How to Build a Fintech or Payment App in 2026: Architecture, Gateways & Timelines

April 21, 2026

Summary

Executive summary

- Payment application development is not generic mobile work: your product sits between users, schemes, PSPs, and regulators—architecture and PCI scope decide what you can ship safely.

- Mobile payment app development succeeds when checkout, ledgering, reconciliation, and fraud are planned together; bolting on a gateway after UX is frozen is how teams buy expensive rework.

- Whether you build a P2P payment app, a merchant wallet, or an online payment application for ecommerce, your rails (cards, RTP, wallets, bank redirect) dictate timelines more than screens do.

- Choosing cost-effective payment gateways for mobile apps in 2026 means modeling total cost of acceptance—FX, disputes, retries—not only the headline gateway fee.

- Apple app developers should pick payment platforms that support Apple Pay, Hosted Fields or native token flows, and testable sandbox paths early; billing is a different dependency than checkout.

- Strong transaction APIs, idempotent webhooks, and observable settlement batches separate apps that scale from apps that hide money bugs behind pretty dashboards.

Learning how to build a payment app in 2026 is closer to shipping a regulated distributed system than to shipping a shopping-catalog app with a checkout button glued on. Users expect instant confirmations, predictable refunds, and clear balances; schemes, acquirers, and banks move money on their own calendars. Mobile payment app development fails when teams optimize the interface first and only later discover that their PSP cannot support the payout model, idempotency story, or dispute semantics the product promised.

This guide frames payment application development the way product and engineering leads actually run it: rails first, ledger and reconciliation second, user experience third—without pretending compliance is someone else’s problem after launch. It draws on DashDevs experience shipping payment-heavy products and integrations across Europe and MENA, alongside patterns we rely on when we design orchestration layers and resilient backends—see also our work on payment orchestration platforms.

What are pay apps?

People ask “what are pay apps?” in search because the category blends consumer wallets, merchant terminals, ecommerce checkouts, and standalone P2P brands. For this article, a payment app is any mobile or web application whose primary value is moving money safely: capturing or sending payments, storing balance or stored value where allowed, initiating payouts, and exposing refund and dispute workflows—not merely displaying a bank portal in a WebView.

That definition matters because an online payment application for ecommerce has different pressures (checkout conversion, retries, webhook storms) than a wallet built for QR or NFC acceptance in stores, and both differ again from building a peer to peer payment app where you optimize for sender–receiver clarity and velocity controls.

Pay apps compete on reliability and clarity as much as UX polish. When balances disagree with card statements—or payouts lag without explanation—users churn faster than they do over minor UI quirks.

Why mobile payment app development is a different discipline

Three constraints separate payment application development from generic consumer apps:

First, PCI and data minimization are architecture choices. Teams that postpone tokenization strategy often paint themselves into raw card-data handling nobody intended to own. Second, correctness beats cleverness: double charges, skipped settlement posts, or mis-keyed refunds are reputational incidents. Third, partners are part of your runtime: gateways, PSPs, open-banking APIs, card networks, and—in P2P—sometimes sponsor banks set limits on what “instant” can mean.

Before you compare vendors, align on vocabulary: our payment processor vs payment gateway breakdown explains capture paths versus clearing and settlement—labels blur when you buy an all-in-one PSP, but incidents still split across those roles.

Payments market context builders should internalize

Digital wallets are mainstream, not niche. Juniper Research projects digital wallet users exceeding six billion by 2030; globally, wallets already represent a large share of point-of-sale flows. That matters because users arrive with expectations trained by super-apps and large wallet brands—instant-looking authorizations, transparent pending states, and forgiving retries.

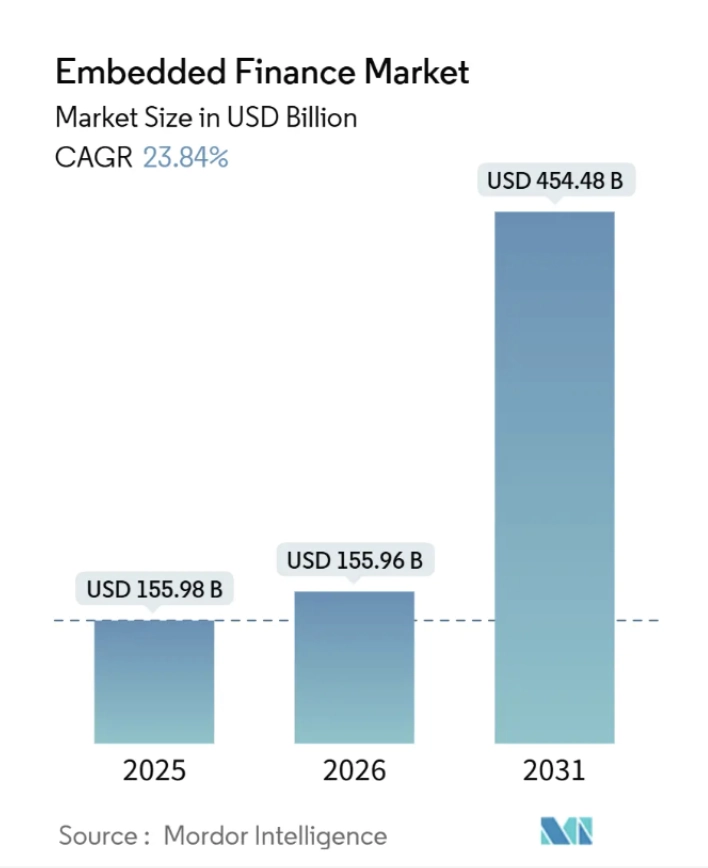

Embedded finance—payments inside commerce, SaaS, or mobility—is still reshaping distribution. Payments dominate embedded finance adoption; many “payment apps” succeed by meeting partners where checkout already happens. Source context and projections vary by analyst; treat headline CAGR figures as directional, not as specifications for your own backlog.

Types of payment apps—and how the build differs

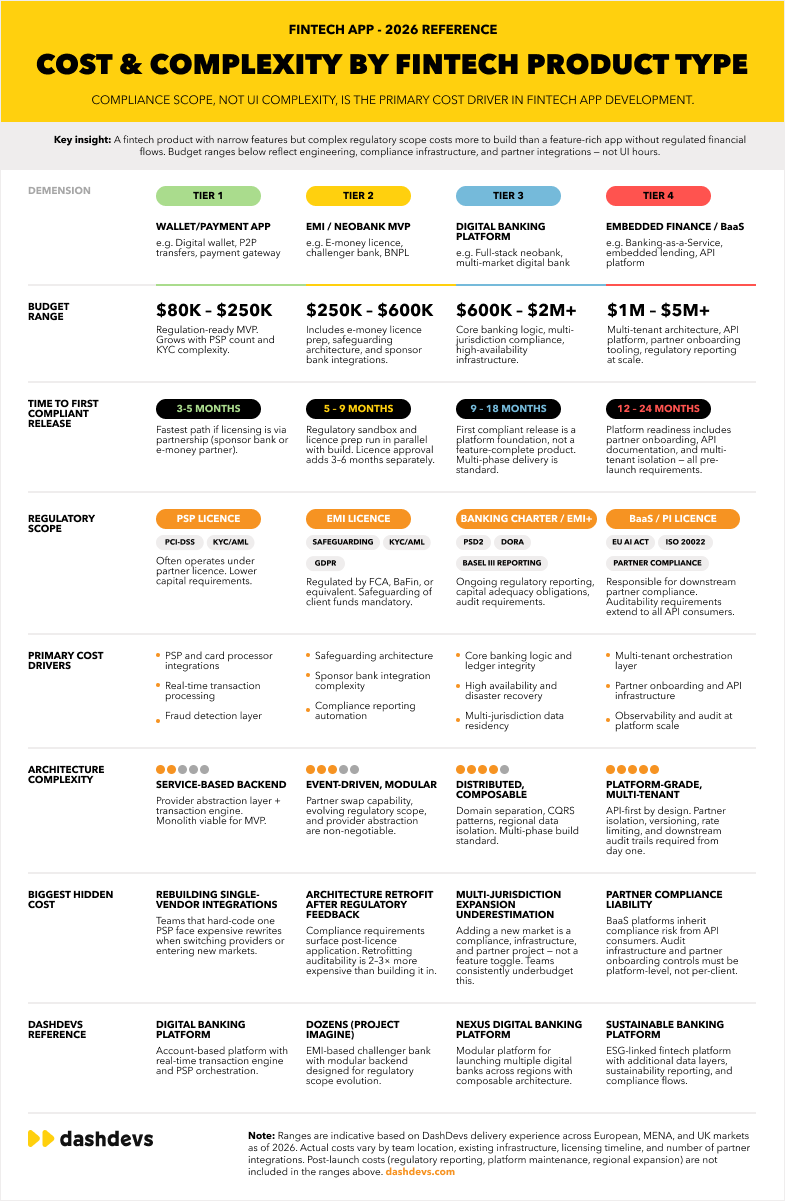

Payment is not one product shape. Before estimating scope for payment application development, classify what you are building:

Consumer wallets and super-wallet features emphasize stored balance or linked instruments, transfers, FX, rewards, sometimes cards. Complexity concentrates in ledgering, reconciliation, fraud, limits, and—where relevant—safeguarding models.

Merchant or small-business acceptance emphasizes capture quality, tipping and MOTO variants, reconciliation to ERP, chargeback tooling, and occasionally multi-location hierarchies.

Checkout-first ecommerce emphasizes conversion, retries, regional payment methods, and resilient webhooks—not only card fields.

Peer to peer (P2P) emphasizes instant-looking transfers between users, invitation graphs, velocity limits, and compliance around funds flow—often the hardest combination with the friendliest UX expectations.

How to build a P2P payment app people trust

Teams researching how to build a P2P payment app—or looking to build a P2P payment app with minimal rework—usually converge on the same pillars:

Define whether balances are bilateral ledger entries inside your platform alone, whether you rely on external RTP or card pushes, or whether you integrate with programs that mirror wallet balances under explicit rules. Nail identity and device binding early; P2P disputes are social as well as financial. Instrument everything: ambiguous “pending” states destroy trust faster than slightly slower confirmations.

Benchmark carefully when someone asks for “best peer to peer payment apps 2025/2026” comparisons—feature charts age quickly; focus your competitive review on disclosure, limits, dispute handling transparency, and how withdrawals work.

Online payment applications and omnichannel realities

An online payment application layered on ecommerce still has to survive peak traffic and noisy callbacks. Teams moving from desktop-first checkout to mobile payment app development should revisit timeouts, fallback payment methods, and fingerprinting flows—patterns we connect to broader electronic rails in our guide to electronic payment services.

MVP features payment apps cannot fake

Your MVP still needs genuine operational bones—not a slideshow:

- Identity and risk basics appropriate to your rail: lightweight for low limits, fuller KYC/KYB where regulation demands it (scope varies enormously by geography).

- Payments core: authorize/capture/refund semantics that match what your PSP exposes; payouts if your product promises them.

- Ledger or booking layer suitable to your promises—stored value apps cannot skip this even when the UI looks “simple.”

- Observability: webhook receipts, reconciliation hooks, searchable transaction IDs for support before you scale ads.

- Security baseline: TLS, secrets management, device integrity checks where relevant, RBAC on internal tools—patterns adjacent to broader high availability expectations even when your first release is small.

Scale-stage additions often include stronger fraud stacks, richer admin consoles, formal dispute desks, partner programs, multi-tenant rollouts (multi-tenant application patterns), and granular fee policies.

Payment gateways and PSPs for mobile stacks

Choosing among cost-effective payment gateways for mobile apps in 2026 is less about chasing the cheapest per-transaction line item and more about total landed cost:

| Cost bucket | Questions to pressure-test with vendors |

|---|---|

| Acceptance | Card-not-present vs in-app; regional methods; ACH/RTP/Open Banking rails |

| FX and cross-border | Who converts, when, and how disputes settle in multiple currencies |

| Fraud and RADAR-class tools | Per-review fees, thresholds, chargeback automation |

| Disputes and retries | Chargeback workflow APIs, representation tooling, webhook reliability |

| Reconciliation | Settlement batch formats, timestamps, timezone behavior |

| Ops | Sandbox fidelity, dashboard usability, incident communications |

Regional licensing and sponsor relationships often matter more than a vendor’s logo—especially when users ask about “best payment solutions for apple app developers 2026” scenarios where Apple Pay, Strong Customer Authentication, and local schemes intersect.

Transaction APIs, webhooks, and orchestration choices

Teams comparing “best transaction api for fintech apps” headlines should translate marketing into interfaces: synchronous authorization APIs, asynchronous settlement events, batch reconciliations, payouts APIs, disputes APIs, export formats. Weak transaction APIs quietly force ops teams into spreadsheets—the opposite of scalable payment application development.

If multiple PSPs or A/B failover matter, introduce orchestration deliberately—routing logic belongs next to ledger semantics so finance does not reconcile three divergent truths. Orchestration overlaps with concepts we walk through under payment processor vs gateway orchestration realities.

Apple App Store, Apple Pay, and IAP boundaries

Apple app developers hit two different worlds: payments for physical goods or services typically flow through PSPs and Apple Pay tokens; digital goods sold inside iOS apps may fall under Apple’s billing rules depending on category and region—misalignment here creates rework, not polish tickets.

When evaluating payment platforms for Apple app developers (2026), prioritize native Apple Pay UX support, documented token flows, issuer decline semantics you can expose to users calmly, sandbox parity with production behaviors, and clear separation between App Store receipts and PSP settlement reports.

Templates, SDKs, and accelerator assets

Builders searching for a pay application template or payment application templates should be precise: downloadable UI kits accelerate prototyping; they do not replace PCI scope decisions or ledger architecture. Where you need regulated rails out of the box, licensed SDK ecosystems and PSP-hosted mobile SDKs reduce raw card exposure—reference vendor docs directly rather than trusting unverified third-party snippets.

Similarly, phrases like free application for payment template highlight design shortcuts; production systems still need contractual coverage with PSPs, contingency handling for declines, and state machines that survive offline clients.

Tech stack priorities for secure payment apps

Backend. Event-oriented services remain the dominant pattern for observable money flows—see why in our fintech backend architecture overview.

Ledger and storage. Separate live transactional stores from analytic replicas; never let ad hoc analytics queries pin OLTP workloads during settlement windows.

Partners. Abstract PSP specifics behind ports/adapters—swap pressure is inevitable when pricing, coverage, or scheme rules change.

Clients. Hard-limit retries with idempotency keys; fingerprint devices thoughtfully; isolate sensitive tokens from analytics SDKs.

Infrastructure. Prefer regional deployments when customer data residency rules apply—especially for EU coverage.

Step-by-step: payment application development that survives launch

- Nail product semantics: consumer vs merchant vs P2P vs marketplace; currencies; settlement promises; withdrawal timing claims.

- Freeze regulatory posture with counsel—not blog posts—in each launch geography; licensing affects wallet and payout language massively.

- Pick rails and PSPs consciously; spike transaction APIs early with realistic declines and partial captures.

- Define ledger postings for charges, refunds, disputes, FX, fees, and payouts; reconciliation tests belong in CI, not slide decks.

- Design UX around honest states—“pending,” “won’t retry,” “refunded”—before visual polish budgets balloon.

- Pilot with constrained cohorts and instrument everything; scale marketing after settlement paths behave under load.

Payment apps rarely scale region-by-region “by copy-paste”; new schemes mean new reconciliation semantics—parallel work alongside features is normal, similar to disciplined expansion described in broader platform literature.

Timeline expectations

Rough calendar ranges—your mileage varies with licensing, rail count, and team maturity:

| Scope | Typical first production-ready horizon | Notes |

|---|---|---|

| Narrow payment MVP (single rail, focused geography) | ~3–5 months | Depends on onboarding depth and PSP readiness |

| Multi-method wallet / checkout expansion | ~6–9 months | Reconciliation complexity dominates |

| Marketplaces + splits + payouts | Often 9–12+ months | Ledgering + partner integrations compound |

Treat regulatory clocks—licensing sponsorship, scheme certification—as parallel streams that can gate calendar dates independently of engineering velocity.

Cost ranges (why payment apps aren’t priced like fitness trackers)

Honest budgeting anchors on rails and obligations:

| Tier | Illustrative investment band | What usually lands inside |

|---|---|---|

| Lean payment MVP | ~$150K–$500K | Core flows, PSP integration, reconciliation hooks, observability baseline |

| Broad wallet / multi-rail expansion | ~$500K–$900K | Additional methods, richer fraud/ops tooling, hardened ledger features |

| Enterprise-grade payout platforms | Often $900K–$2M+ | Complex splits, multi-region variants, heavier compliance surface |

Compare detailed hourly economics separately; start from how much does it cost to build an app when communicating with finance stakeholders.

Avoidable mistakes when you create a payment app

Skipping ledger semantics “until later” turns friendly MVPs into expensive migrations once partners or auditors insist on traceability—topics adjacent to disciplined multi-account design in products that mix balances with payouts (multi-account ledger system, when your roadmap crosses into wallet territory).

Optimizing purely for cheapest headline fees ignores dispute and FX drag—often the dominant surprise in landed costs.

Letting marketing promise instant settlement language without engineering agreement on PSP cut-offs practically guarantees quarters that are heavy on chargebacks.

Ignoring webhook idempotency and deadlock handling invites duplicate settlement posts—the worst class of bugs to explain to users.

Where payment apps head next

Distribution via embedded checkout and partner ecosystems continues to accelerate; wallets keep gaining POS share globally. Regulatory attention to transparency—clear pending vs settled balances, understandable dispute pathways—rises alongside adoption. Observability-first architecture is becoming table stakes, not heroics.

Teams that instrument money movement like product telemetry—structured events on every meaningful transition—recover faster from incidents and pass partner reviews sooner.

Closing guidance

If one lesson stands out when teams ask how to create a payment app successfully, it is this: rails and reconciliation define your timeline—screens do not. Mobile payment application development rewards teams that negotiate PSP contracts with engineering in the room, rehearse declines before launch marketing, and treat operational tooling as launch criteria alongside signup funnels.

Whether you pursue an online payment application for commerce, wallet-led acceptance, or a phased plan to build a peer to peer payment app with disciplined ledgering underneath, anchor your roadmap in observable money flows—then iterate UX with confidence.

Talk to DashDevs about PSP shortlists, mobile PCI scope, orchestration layers, and delivery plans grounded in production traffic—not slide assumptions.

Share article