How to Build a Micro-Investment Platform in 2026

How to Build a Micro-Investment Platform in 2026

March 5, 2026

Summary

- Micro-investing platforms enable users to invest small amounts automatically

- Popularized by apps like Acorns, Robinhood, Chip

- Built using modular fintech infrastructure

- Require brokerage integration, ledger infrastructure, compliance

- Typical build time: 6–12 months depending on scope

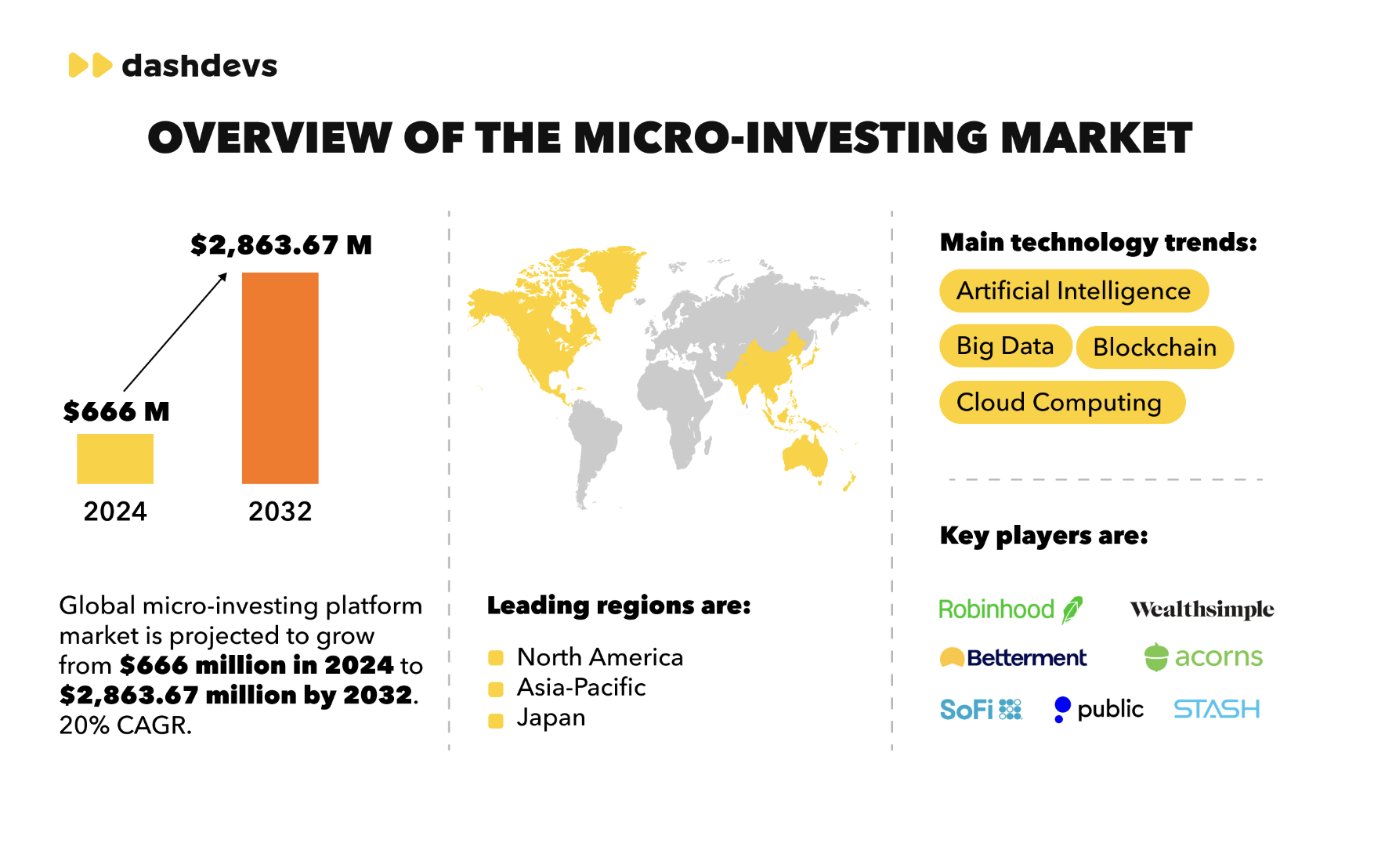

Over the last decade, investing has shifted from a niche activity dominated by institutions to something accessible from a smartphone. Today, millions of users can start investing with just a few dollars using a micro-investing platform.

Behind these simple apps sits a complex financial infrastructure that connects brokerage APIs, trading engines, custody providers, compliance systems, and portfolio analytics. Understanding these foundations is critical for fintech founders and product teams exploring how to build an investment platform or create an investment app.

To understand why micro-investing platforms are growing so quickly, we first need to look at the market trends driving their adoption.

Market Trends Driving Micro-Investing Platforms

The growth of the micro-investing platform category is closely tied to broader changes in fintech and wealth management. Several major trends are reshaping how individuals access financial markets and how companies approach building an investment platform.

Democratization of Investing

Historically, investing was limited to people who could afford brokerage accounts with high minimum balances. Traditional financial services required significant capital and often involved complicated onboarding processes.

Micro-investing platforms changed that.

Apps such as Robinhood, Acorns, Revolut Investing, and Trading212 removed many of the traditional barriers by offering:

- commission-free trading

- fractional share investing

- simplified mobile experiences

- automated investment tools

One of the most important innovations enabling this shift is fractional ownership.

Instead of buying a full share of a company like Apple or Tesla, users can purchase a fraction of a share with just a few dollars. The same principle now applies to:

- equities

- ETFs

- cryptocurrencies

- index funds

This approach dramatically lowers the entry barrier for new investors.

Behind the scenes, this model relies on API-driven brokerage infrastructure, which allows fintech companies to integrate trading capabilities into their apps without building a full brokerage from scratch.

This infrastructure makes it possible to create an investment platform much faster than in the past.

AI-Driven Investing and Automation

Another trend accelerating the adoption of investment apps is automation.

Many modern micro-investing platforms include robo-advisor functionality that helps users invest automatically rather than actively trading.

Common features include:

- automated portfolio allocation

- risk-based investment strategies

- automated rebalancing

- savings automation and round-ups

Artificial intelligence and data analytics also allow platforms to implement behavioral nudges that encourage consistent investing habits.

For example, some apps analyze spending patterns and recommend investing spare change or small recurring amounts.

These features make investing less intimidating for beginners while encouraging long-term financial discipline.

As a result, investment application development increasingly combines financial infrastructure with data-driven user engagement.

Embedded Investing in Financial Apps

A major shift in fintech is the rise of embedded investing.

Instead of building standalone brokerage apps, many fintech companies now integrate investing capabilities directly into existing financial products.

Examples include:

- digital banks

- savings apps

- budgeting platforms

- personal finance tools

A strong example of this model is the Chip savings and investment app. Chip began as an automated savings platform. Over time, it expanded into investing features that allow users to move seamlessly from saving money to investing it.

This evolution shows how fintech apps are becoming all-in-one financial ecosystems rather than single-purpose tools. For product teams thinking about how to create an investment platform, embedded investing opens the door to integrating wealth features into existing applications.

Rise of Multi-Asset Investment Platforms

Today’s users expect more than just stock trading.

Modern micro-investing platforms increasingly support multiple asset classes within a single application, including:

- equities

- ETFs

- cryptocurrencies

- commodities

- tokenized digital assets

This shift reflects the broader transformation of financial infrastructure toward multi-asset investment platforms.

A good example of this architecture can be seen in the digital assets trading platform case.

This project demonstrates how modern fintech platforms can combine traditional assets and digital assets within one unified trading environment.

For companies exploring how to build a trading platform or create an investment app, supporting multiple asset classes is quickly becoming a competitive requirement.

Why These Trends Matter

The combination of democratized access, automation, embedded finance, and multi-asset infrastructure has created the perfect environment for micro-investing platforms to thrive.

As financial technology continues to evolve, companies that successfully combine simple user experiences with robust backend infrastructure will be best positioned to capture the growing demand for accessible digital investing.

What Is a Micro-Investing Platform

A micro-investing platform is a type of investment application that allows users to invest small amounts of money automatically or incrementally. Instead of requiring large upfront deposits, these platforms enable people to start investing with just a few dollars.

The idea is simple: remove financial and psychological barriers that traditionally prevented people from entering the investment market.

Most micro investing platforms use automation to help users build portfolios gradually through features such as:

- Spare change investing – rounding up everyday purchases and investing the difference

- Recurring investments – automatically investing a fixed amount on a weekly or monthly basis

- Automated portfolios – allocating funds into diversified assets based on risk profiles

For example, when a user buys coffee for $3.60, the platform might round the transaction up to $4.00 and invest the remaining $0.40.

Over time, these small contributions accumulate into meaningful investment portfolios.

Some of the most well-known micro-investing platforms include:

- Acorns – pioneers of round-up investing

- Stash – combines investing education with fractional shares

- Chip – integrates savings automation and investing features

- Trading212 – offers fractional investing and commission-free trading

These platforms make investing accessible to people who may not have previously considered themselves investors.

Micro-Investing vs. Other Investment Platforms

Although micro-investing apps share infrastructure with trading platforms, their user experience and purpose are very different.

| Platform Type | Description |

| Micro-investing platforms | Focus on small recurring investments and automated portfolio growth |

| Trading platforms | Designed for active traders making frequent buy/sell decisions |

| Wealth management platforms | Provide portfolio advisory, financial planning, and long-term investment strategies |

Micro-investing apps prioritize simplicity and automation, while trading platforms emphasize execution tools and market access.

If you’re interested in how traditional trading apps are structured, read the article on how to create a stock trading app.

Understanding this difference is important when planning investment app development or evaluating how to build an investment platform that targets beginner investors.

Why Companies Build Micro-Investing Platforms

The growth of micro-investing platforms is not just driven by consumer demand. It is also fueled by strong business incentives for fintech companies, banks, and digital platforms.

For many organizations, adding investment features unlocks new revenue streams while strengthening customer engagement.

New Revenue Streams

One of the main reasons companies invest in building an investment platform is monetization.

Micro-investing platforms generate revenue through several models:

- Trading commissions on transactions

- Asset management fees on managed portfolios

- Premium subscriptions for advanced features and analytics

For example, many platforms offer a free basic investing experience while charging a monthly fee for features like automated portfolios, tax optimization tools, or advanced analytics.

Because these revenue models scale with user growth and portfolio size, they can become significant long-term income sources.

Customer Retention and Engagement

Investment features significantly increase customer stickiness.

When users start investing through an app, they tend to check their portfolios regularly, follow market trends, and remain engaged with the platform.

This increased engagement leads to:

- higher user retention

- stronger lifetime customer value

- deeper financial relationships

This strategy is especially powerful for:

- neobanks

- personal finance apps

- savings platforms

By adding investing capabilities, these products evolve from simple financial tools into full financial ecosystems.

Instead of switching between different apps for banking, saving, and investing, users can manage their finances in one place.

Data-Driven Financial Products

Another strategic advantage of investment application development is access to valuable financial data.

Investment platforms collect insights about:

- portfolio allocation preferences

- trading behavior

- savings patterns

- risk tolerance

This information enables companies to build smarter financial products.

For example, platforms can use this data to provide:

- personalized investment recommendations

- automated savings strategies

- targeted loan or credit products

- insurance offers tailored to financial behavior

In other words, micro-investing platforms are not just investment tools — they are powerful engines for building data-driven financial ecosystems.

Together, these business drivers explain why so many fintech companies, banks, and startups are exploring how to create an investment platform or integrate investing features into existing products.

How Micro-Investing Platforms Work

While micro-investing apps appear simple on the surface, they rely on sophisticated financial infrastructure behind the scenes. A modern micro-investing platform combines compliance systems, trading infrastructure, brokerage integrations, and analytics to automate investing for users with minimal friction.

To understand how investment apps work, it’s helpful to break down the core technical components that power these platforms.

User Onboarding and Identity Verification

Every investment application begins with secure user onboarding. Because financial platforms must comply with strict regulations, users cannot simply create an account and start investing immediately.

The onboarding process typically includes:

- KYC (Know Your Customer) verification

- AML (Anti-Money Laundering) screening

- identity verification through documents or biometrics

- risk profiling questionnaires

Risk profiling is especially important in investment platforms. It helps determine the appropriate asset allocation for each user based on their financial goals and risk tolerance.

For example, conservative investors may receive portfolios weighted toward ETFs and diversified funds, while aggressive profiles may include higher exposure to equities or crypto assets.

Once onboarding and compliance checks are complete, the platform can move to the next critical layer: the investment engine.

Investment Engine

The investment engine is the core logic that powers automated investing within a micro-investing platform.

This component handles tasks such as:

- order execution

- automated portfolio allocation

- investment strategy rules

- portfolio rebalancing

For example, when a user invests $10, the engine determines how that amount should be distributed across different assets in their portfolio.

Over time, market movements may shift portfolio allocations away from their target structure. The investment engine automatically rebalances assets to maintain the desired strategy.

This automation allows users to build diversified portfolios without actively managing every trade.

To execute these transactions in real markets, however, the platform must integrate with external brokerage infrastructure.

Brokerage Integrations

Most fintech companies do not build full brokerage infrastructure themselves. Instead, they connect their investment platform to licensed brokers through APIs.

Popular brokerage providers include:

- Alpaca

- DriveWealth

- Saxo Bank

- Interactive Brokers

These providers handle trade execution, regulatory compliance, and market connectivity.

By integrating with brokerage APIs, companies can significantly accelerate investment app development while remaining compliant with financial regulations.

If you want to explore this topic in more depth, this guide explains the key players in wealth platform integrations.

Once trades are executed, the assets themselves must be securely stored and managed.

Custody and Asset Storage

After a trade is executed, the purchased assets must be stored safely.

This responsibility typically falls to:

- broker-dealers for equities and ETFs

- custodian banks for managed portfolios

- digital asset providers for cryptocurrencies

Custody providers ensure that client assets are securely held and legally separated from the platform’s operational funds.

This separation protects investors and is a key regulatory requirement when building an investment platform.

Once assets are stored, the platform must present investment performance in a way that users can easily understand.

Portfolio Analytics and Insights

The final layer of a micro-investing platform focuses on user-facing analytics.

Modern investment apps provide dashboards that help users track their financial progress through:

- portfolio performance charts

- asset allocation breakdowns

- risk indicators

- historical returns

These insights make investing more transparent and help users understand how their money is working.

A strong example of this approach is the investment platform intelligent analytics case. In this project, advanced analytics tools were built to help investors interpret portfolio performance and make informed financial decisions.

Together, these infrastructure layers create the foundation that allows micro-investing platforms to automate investing while remaining compliant and scalable.

Step-by-Step: How to Build an Investment Platform

Understanding the technology behind micro-investing platforms is only the first step. The next challenge is translating that infrastructure into a working product.

For founders and product teams exploring how to create an investment platform, the development process typically follows a structured framework.

Step 1 — Define the Product Model

The first step is deciding what type of investment product you want to build.

Common models include:

- micro-investing platforms focused on small automated investments

- trading platforms for active investors

- robo-advisors offering automated portfolio strategies

- hybrid platforms combining multiple investment models

Your product model determines both the user experience and the technical architecture of the platform.

Once the product vision is clear, the next step is establishing the financial infrastructure that will power trades.

Step 2 — Choose Brokerage Infrastructure

Every investment platform needs a way to execute trades.

Companies typically choose between:

- integrating with API-based brokerage providers

- partnering with a licensed brokerage firm

- obtaining their own broker-dealer license

For most fintech startups, API brokers provide the fastest route to market.

Once brokerage connectivity is established, the platform must manage financial transactions internally.

Step 3 — Build a Financial Ledger

A financial ledger is one of the most critical components of any investment application.

It tracks:

- user balances

- deposits and withdrawals

- executed trades

- settlement records

Accurate ledger systems ensure financial transparency and prevent discrepancies between platform records and brokerage systems.

With the ledger in place, the platform can begin executing trading logic.

Step 4 — Develop Trading Logic

The trading layer controls the lifecycle of every investment transaction.

This includes:

- order creation

- asset pricing

- execution confirmation

- portfolio updates

Trading logic must also handle error scenarios and ensure that orders remain synchronized with brokerage partners.

Once trading functionality is stable, regulatory infrastructure must be integrated.

Step 5 — Integrate Compliance Systems

Compliance is a fundamental requirement for any investment platform.

This includes:

- KYC identity verification

- AML monitoring

- regulatory reporting

- secure financial data storage

Integrating compliance systems early in the architecture helps avoid costly redesigns later.

With compliance in place, the platform is ready for its first public release.

Step 6 — Launch an MVP

The final step is launching a minimum viable product (MVP).

At this stage, the focus should be on:

- supporting a limited number of assets

- onboarding a small group of users

- validating trading infrastructure stability

Launching a controlled MVP allows teams to gather feedback, refine the product, and scale the platform gradually.

This iterative approach is the safest way to transform a concept into a fully operational micro-investing platform.

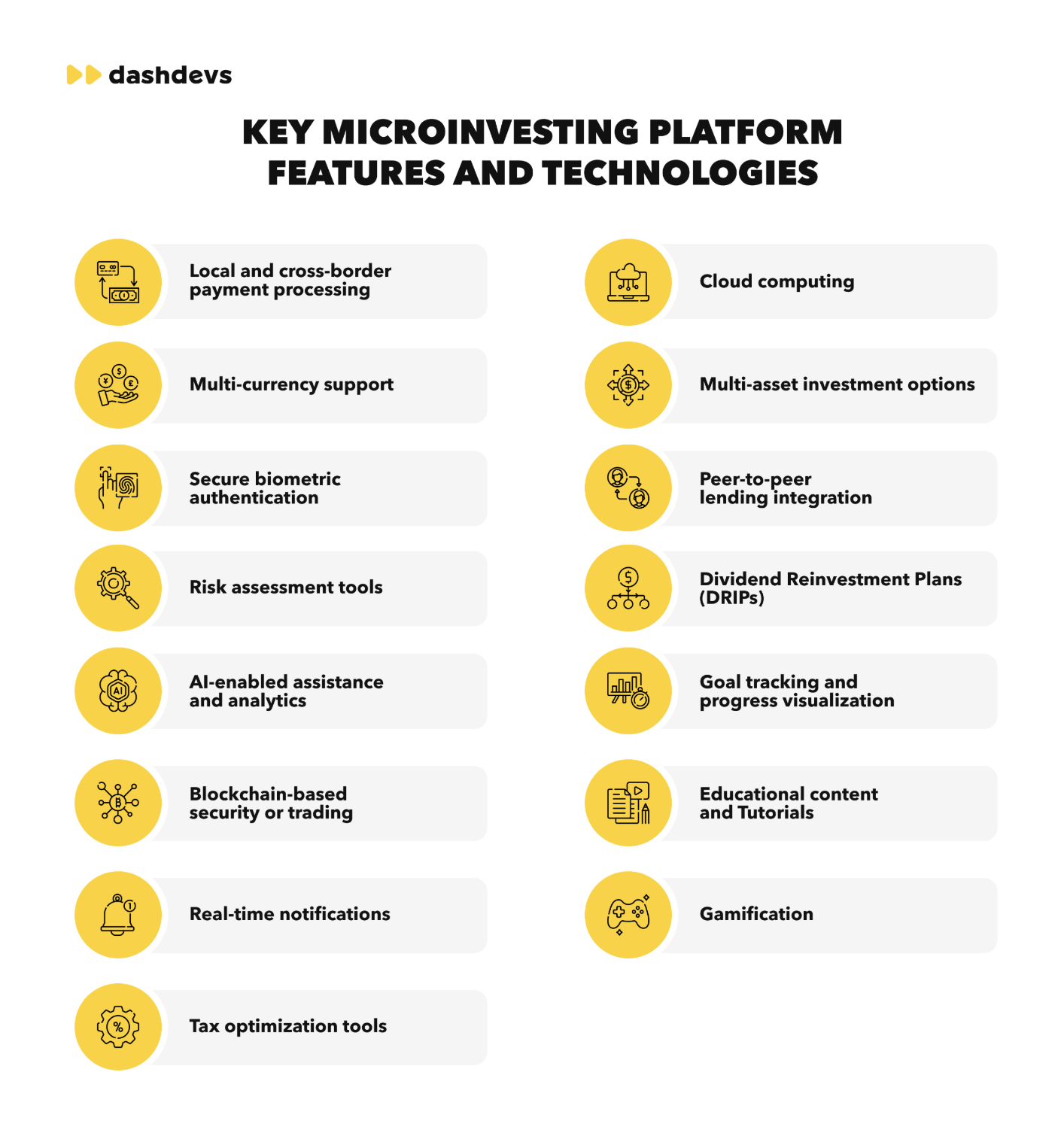

Core Features of a Micro-Investing Platform

While the backend infrastructure of an investment platform is complex, the user experience must remain simple and intuitive. Successful micro-investing platforms achieve this balance by combining automation with accessible financial tools.

Below are the core features commonly found in modern micro investing platforms.

User Onboarding and KYC

Secure onboarding is the first feature every investment app must implement.

Users must verify their identity before accessing investment services, ensuring the platform complies with regulatory requirements.

Fast onboarding experiences help reduce friction while maintaining compliance, making it easier for new users to begin investing.

Once a user account is verified, the platform can begin helping users invest automatically.

Automated Savings and Round-Ups

One of the most recognizable features of micro-investing platforms is round-up investing. This feature allows small amounts of money to be invested automatically during everyday transactions.

For example: A user spends $4.70 on a purchase. The platform rounds the transaction up to $5.00 and automatically invests the $0.30 difference.

Over time, these small contributions accumulate into meaningful investment portfolios. This approach makes investing accessible to beginners who may feel intimidated by traditional trading platforms.

Portfolio Management

Portfolio management tools help users monitor and understand their investments.

These features typically include:

- asset allocation dashboards

- diversification insights

- automated portfolio rebalancing

- long-term performance tracking

By simplifying complex financial concepts, these tools make investing easier for first-time users.

However, even simple portfolio management relies on sophisticated trading infrastructure behind the scenes.

Trading Infrastructure

Although micro-investing platforms simplify investing, they still rely on full trading platform development infrastructure.

Behind the scenes, the system manages:

- order routing

- trade execution

- clearing and settlement processes

This trading infrastructure ensures that investments are executed correctly and recorded accurately in the financial ledger.

For companies exploring custom trading platform development, this layer is essential for ensuring reliability and scalability.

Beyond trading capabilities, many platforms also focus on helping users understand how investing works.

Investment Education

Financial literacy is an important part of the micro-investing experience.

Many investment apps include educational tools designed to help users learn about financial markets.

Common examples include:

- short investment tutorials

- explanations of portfolio performance

- insights into diversification and risk management

These features empower users to make better financial decisions while increasing engagement with the platform.

Finally, platforms often use behavioral techniques to keep users consistently investing.

Notifications and Behavioral Nudges

Behavioral nudges play a major role in user engagement.

Micro-investing platforms often send notifications such as:

- reminders to invest regularly

- alerts about portfolio performance

- confirmations when round-up investments occur

These prompts encourage users to stay engaged with their investments and develop consistent saving habits.

Combined with automation and analytics, these features help transform micro-investing apps into long-term financial tools.

Technology Stack for Investment Platforms

Building a scalable micro-investing platform requires a reliable engineering stack that can process transactions, manage portfolios, and handle financial data securely. Most modern investment app development projects rely on cloud-native architectures and modular fintech infrastructure.

Backend Technologies

Backend services handle core investment logic, order execution, portfolio calculations, and API communication.

| Technology | Common Use |

| Java | High-performance financial systems |

| Go | Low-latency microservices |

| Python | analytics, AI, portfolio models |

| Node.js | API gateways and integration layers |

These services usually power the backend of a custom trading platform development stack.

Infrastructure Architecture

Modern cloud investment platforms are typically built using:

- cloud-native infrastructure (AWS, GCP, Azure)

- event-driven microservices for trading and analytics

- distributed ledgers to maintain transaction consistency

Cloud architecture allows platforms to scale transaction processing and handle market volatility without service interruptions.

Data Infrastructure

Investment platforms depend heavily on data pipelines.

They must process:

| Data Type | Purpose |

| Real-time market data | asset prices and trading decisions |

| Portfolio analytics | allocation, diversification, risk |

| Historical performance data | trend analysis and reporting |

Reliable data pipelines ensure users receive accurate portfolio insights.

Security Layer

Security is critical in investment application development.

Key components include:

- end-to-end data encryption

- fraud detection systems

- audit logs for compliance and reporting

Without these systems, financial platforms cannot meet regulatory requirements.

Regulatory Requirements

Launching a micro-investing platform requires strict compliance with financial regulations. These requirements vary by region but typically include licensing, KYC verification, and ongoing monitoring.

Licensing Requirements

Depending on the platform model and jurisdiction, companies may require:

| License Type | Purpose |

| Broker-dealer license | executing securities trades |

| Investment advisor license | providing portfolio advice |

Some startups partner with licensed brokers instead of obtaining licenses directly.

Compliance Frameworks

Investment platforms must follow regulatory frameworks that govern financial services.

| Region | Framework |

| European Union | MiFID II, PSD2 |

| United States | SEC regulations, FINRA rules |

These frameworks define requirements for investor protection, reporting, and risk management.

AML and KYC

All investment apps must implement strong AML and KYC procedures.

These processes ensure:

- identity verification for users

- transaction monitoring

- prevention of financial crimes

Compliance infrastructure should be integrated early when building an investment platform.

Monetization Models of Micro-Investing Platforms

For founders building micro investing platforms, a monetization strategy is just as important as product design. Investment platforms typically generate revenue through multiple sources. Combining several models allows companies to scale revenue alongside user growth.

Subscription Plans

Many investment apps offer premium features through subscription tiers.

Examples include:

- advanced portfolio analytics

- automated portfolio management

- AI-driven financial insights

Subscriptions create predictable recurring revenue.

Order Flow Revenue

Some platforms generate income through payment for order flow (PFOF). In this model, brokerage partners compensate the platform for routing trades through their exchanges.

This model became widely known through Robinhood. While controversial in some markets, it remains a significant revenue source for many trading platforms.

Asset Management Fees

Platforms offering managed portfolios often charge a small annual fee based on Assets Under Management (AUM).

Example structure:

| Portfolio Value | Typical Fee |

| Under $10k | 0.5% annually |

| $10k – $100k | 0.3% |

| $100k+ | 0.2% |

As user portfolios grow, these fees create scalable long-term revenue.

Spread Revenue

Platforms offering crypto or fractional trading may earn revenue from the spread between buy and sell prices. This is common in multi-asset investment platforms where market liquidity varies. For business owners, combining multiple monetization models can significantly increase profitability.

Micro-Investing Platforms Built by DashDevs

DashDevs has built multiple fintech systems that support investment platform development, trading infrastructure, and wealth analytics.

Below are real examples illustrating how investment technology can be implemented in production environments.

Multi-Asset Trading Platform

This platform supports trading across both traditional and digital assets.

Key capabilities include:

- crypto and digital asset trading

- high-performance execution infrastructure

- real-time order processing

The project demonstrates how modern investment platforms can combine traditional financial markets with digital asset ecosystems.

Wealth Analytics Platform

This platform focuses on advanced portfolio analytics.

Features include:

- portfolio performance visualization

- risk indicators and allocation insights

- intelligent investment recommendations

Analytics tools help users better understand their investment behavior and optimize strategies.

AI-Driven Investment Platform

This project demonstrates how AI-driven investing can enhance financial decision-making.

The platform includes:

- automated investment insights

- AI-powered portfolio analytics

- intelligent asset allocation

AI technologies are increasingly shaping the future of investment application development.

Savings and Investing Mobile App

Chip is an example of embedded investing.

The app combines:

- automated savings tools

- micro-investing features

- financial goal tracking

This model shows how fintech apps can evolve from savings tools into full wealth management platforms.

Build vs. Buy vs. Integrate

When companies decide to launch a micro-investing platform, they typically choose between three infrastructure strategies. Each approach has different trade-offs. Let’s consider them in detail.

Build From Scratch

| Pros | Cons |

| full product control | higher development cost |

| flexible architecture | longer time to market |

Building from scratch allows maximum customization but requires significant engineering investment.

White-Label Platforms

White-label investment platforms provide pre-built infrastructure.

| Pros | Cons |

| faster launch | limited customization |

| lower upfront cost | vendor dependency |

These solutions are suitable for companies prioritizing speed over customization.

API Integration Model

The most common approach is combining multiple fintech APIs.

Platforms integrate:

- brokerage APIs

- KYC verification services

- payment infrastructure

- market data providers

This model balances flexibility and speed.

For a related example of investment infrastructure, read our guide on how to build a crowdfunding platform.

Timeline and Cost of Developing a Micro-Investing Platform

Launching a micro-investing platform is a complex project that requires coordination across engineering, compliance, and financial infrastructure.

Development timelines depend on platform complexity, regulatory scope, and integration requirements.

| Stage | Timeline | Description |

| MVP investment platform | 6–9 months | core onboarding, brokerage integration, basic portfolio analytics |

| Full investment platform | 12–18 months | automation tools, analytics, multi-asset support |

The MVP stage focuses on validating the product and ensuring trading infrastructure works reliably.

Key Cost Drivers

Several factors influence the total cost of building an investment platform.

Major cost drivers include:

- brokerage and trading integrations

- compliance infrastructure (KYC, AML)

- portfolio analytics development

- security and audit systems

- cloud infrastructure and monitoring

Platforms supporting multiple asset classes typically require more advanced architecture and higher investment.

Long-Term Operational Costs

After launch, companies must plan for ongoing operational expenses.

| Operational Area | Purpose |

| Cloud infrastructure | hosting and scaling |

| Market data providers | real-time pricing |

| Compliance systems | regulatory monitoring |

| Security infrastructure | fraud detection and encryption |

Financial platforms require continuous maintenance, making operational planning just as important as initial development.

For business owners considering how to create an investment platform, the most successful strategy is usually launching a focused MVP, validating user demand, and gradually expanding the platform as adoption grows.

To conclude

Micro-investing platforms are reshaping the wealthtech landscape by making investing more accessible, automated, and integrated into everyday financial behavior. What once required brokerage accounts, large deposits, and financial expertise can now be done through intuitive mobile apps that invest small amounts over time.

For fintech companies, banks, and digital platforms, building a micro-investing platform creates an opportunity to expand product offerings, increase user engagement, and unlock new revenue streams through subscriptions, asset management fees, and financial insights.

However, launching a successful investment platform requires far more than a simple mobile interface. Behind the scenes, companies must integrate brokerage infrastructure, implement secure financial ledgers, manage regulatory compliance, and design scalable cloud architectures capable of handling real-time market data and trading activity. Businesses that approach development strategically — starting with a focused MVP and gradually expanding functionality — are best positioned to build reliable platforms that scale alongside user growth.

At DashDevs, we help fintech companies turn investment platform ideas into production-ready systems. Our team supports the full development cycle — from product architecture and brokerage integrations to secure ledger infrastructure and cloud-native trading platforms — helping businesses launch faster while meeting strict financial and regulatory requirements.

Thinking about building a micro-investing platform or adding investing features to your fintech product? Talk to DashDevs experts and explore how we can help you design and launch a scalable investment platform. Let’s get in touch.

Share article