How to Start a Neobank: Regulatory and Technology Roadmap

February 26, 2026

Summary

- Speed without architectural control creates long-term dependency.

- Licensing strategy defines your product limits more than UX ever will.

- Vendor orchestration becomes your biggest hidden complexity at scale.

- Modular infrastructure reduces re-architecture risk as you grow.

Building a neobank today isn’t about launching quickly with a plug-and-play platform. It’s about designing the right combination of sponsor-bank partnerships or licensed paths, modular infrastructure, and operational control—without creating long-term dependency on rigid vendor stacks.

The biggest misconception? A neobank is simply a sleek mobile app layered on top of someone else’s core. In reality, regulators expect resilience. Payment schemes require technical rigor. Compliance workflows must scale. And vendor orchestration quickly becomes complex if the architecture isn’t designed properly.

We’ve seen this in production. DashDevs helped launch one of the UK’s early fully licensed challenger banks—Dozens—orchestrating sponsor-bank integrations, compliance workflows, card issuing, and core banking infrastructure from scratch. That real delivery experience later became the foundation for Fintech Core, our modular neobank platform designed to accelerate compliant launches while preserving flexibility across banks, PSPs, and third-party providers.

If you’re evaluating your options, explore our neobank app development services to see how we design production-ready architectures for regulated fintech launches.

Let’s unpack what it really takes to build a neobank in 2026—without costly re-architecture later.

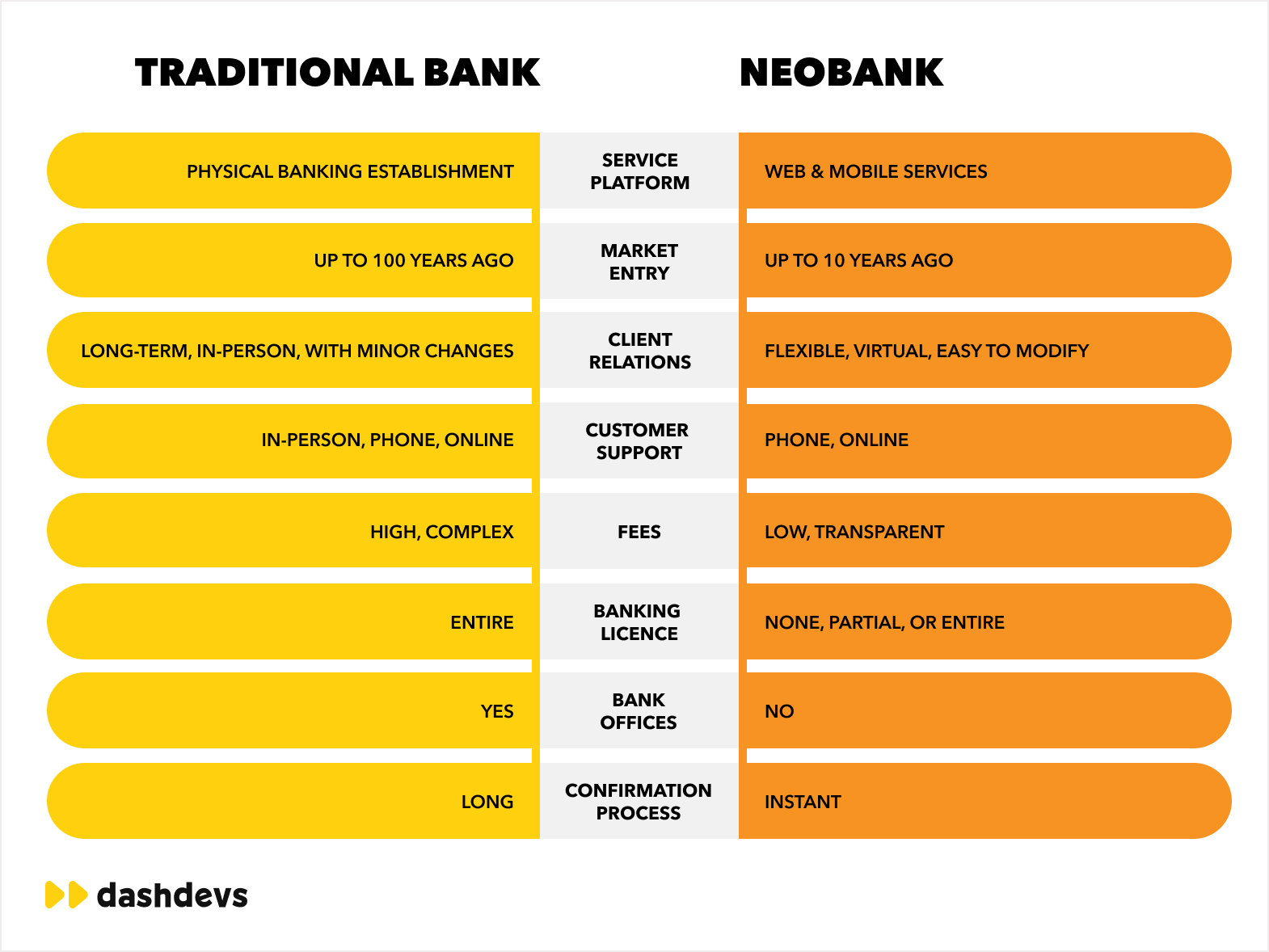

What Is a Neobank (vs. Digital Bank, Challenger Bank, Fintech App)?

The terms neobank, digital bank, and challenger bank are often used interchangeably. Structurally and legally, they are different.

The core distinction is simple: Who holds the banking license—and who carries regulatory responsibility?

That decision defines what customers can legally do inside the product.

| Model | Holds Banking License | Can Hold Insured Deposits | Can Lend from Own Balance Sheet | Speed to Launch | Regulatory Burden |

| Neobank (Sponsor Bank) | No | Via partner bank | Via partner bank | Fast | Medium (shared) |

| Neobank (EMI) | No (EMI only) | No (safeguarded funds, not deposits) | No | Fast–Medium | Medium |

| Fully Licensed Digital Bank | Yes | Yes | Yes | Slower | High |

| Fintech App | No | No | No | Very fast | Low |

Neobank (EMI or Sponsor-Bank Model)

A neobank is a branchless, mobile-first financial product that typically operates without a full banking license.

It usually works under:

- An EMI license, or

- A sponsor bank/BaaS partnership

In both cases, a regulated bank ultimately holds customer deposits.

Users can typically:

- Open accounts

- Send and receive payments

- Get debit cards

- Access budgeting tools

- Use lending products through partners

Users cannot (independently):

- Hold deposits directly under the neobank’s own license

- Access lending is funded from its own balance sheet

Examples include Chime (sponsor-bank model) and Revolut (hybrid structure across markets).

Neobanks are faster to launch—but architecturally dependent on partners.

Fully Licensed Digital Bank

A digital bank holds a full banking license but operates primarily online.

It can:

- Hold insured deposits

- Lend directly

- Operate under national deposit guarantee schemes

Examples include Monzo, Starling Bank, and N26.

This model requires higher capital and deeper regulatory oversight—but offers full operational control.

Challenger Bank

“Challenger bank” is a market term, not a legal category. It describes banks competing with incumbents through modern UX, pricing, or infrastructure. A challenger may be licensed or partner-based.

When building a neobank or digital bank, licensing determines architecture.

| Licensing Path | Best For | Trade-Off |

| Sponsor-Bank Model | Fast MVP, capital-efficient launch | Vendor dependency |

| EMI → Banking License Later | Phased growth strategy | Regulatory transition complexity |

| Full License from Day One | Long-term infrastructure play | Time and capital intensity |

| Multi-Market Phased Licensing | Cross-border scale | Operational complexity |

DashDevs supports both sponsor-bank neobanks and fully licensed digital banks through its neobank app development services, helping teams align regulatory structure with scalable, production-ready architecture.

Because in modern fintech, the difference isn’t just digital vs. traditional. It’s about licensing, control, and long-term ownership.

You may be additionally interested in exploring how to build a digital bank in another one of our blog posts.

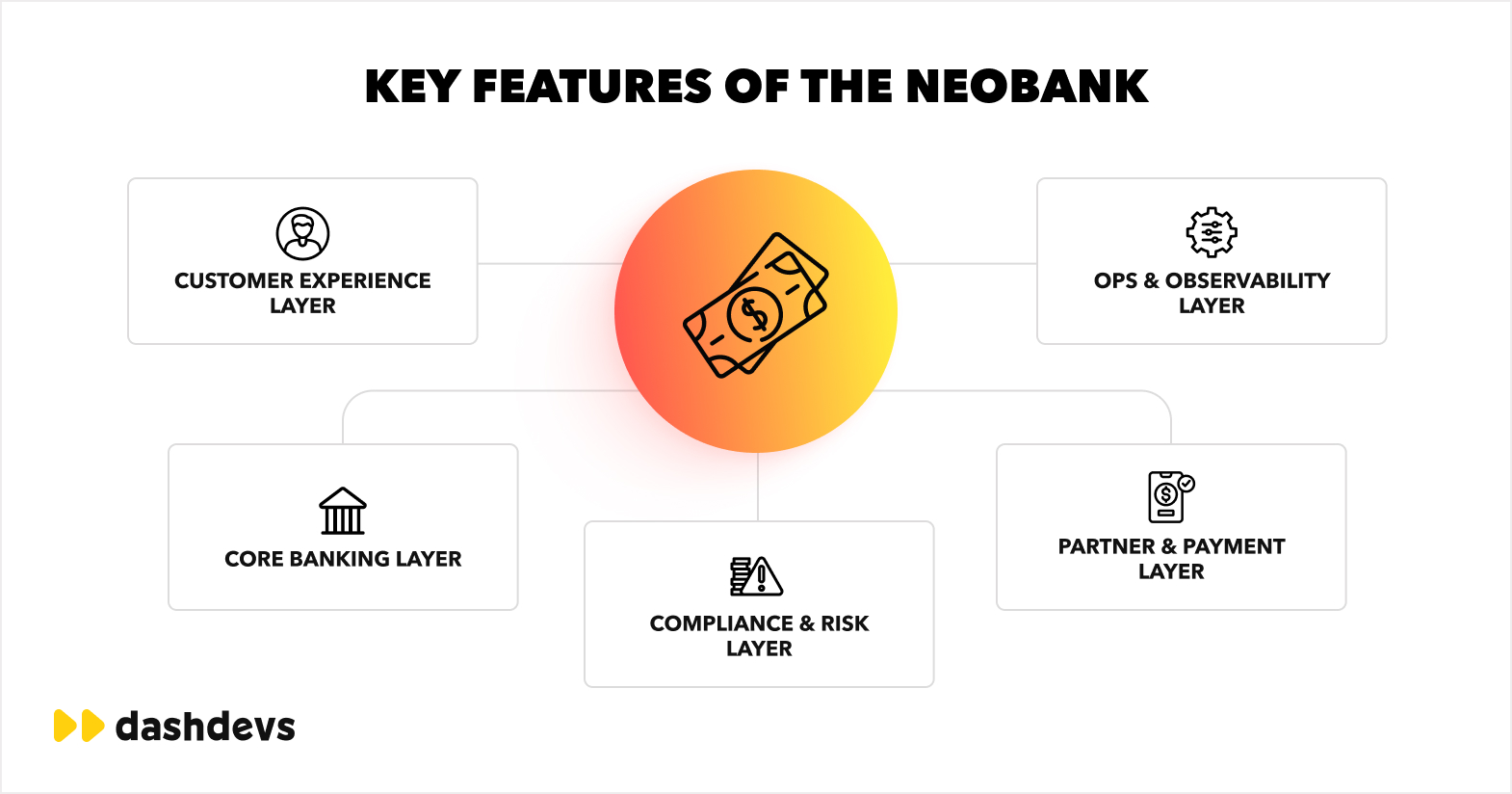

What Are the Key Features of Neobanks?

When discussing neobank features, it’s tempting to present a flat checklist: onboarding, cards, payments, notifications, and support.

In real delivery, however, features don’t live in isolation. They are tightly connected to ledger logic, compliance workflows, and sponsor-bank integrations. In production environments, feature velocity is defined by architecture—not just UI speed.

To understand what truly makes a neobank work, it’s more accurate to group capabilities into delivery layers.

1. Customer Experience Layer

This is the visible layer—what customers interact with daily.

Core features include:

- Digital onboarding and authentication (biometrics, 2FA, fast registration)

- Personal account management (profile controls, spending limits, internet limits)

- Card management (virtual/physical cards, freeze/unfreeze, dynamic CVV)

- Payments (P2P transfers, local and cross-border payments, contact sync)

- Transaction history and categorization

- Push notifications and alerts

- In-app customer support

This layer often includes differentiators such as cashback, savings goals, budgeting tools, referral systems, or crypto access.

However, these are experience features. They rely entirely on deeper infrastructure layers.

2. Core Banking Layer

This is the financial engine underneath the product.

It typically includes:

- Double-entry ledger system

- Account and balance logic

- Fee and interest calculation

- Limits management

- Multi-currency support

Without a properly designed ledger, transaction history becomes unreliable, reconciliation breaks, and compliance risks increase.

This layer determines whether the product can scale.

3. Compliance & Risk Layer

Regulation is not a side module. It is embedded in everyday banking flows.

This layer includes:

- KYC/KYB verification

- AML monitoring

- Transaction screening

- Fraud detection

- Audit trails

- Regulatory reporting

In regulated markets, onboarding and payments are directly tied to compliance checks. Feature expansion must move in parallel with risk controls.

4. Partner & Payments Layer

Most neobanks depend on external providers for:

- Sponsor bank integrations

- Card schemes

- Payment processors

- Open banking APIs

- BaaS platforms

This layer defines settlement logic, reconciliation processes, and geographic expansion capability. Poor orchestration here leads to operational bottlenecks later.

5. Operations & Observability Layer

Often overlooked at the MVP stage but critical at scale:

- Monitoring and alerting

- Vendor uptime tracking

- Incident management

- Reconciliation dashboards

- Reporting and analytics

Without strong observability, growth creates operational instability.

Real-World Delivery Insight

During the build of Dozens, everyday features like onboarding and payments were tightly coupled with compliance workflows, ledger architecture, and sponsor-bank APIs.

Feature delivery depended more on backend structure than on frontend design speed.

That experience later shaped Fintech Core—DashDevs’ modular neobank platform. Instead of treating onboarding, payments, compliance, and ledger as flat features, Fintech Core packages them as composable modules. This allows teams to scale, change partners, or evolve licensing paths without costly re-architecture.

Through our neobank app development services, DashDevs supports both sponsor-bank neobanks and fully licensed digital banks—aligning feature sets with compliant, production-ready infrastructure from day one.

Vendors vs. Platforms vs. APIs: What Actually Determines Your Neobank Architecture

When founders ask, “Should we use a white-label platform or build our own system?" they’re usually asking the wrong question.

The real question is how much control we need in 2–3 years—and how much complexity are we ready to manage today?

In regulated fintech, architectural shortcuts rarely stay invisible. They surface during audits, licensing transitions, geographic expansion, or scaling.

There are three common approaches. Each works—but under different conditions.

1. White-Label Platforms: Speed First

White-label platforms package onboarding, payments, cards, and compliance into a single stack. You integrate once and launch fast.

This approach makes sense when:

- You need an MVP quickly

- You’re validating demand

- You’re fundraising

But here’s the trade-off: the vendor owns the roadmap gravity.

As your product evolves, customization becomes limited. Switching providers becomes expensive. If you later move from a sponsor bank to a full license, re-architecture may be unavoidable.

White-label platforms optimize for speed of entry, not long-term flexibility.

2. API-First Orchestration: Controlled Flexibility

API-first orchestration means you integrate sponsor-bank rails, KYC providers, card schemes, and payment processors directly—while owning the orchestration and logic layer.

This model offers the best structural balance.

You can:

- Swap providers

- Expand into new markets

- Adjust compliance flows

- Control reconciliation

But this flexibility comes with responsibility. Integration debt builds quickly. Operational monitoring becomes critical. Reconciliation logic must be engineered, not improvised.

API-first is powerful—but only with strong architectural discipline.

3. Custom Core: Infrastructure Ownership

Building your own core (ledger + compliance engine + orchestration layer) is a long-term infrastructure move.

It makes sense when:

- You hold or plan to obtain a full banking license

- You want balance-sheet control

- You’re building for regulated scale

The trade-offs are clear:

- Longer timelines

- Higher capital requirements

- Greater regulator scrutiny

- Operational complexity

Custom core is not about speed. It’s about sovereignty.

What We Did in Production

When building Dozens, we deliberately avoided a rigid white-label stack.

We implemented API-first orchestration around sponsor-bank rails, combined with a custom ledger and dedicated compliance workflows. That structure reduced vendor lock-in and supported FCA scrutiny during licensing.

Everyday features like onboarding and payments were tightly coupled to ledger logic and compliance controls. Delivery speed depended on architecture—not UI velocity.

That experience later shaped Fintech Core’s modular orchestration and core design.

How to Build a Digital Bank or Neobank from Scratch?

As a fintech professional and CEO of a fintech company with over 13 years of experience and real-life knowledge developing a neobank from scratch in 9 months, I’m delighted to share practical insights on creating such a product since I already have the expertise you may need.

If you are wondering how to start a digital bank, this information will be useful for you as well. The next section will delve into the critical steps, complete with practical examples and advice.

Starting neobank app development from scratch is a journey filled with challenges and rewards. Remember to stay true to your vision, prioritize compliance and security, and deliver a seamless user experience. Neo banking is all about adaptability and innovation, and by following these steps, you’re on your way to making a significant impact in the financial industry.

Step 1. Define Your Vision and Mission

Step one in how to start a neobank is defining a clear vision and mission. Take inspiration from real-life success stories of fintech companies like Monzo, a UK-based neobank that aimed to make banking simple and accessible. Define your unique selling proposition (USP) and identify the problems your neobank will solve for customers. For instance, if you’re targeting millennials, create a bank that prioritizes features that enhance budgeting and offer real-time insights into spending.

To-do list:

- Take inspiration from real-life success stories.

- Define a unique selling proposition (USP).

- Identity problems your product will solve.

- Prioritize and customize features for user needs.

Step 2. Understand Regulatory Compliance

To launch a digital bank, neobank, or fintech solution, securing the right license is paramount. However, the landscape has shifted. In the past, only a full banking license would suffice. Today, you can operate a bank-like service with an EMI (Electronic Money Institution) or PI (Payment Institution) license.

These licenses allow you to offer many banking services, except granting loans and accepting deposits. Notably, Revolut, a prominent fintech player, hasn’t pursued a banking license in the US — a testament to the evolving norms. So, what’s the difference between EMI and PI licenses?

An EMI is an institution that’s authorized to issue electronic money.

Holding an EMI license allows you to:

- Issue and distribute electronic currency, enabling customers to store funds in an e-wallet for payments.

- Execute currency exchanges.

- Facilitate direct debit or credit transfers.

- Transfer funds to other customers.

- Handle withdrawals and deposits.

- Grant customers access to their account details.

On the other hand, PI stands for “Payment Institution.” A Payment Institution is a type of financial entity that is authorized to provide certain payment services without issuing electronic money. To understand well how to start a neobank you need to be well-versed with EMI and PI concepts.

By obtaining a PI license, you:

- Can’t issue electronic money.

- Can’t facilitate payment transactions (e.g., transfers).

- Can’t store money long-term.

In short, EMI = e-money + payments. PI = just payments.

There are distinct things EMI and PI cannot provide:

- Traditional bank accounts (only e-wallets are permissible).

- Deposit guarantees.

- Conduct international transactions.

Such services typically necessitate a banking license, which is more challenging to secure.

In essence, while a full banking license might be the traditional route, the EMI and PI licenses are viable alternatives for those looking to break into the fintech space without diving deep into traditional banking regulations.

To-do list:

- Start by researching the specific compliance requirements in your region.

- Seek legal and expert guidance.

Step 3. Assemble Your Dream Team

Neobank app development requires diverse expertise. Look for experts who understand fintech, such as former employees from established fintech firms or banks. Collaboration is key in this process, and an agile mindset is essential to adapt to unforeseen challenges. Consider hiring experienced professionals who have faced and conquered hurdles in fintech.

To-do list:

- Seek fintech experts with real experience (pay attention to projects they built — was it neobanks mobile app development or web development, which technologies they worked with, which integrations they set up).

- Prioritize collaboration and agile thinking.

- Hire professionals with a track record of overcoming fintech challenges.

Step 4. Focus on User Experience and Marketing

User experience (UX) can make or break your neobank. Take inspiration from Chime, a US-based neobank with a user-friendly mobile app. Ensure your digital channels are intuitive, secure, and accessible. Regarding marketing, remember the story of one of our customers — Pi-1, an award-winning BaaS platform from the UK. Their product wasn’t significantly different from others, but their success was driven by effective marketing, a modern-looking app, and excellent features, targeting banks and fintechs.

Establishing your brand’s look can achieve better market results and capture a larger market share. Effective communication of your brand’s unique value proposition can set you apart, even in a competitive landscape.

To-do list:

- Prioritize intuitive, secure, and accessible digital channels.

- Invest in user-friendly mobile app design.

- Emphasize effective communication of your unique value proposition in marketing.

Step 5. Prioritize Compliance and Security

Don’t underestimate the importance of compliance and security for neobank app development. A great example is Monese, a UK neobank, which learned this hard when facing regulatory challenges. The company’s initial difficulties might have arisen from insufficient Know Your Customer (KYC) and AML procedures.

Compliance involves adhering to various financial regulations and ensuring your neobank operates within legal boundaries. One critical aspect is KYC, which consists of verifying your customers’ identities to prevent fraud and financial crimes. Anti-Money Laundering (AML) processes are designed to detect and report suspicious activities that might indicate money laundering or other illicit financial transactions.

It would be best to stay updated on regulations like GDPR (General Data Protection Regulation) in Europe, which also governs the handling of personal data. Security is paramount in protecting customer data from threats, cyberattacks, and breaches. Consider partnering with cybersecurity experts who can help you implement robust security measures, encryption protocols, and monitoring systems to safeguard customer data and maintain compliance with industry standards.

Tip:

Although numerous security tools and measures are at your disposal, remember that they should be okay with your app users. Ideally, when it comes to how to start a neobank, security should work behind the scenes, ensuring a seamless and user-friendly experience, such as using video calls for identity verification or entering the last symbols of phone number calling.

To-do list:

- Prioritize compliance with financial regulations, including KYC and AML processes.

- Stay informed about data protection regulations like GDPR.

- Invest in robust cybersecurity measures to protect customer data from potential threats.

Step 6. Develop Your Business Processes

Start with robust business processes before diving into software development. Document how customers will onboard, how transactions will be processed, and how compliance procedures will be handled. This approach streamlines software development and ensures your operations run smoothly.

To-do list:

- Craft a seamless onboarding process to ensure customers can easily open accounts and use your services.

- Define efficient workflows for processing transactions to guarantee your digital channels are intuitive, secure, and accessible.

- Prioritize KYC and AML processes to prevent regulatory challenges.

- Create a secure data management system to handle customer information (use tools like Looker, Tableau, or Power BI).

Step 7. Choose the Right Software Engineering Approach

Engage engineers with fintech experience as they understand the intricacies. Ensure your engineering team can make informed choices and select technologies tailored to the neobanking environment. Without this expertise, engineers may inadvertently choose data types or technologies that could result in balance inconsistencies.

Choosing the right technologies tailored to the neobanking landscape is a basement for a successful product, the same as a base for the future house. Not all technologies suit fintech solutions; an ill-informed choice can lead to technical challenges. Your engineering team should be well-versed in selecting technologies that ensure scalability, security, and seamless integration.

#1 Cloud computing

- Examples: Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP).

- How it works: Cloud computing enables you to host your neobank’s infrastructure on remote servers, providing scalability, flexibility, and cost-effectiveness.

- Parameters for selection: Consider data security, compliance standards, scalability options, and ease of integration when choosing a cloud provider.

#2 API integration

- Examples: RESTful APIs, GraphQL.

- How it works: APIs allow your neobank to connect and exchange data with other financial institutions, payment processors, or third-party services seamlessly.

- Parameters for selection: Look for APIs that offer robust security features, developer-friendly documentation, and compatibility with your chosen programming languages.

#3 Blockchain and Distributed Ledger Technology (DLT)

- Examples: Ethereum, Hyperledger Fabric, Ripple.

- How It works: Blockchain and DLT can enhance security and transparency in transactions, making them suitable for cross-border payments and asset tokenization.

- Parameters for selection: Consider factors like consensus mechanisms, innovative contract capabilities, and regulatory compliance when choosing a blockchain platform.

#4 Data encryption

- Examples: Advanced Encryption Standard (AES) and Transport Layer Security (TLS).

- How It works: Data encryption ensures that sensitive customer information remains confidential during storage and transmission.

- Parameters for selection: Look for encryption protocols that are widely recognized, regularly updated, and compliant with industry standards.

#5 Artificial Intelligence (AI) and Machine Learning (ML)

- Examples: TensorFlow, PyTorch, scikit-learn.

- How it works: AI and ML can help detect fraud, automate customer support, and provide personalized financial insights.

- Parameters for selection: Evaluate the capabilities of AI/ML libraries, the availability of pre-trained models, and their suitability for your specific use cases.

#6 DevOps tools

- Examples: Jenkins, Docker, Kubernetes.

- How It works: DevOps tools facilitate continuous integration and continuous delivery (CI/CD), enabling faster and more reliable software development and deployment.

- Parameters for selection: Consider factors like ease of use, scalability, and compatibility with your chosen cloud infrastructure.

#7 Biometric authentication

- Examples: Facial recognition and fingerprint scanning.

- How it works: Biometric authentication enhances security by verifying a user’s identity based on unique physical characteristics.

- Parameters for selection: Evaluate the accuracy, speed, and user-friendliness of biometric authentication methods.

When choosing these technologies for neobank app development, align them with your specific business goals, regulatory requirements, and user expectations.

Step 8. Architect Your System for Scalability and Security

Neglecting proper architectural planning can be a costly mistake, especially considering that the neobank app development cost is not known as being the most budget-friendly option. Try to architect your system for scalability, robustness, and security. Consider the example of Monzo, which faced challenges as it scaled.

Monzo’s scaling challenges:

- Performance bottlenecks: Monzo experienced performance bottlenecks as its customer base multiplied. These bottlenecks could lead to slow transaction processing, delayed account updates, and frustrated users.

- Infrastructure limitations: The initial architecture of Monzo’s systems may not have been designed to handle the scale of users, transactions, and data they eventually encountered. This led to issues with system stability and reliability.

- Security concerns: With more users, enhanced security measures are paramount. Monzo had to continuously bolster its security protocols to protect customer data and transactions from increasing threats.

- Integration challenges: As Monzo expanded its offerings and partnered with various financial service providers, integrating new features seamlessly into its existing system became a complex task. This could result in service disruptions and user dissatisfaction.

- Regulatory compliance: Monzo had to navigate complex regulatory requirements as a financial institution. Ensuring compliance across various jurisdictions while scaling posed a significant challenge.

Step 9. Consider a Banking-as-a-Service Platform

If building from scratch feels overwhelming, explore banking-as-a-service platforms like our FinTech Core. This modular solution offers licensing for its components, allowing custom development while saving time and resources.

Here are the key benefits of FinTech Core which speed up neobank app development:

- Modular approach. FinTech Core is designed as a modular solution. It offers a range of components that can be tailored to your specific needs. This is akin to having a toolkit with various specialized tools that you can pick and choose from to build your neobank. You don’t have to reinvent the wheel for every aspect of your banking services.

- Licensing flexibility. With FinTech Core, you can license individual components, allowing you to customize your neobank while saving significant time and resources. It’s similar to having access to high-quality building materials and hiring skilled builders to construct your dream home without starting entirely from scratch.

- Speed to market. With FinTech Core’s pre-built components, you can significantly reduce your time to market. You will have a trusted partner who knows your destination’s fastest and most efficient routes.

- Expertise and guidance. Neobank app development involves complex regulatory, compliance, and security considerations. With FinTech Core, you benefit from the accumulated knowledge and experience of the team behind the platform. We can navigate these challenges before and guide you effectively.

- Cost-efficiency. Developing every aspect of a neobank can be costly. By leveraging FinTech Core, you can potentially cut development costs significantly, making it more financially viable to realize your neobank vision.

Neobank Tech Stack: Architecture for Regulated Scale

A neobank tech stack is not just core banking + mobile app + APIs.

In regulated fintech, architecture is layered. Each layer supports compliance, scale, and partner orchestration. If one layer is weak, the entire system becomes fragile under audit or growth pressure.

Below is a practical stack map used in real production environments.

1. Customer Layer

This is the experience surface.

- iOS/Android apps

- Web interface (if required)

- Authentication (biometrics, 2FA)

- In-app support

This layer handles UX. It should remain thin. Financial logic must not live here.

2. Orchestration Layer

This is the control layer that connects everything.

- API gateway

- Business logic engine

- Workflow management

- Vendor integrations

- Limits enforcement

The orchestration layer connects sponsor banks, card networks, KYC providers, and payment processors into a coherent system.

Without strong orchestration, vendor dependency becomes structural and difficult to unwind.

3. Core & Ledger Layer

This is the financial backbone.

- Double-entry ledger

- Account structure

- Balance calculation

- Fee and interest logic

- Multi-currency support

The ledger determines reconciliation accuracy, reporting integrity, and regulator confidence. It is not a feature—it is infrastructure.

4. Compliance Layer

Compliance is not a plug-in. It is an architectural constraint. A production-ready system must support:

- KYC / KYB

- AML screening

- Transaction monitoring

- Audit trails

- Data lineage

- Regulatory reporting

- Sponsor-bank audit readiness

During the build of Dozens, compliance workflows shaped core architectural decisions. Ledger design, reporting exports, and orchestration logic were defined around FCA scrutiny requirements.

This experience later influenced Fintech Core’s design—embedding compliance primitives at the foundation rather than layering them on top.

5. Payments Layer

This layer connects the bank to financial rails.

- Sponsor-bank integrations

- Card schemes

- SEPA / Faster Payments / ACH

- Open Banking APIs

Settlement, reconciliation, and payment reliability sit here. This layer directly impacts operational risk.

6. Observability & Operations Layer

Regulators expect operational resilience.

This layer includes:

- Monitoring and alerting

- Incident management

- Reconciliation dashboards

- SLA tracking

- Reporting and analytics

Without strong observability, scale introduces instability.

Where Fintech Core Fits

Fintech Core covers the orchestration, ledger, onboarding, payments, and compliance layers as modular components.

This allows teams to plug in sponsor banks and third-party vendors without rebuilding the core system for every market or licensing shift.

Instead of stitching providers together repeatedly, teams operate on a structured foundation.

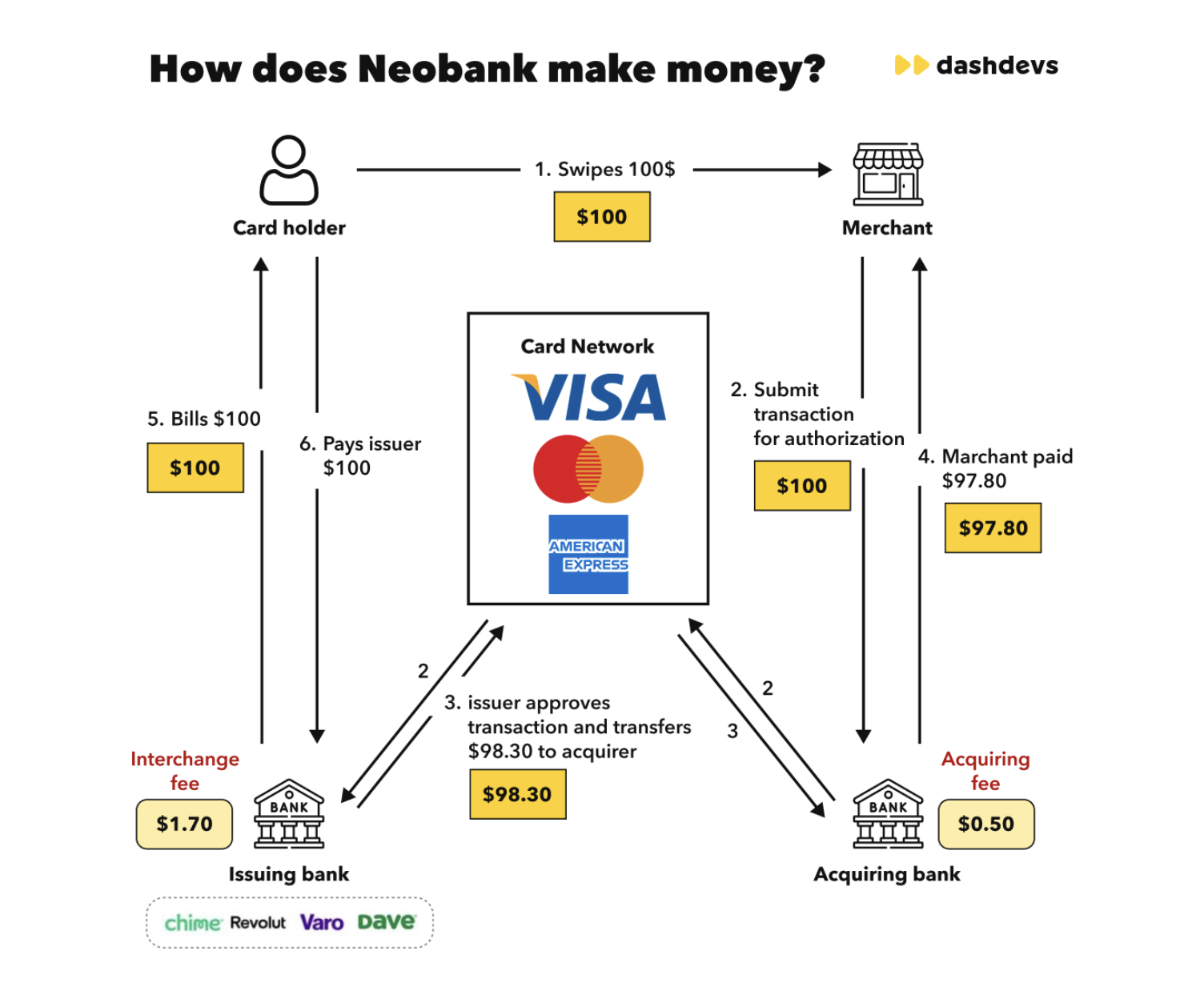

How Do Neobanks Make Money?

There are many business models in fintech, and we’ve already described some of the most popular nowadays. Among them, there are a few specifically spread from which neobanks make money.

#1 Interchange fee. A significant portion of a neobank’s revenue comes from the interchange fees paid by merchants when users use their debit cards to make purchases. Every time a Visa or Mastercard debit card is used to make a purchase, Visa adds a percentage fee to the total. In return, Visa sends a portion of the fees to a neobank.

#2 Loans and overdrafts. In exchange for a fee on each purchase, they facilitate the use of credit cards. When customers go above their restrictions, they pay interest, which generates revenue for the company.

#3 Additional accounts. Digital banking solutions make money from the interest that tacks on to new account balances is another source of revenue.

#4 Withdrawal fee. Neobanks usually accrue interest on the ATM fees, which is another source of revenue.

#5 VIP client services: Offering premium services for a specific fee is common among neobanks, catering to high-value clients.

How Much Does It Cost to Build a Neobank App?

Building a neobank app is no small feat; it requires careful planning, development, and substantial investment. Here’s a breakdown of the potential costs and considerations involved:

1.Cost of Custom Development

Starting a neobank app from scratch can be a pricey venture. To give you a perspective, consider our experience of building the Pi-1 BaaS solution, which was developed at an estimated cost of $4 million.

It’s clear from this figure that you won’t be creating such an app for a mere $100,000. The scope and features you desire play a pivotal role in determining the cost, and you should know them if you’re looking to how to start a neobank.

It’s also crucial to understand that development costs fluctuate depending on the region. For example, North American developers might charge between $150 - $250 per hour. Contrast this with Ukrainian developers who may charge as low as $60 - $90 per hour. Given that the development phase can span 9 months to 2 years, these regional rate disparities can have a significant impact on the total expenditure.

2. Cost of Using White Label Modular Solution

White-label modular fintech solutions are an increasingly popular choice for those wanting to fast-track their entry into the digital banking and payment sector. One of the best choices is Fintech Core, which our clients easily adapt to their needs all around the world.

How to start a neobank easily? With Fintech Core, all the necessary service providers and integrations come pre-configured. This means you’re not starting from ground zero; instead, you’re building on a solid foundation, which significantly reduces time and cost.

Furthermore, the inherent modularity allows for easy customization and scalability. As your neobank grows and the financial landscape evolves, you can add or remove modules as needed, ensuring your platform remains contemporary and competitive.

Cost justification: In terms of timeline and cost, while a custom development might take anywhere from 9 months to 2 years to fully develop and launch, a white-label solution can dramatically cut this down. You could potentially launch your neobank in as little as 3 months, starting from an investment of around $30,000.

It’s crucial to remember that these figures are approximate. Actual costs can diverge based on individual project details, vendor negotiations, and market dynamics. Direct consultation with development professionals is always recommended for precise estimations.

Conclusion

Building a neobank is not just about shipping a mobile app. It’s about making the right structural decisions around licensing, compliance, vendor orchestration, and long-term control.

The opportunity in digital banking is real. Customers expect speed, transparency, and mobile-first experiences. Regulators expect resilience, auditability, and operational maturity. The teams that succeed are the ones that align from day one.

In regulated fintech, architecture is strategy. The choices you make early—sponsor bank vs. license, white-label vs. orchestration, modular vs. monolithic—will define how easily you scale, expand, and adapt.

If you’re planning to launch a neobank, let’s design it the right way. Contact us

Share article