. The wrong stack can block you from obtaining a licence, limit your ability to scale to new regions, or create technical debt that makes acquisition more expensive.

Backend Architecture

Event-driven, service-based backend architecture is the standard for production-grade fintech products. It provides the auditability (every event is recorded), the fault isolation (failures do not cascade), and the scalability (services scale independently) that fintech products require. Monolithic backends are not wrong for early MVPs, but they create migration costs as the product scales.

Databases

Fintech products require a clear separation between transactional databases (handling live financial data with ACID guarantees) and analytical databases (handling reporting, fraud analysis, and business intelligence). Mixing these in a single database creates performance bottlenecks and compliance risks.

Integrations: Banking Rails, KYC, PSPs, and Cards

Integration architecture is where most fintech apps either succeed or accumulate crippling technical debt. The key principle is provider abstraction: your core product logic should not be directly coupled to specific third-party vendors. An abstraction layer allows you to swap providers, negotiate better rates, respond to regulatory changes, and demonstrate vendor independence to acquirers.

Security

Encryption at rest and in transit, secrets management, role-based access control, and comprehensive audit logging are non-negotiable. In regulated markets, security architecture must be documentable: regulators and auditors expect to see evidence of security controls, not just claims.

Infrastructure

Cloud-native infrastructure with regional isolation is the default for fintech products operating across jurisdictions. Data residency requirements — which determine where financial data must be stored and processed — are increasingly strict. Designing for regional isolation from day one avoids expensive retrofit work when you expand to new markets.

For a deeper technical breakdown, read: Fintech Backend Architecture

Tech stack decisions lock in or limit your licensing strategy, scalability, and acquisition readiness. This is not a purely technical decision — it is a business decision.

Step-by-Step: How to Build a Fintech App

The following process reflects how production-grade fintech apps are built in practice — not the idealised version found in generic app development guides. Each step is sequenced to avoid the most common and costly mistakes in fintech app development.

Step 1: Define Your Fintech Product Scope

Before any engineering work begins, define your app type (digital bank, wallet, EMI, embedded finance), your target regions, and your regulatory exposure. These three variables determine everything downstream: licensing path, partner stack, infrastructure design, and time-to-market. Teams that skip this step and jump to wireframes inevitably rebuild when regulatory reality arrives.

Step 2: Run Market and Regulatory Research

Validate demand, test your monetisation model, and — critically — validate your compliance complexity early. In fintech, market research is not only product research. It is regulatory and partner feasibility research. Understanding whether you need an EMI licence, a payment institution licence, or a full banking charter in your target markets is a product decision, not a legal formality.

Step 3: Define MVP Scope (Regulatory-First, Not Feature-First)

Your MVP scope should be defined by what regulators and partners require to approve you for live operation — not by what looks good in a demo. Map compliance-critical features, partner dependencies, and operational workflows first. Features can be added; a backend architecture that does not support auditability cannot be easily retrofitted.

Step 4: Design UX for Regulated Flows

Fintech UX is not standard consumer app UX. Identity flows, consent management, compliance disclosures, and step-up authentication are regulatory requirements that must be designed carefully — both for user experience and for legal defensibility. Poor UX in these flows does not just hurt conversion; it can create regulatory exposure.

Step 5: Build Backend and Orchestration Layer First

The backend comes before the frontend in fintech. Specifically: your partner abstraction layer, event-driven business logic, and ledger patterns should be established before you invest heavily in UI. This ensures that your frontend is built on a stable, compliant foundation — and that partner swaps or integration changes do not require UI rebuilds.

Step 6: Implement Security, Availability, and Compliance by Design

Fault tolerance, audit logging, monitoring, and regulatory reporting are not features to be added after launch. They are design constraints to be built in from day one. Teams that treat them as “Phase 2” priorities routinely discover that retrofitting them into a live system is more expensive than the MVP itself.

Step 7: Launch with Controlled Distribution

Pilot with controlled user groups, operate in regulatory sandboxes where available, and collect early operational metrics before scaling. The goal is not to acquire users — it is to validate that your compliance, operational, and technical infrastructure holds under real conditions. Scaling with unresolved infrastructure issues is one of the fastest ways to trigger regulatory intervention.

Step 8: Scale Region by Region, Not Feature by Feature

Fintech product expansion is a different discipline from consumer app growth. Adding new banking rails, entering new licensing jurisdictions, or onboarding new partner types each require their own technical and compliance work. Teams that attempt to do this in parallel with feature development routinely find their engineering capacity overwhelmed.

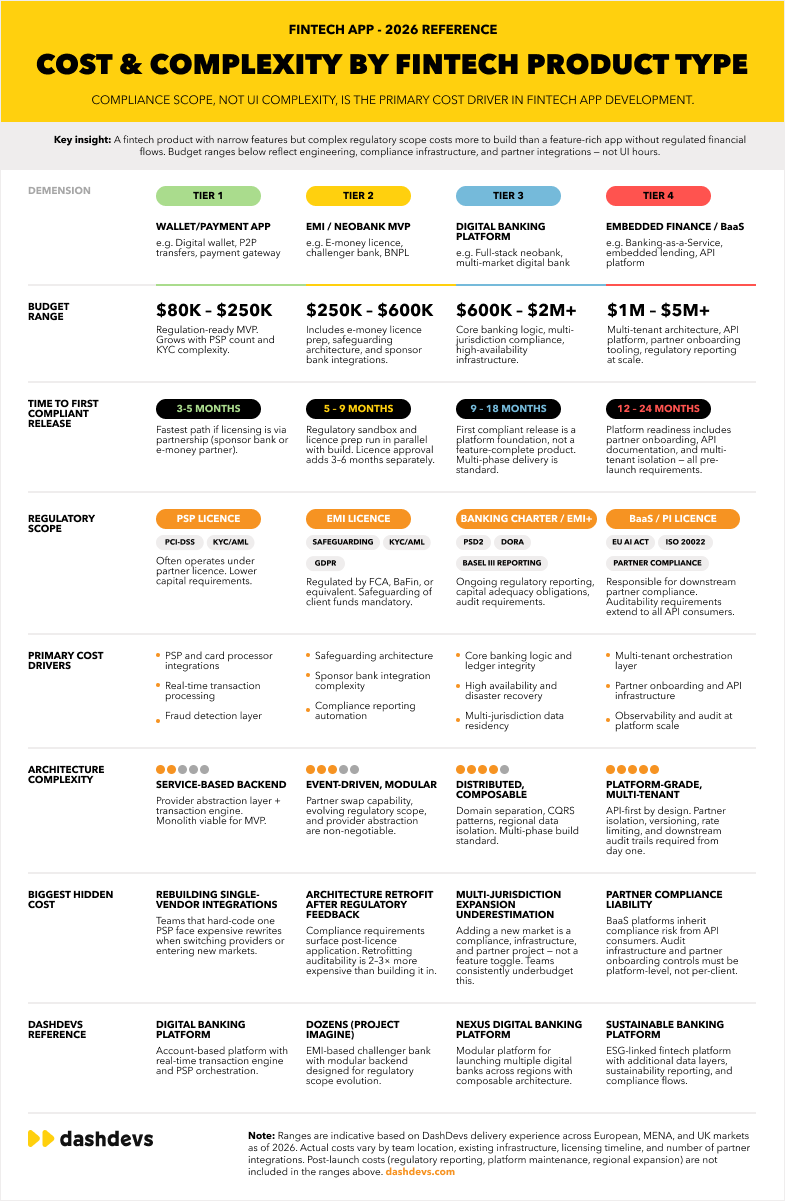

How Much Does It Cost to Build a Fintech App?

The honest answer is: it depends on regulatory scope more than feature scope. A payment wallet MVP and a full digital banking platform can both be called “fintech apps,” but their development costs differ by an order of magnitude.

| $150K–$500K | Typical range for a regulation-ready fintech MVP (narrow scope, single jurisdiction, 3–5 months) |

| $500K–$2M+ | Production-grade digital banking platform or multi-jurisdiction neobank (6–18 months to first compliant release) |

The main cost drivers — in rough order of impact — are:

- Compliance scope: licensing requirements, regulatory reporting, audit preparation

- Partner integrations: the number and complexity of banking rails, PSPs, KYC providers, and card processors

- Security and infrastructure: encryption, availability architecture, regional data isolation

- Admin and operations tooling: compliance dashboards, customer support tools, monitoring

- Post-launch evolution: ongoing regulatory reporting, platform maintenance, new jurisdiction expansion

The biggest hidden cost in fintech app development is rewriting architecture after regulatory feedback. Teams that front-load compliance design typically spend 30–40% less overall than teams that treat it as a retrofit problem.

For a detailed cost breakdown by product type, read: How Much Does It Cost to Build an App

How to Avoid Building the Wrong Fintech Product

The market is full of fintech products that were technically well-built but commercially or regulatorily wrong. Avoiding this outcome requires validating three dimensions before committing to architecture:

- Regulatory feasibility: Can you actually obtain the licences or partnerships required to operate in your target market? What are the capital requirements, timelines, and operational conditions?

- Monetisation model: Does your revenue model survive after partner fees, regulatory costs, and operational overhead? Many fintech unit economics look strong before factoring in the full cost of compliance and infrastructure.

- Go-to-market constraints: How will you acquire users or partners? In embedded finance, your distribution strategy may require API-first architecture from day one. In direct-to-consumer neobanking, your CAC and retention economics need to be modelled before you invest in platform scale.

Market research in fintech is not only product research — it is regulatory and partner feasibility research. The teams that skip this step are the ones we most often see rebuilding 12–18 months into a build.

Future Outlook: Where Fintech Apps Are Heading (2026–2030)

Understanding where the market is heading shapes the architecture decisions you make today. Here is where we see the next phase of fintech app development going — based on market data, regulatory direction, and what we are observing in active builds.

Embedded Finance Becomes the Default Distribution Channel

The trajectory is clear: by 2030, the majority of financial services interactions will happen inside non-financial platforms — e-commerce checkouts, payroll SaaS, mobility apps, and marketplace platforms. Standalone fintech apps will increasingly need to function as infrastructure providers, not just consumer products. The embedded finance market is projected to reach USD 454 billion by 2031, and the architectural implications are significant: API-first design, white-label capability, and multi-tenant orchestration will be table stakes for any fintech product with distribution ambitions beyond direct-to-consumer.

Banking-as-a-Service Consolidation Reshapes the Partner Landscape

The BaaS market is entering a consolidation phase that will reshape the vendor landscape significantly through 2027-2028. Several mid-tier BaaS providers will exit, merge, or pivot under regulatory pressure. For fintech builders, this reinforces the case for provider abstraction: teams that have built direct dependency on a single BaaS vendor will face costly migrations as the landscape shifts. Teams with clean abstraction layers will treat it as a swap, not a rebuild.

AI Regulation Creates Compliance Asymmetry

The EU AI Act is only the beginning. Risk-based AI frameworks are expected to proliferate globally through 2026–2028, with fintech among the highest-scrutiny sectors given the potential for algorithmic bias in credit decisions, fraud scoring, and identity verification. Fintech teams that have built AI systems with documentation, explainability, and bias monitoring will maintain their deployments without interruption. Those that have not will face mandatory remediation on a regulator-set timeline.

Super-App Architecture Expands Beyond Asia

The super-app model — one platform handling financial and non-financial flows — has been the norm in Southeast Asia and China for years. It is now migrating to European and North American markets, driven by the success of platforms like Revolut expanding beyond banking into lifestyle, travel, and commerce features. For fintech builders, this trend demands modular backend architecture: apps that cannot expand their service scope without re-architecture will lose ground to platforms that can add new verticals without disrupting existing flows.

Fintech M&A Intensifies — and Architecture Becomes an Exit Asset

As the market matures, M&A activity will continue to accelerate. Banks are acquiring regulated fintech platforms. Infrastructure providers are merging. Embedded finance specialists are being absorbed into larger ecosystem plays. The implication for product architecture is direct: clean domain separation, data portability, audit trails, and documented compliance controls are not just good engineering practices — they are due diligence requirements that directly affect acquisition valuation and timeline. Architecture decisions made today will determine exit options in 2027–2029.

Regulators Will Expect Stronger Observability and Auditability

The direction of travel in financial regulation is toward greater observability: real-time transaction monitoring, structured audit trails, explainable automated decisions, and documented risk management frameworks. Fintech products built with observability as an afterthought will face increasing friction as these expectations harden into requirements. Teams that build monitoring, logging, and audit infrastructure as first-class product components will have a structural compliance advantage over those that treat them as background infrastructure.

Future-ready fintech apps will be acquisition-ready architectures, not just user-facing products. The decisions you make about compliance design, vendor abstraction, and data portability in 2026 will directly shape your strategic options in 2028 and beyond.

Wrapping Up: How to Build a Fintech App Without Locking Yourself In

If there is one overriding lesson from years of building fintech products across licensing models, geographies, and product types, it is this: the architecture you choose in the first few months is harder to change than the features you build.

Teams that start with regulatory architecture — that treat compliance, partner abstraction, and auditability as design constraints rather than features — consistently ship faster, scale further, and exit better than those that treat them as secondary concerns.

The key takeaways for any team learning how to build a fintech app:

- Start with regulatory architecture, not with feature lists

- Design partner abstraction layers early — treat your integration strategy as a business asset

- Build for licensing evolution, not just your current regulatory status

- Avoid one-size-fits-all platforms that create vendor lock-in and limit exit options

- Treat compliance, monitoring, and observability as first-class product capabilities from day one

If you are at the stage of validating your fintech app architecture before committing to build — or if you are mid-build and starting to see the warning signs of technical debt — talk to DashDevs. We have built digital banks, wallets, EMI platforms, and embedded finance infrastructure across multiple markets. We know where the bodies are buried, and we can help you avoid the most expensive mistakes before they happen.

Share article