How to Start a Neobank: Licensing, Vendors, and Technology in 2026

June 2, 2026

Summary

Key Points in 60 Seconds

- Building a neobank is an architecture and licensing decision—not a mobile app sprint.

- Most neobanks launch via sponsor bank or EMI paths before pursuing a full banking license.

- White-label speed, API orchestration, and custom core each fit different growth stages.

- Compliance, ledger design, and vendor orchestration define delivery speed more than UI.

- DashDevs Fintech Core and neobank delivery experience support regulated launches from MVP to scale.

Building a neobank today is not about launching quickly with a plug-and-play platform. It is about designing sponsor-bank partnerships or licensed paths, modular infrastructure, and operational control—without creating long-term dependency on rigid vendor stacks.

The global neobank market exceeded $140 billion in 2024 and continues to grow as customers expect mobile-first banking apps without physical branches. Founders researching how to build a neobank or how to start a neobank are usually comparing three paths: white-label speed, API orchestration, or custom core ownership.

Quote-worthy reality: A neobank is not a sleek app on someone else’s core. Regulators expect resilience, payment schemes require technical rigor, and neobank compliance workflows must scale with volume.

DashDevs helped launch one of the UK’s early challenger banks—Dozens—orchestrating sponsor-bank integrations, compliance, card issuing, and core infrastructure. That delivery experience shaped Fintech Core, our white label fintech solution for modular neobank launches.

For production architecture support, see our neobank app development company services.

Summary: What Founders Should Decide First

- Licensing path defines product limits more than UX—sponsor bank, EMI, or full banking license.

- Architecture model (white-label, API orchestration, custom core) determines vendor lock-in risk.

- Neobank regulatory requirements must be embedded in onboarding and payments—not added later.

- Ledger and reconciliation drive feature velocity; weak cores break at scale.

- Do neobanks have a banking license? Often no directly—they operate via partner banks or EMI structures.

This guide covers definitions, vendor models, launch steps, tech stack, costs, and monetization—without repeating the same licensing lecture in every section.

How to build a neobank in 2026 starts with three decisions: license path, architecture model, and first vendor contracts. Everything else—UX, marketing, feature roadmap—depends on those foundations.

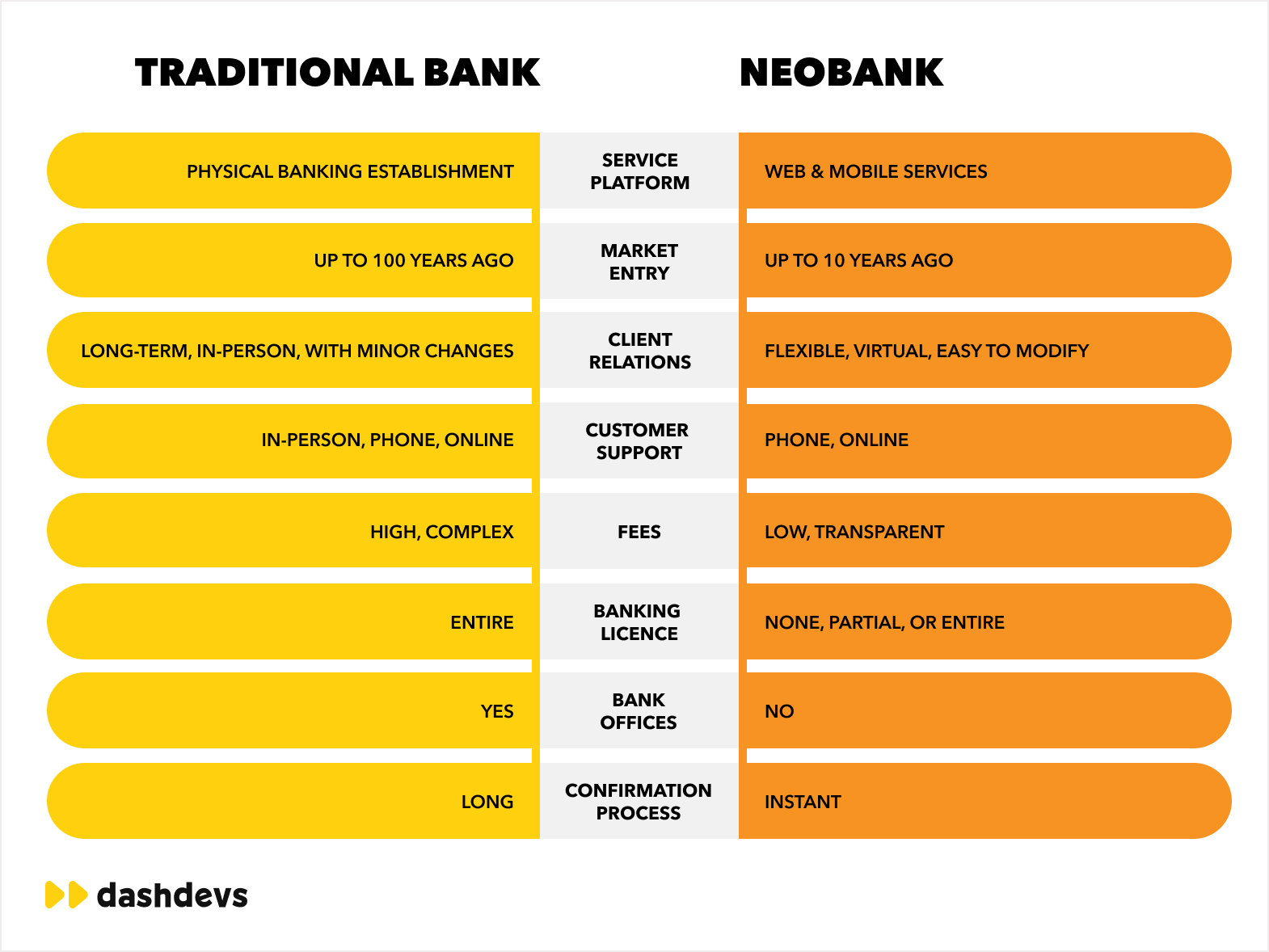

What Is a Neobank (vs. Digital Bank, Challenger Bank, Fintech App)?

The terms neobank, digital bank, and challenger bank are often used interchangeably. Structurally and legally, they differ.

The core distinction: who holds the banking license—and who carries regulatory responsibility?

| Model | Holds Banking License | Can Hold Insured Deposits | Can Lend from Own Balance Sheet | Speed to Launch | Regulatory Burden |

|---|---|---|---|---|---|

| Neobank (sponsor bank) | No | Via partner bank | Via partner bank | Fast | Medium (shared) |

| Neobank (EMI) | No (EMI only) | No (safeguarded funds) | No | Fast–Medium | Medium |

| Fully licensed digital bank | Yes | Yes | Yes | Slower | High |

| Fintech app | No | No | No | Very fast | Low |

Neobank (EMI or Sponsor-Bank Model)

A neobank is a branchless, mobile-first financial product that typically operates without a full banking license—often via an EMI license or sponsor bank/BaaS partnership. Regulated partner banks ultimately hold customer bank accounts in many models.

Users can typically: open accounts, send payments, get debit cards, use budgeting tools, and access partner-funded lending.

Users cannot (independently): hold deposits under the neobank’s own license or lend from its balance sheet.

Examples: Chime (sponsor-bank model), Revolut (hybrid across markets).

Fully Licensed Digital Bank

A digital bank holds a full license, can hold insured deposits, lend directly, and operate under deposit guarantee schemes. Examples: Monzo, Starling Bank, N26. Higher capital requirements, deeper regulatory requirements, but full operational control.

Challenger Bank

“Challenger bank” is a market term—not a legal category. It describes banks competing with incumbents through modern UX, pricing, or infrastructure.

When building your own neobank, licensing determines architecture. Compare paths:

| Licensing Path | Best For | Trade-Off |

|---|---|---|

| Sponsor-bank model | Fast MVP, capital-efficient launch | Vendor dependency |

| EMI → banking license later | Phased growth | Regulatory transition complexity |

| Full license from day one | Long-term infrastructure play | Time and capital intensity |

| Multi-market phased licensing | Cross-border scale | Operational complexity |

Many teams start sponsor-bank-first through BaaS partners, then evolve licensing as product-market fit proves out.

Sponsor Bank vs EMI vs Full License: Operational Differences

| Path | Who holds customer funds | Typical products | Regulator focus |

|---|---|---|---|

| Sponsor bank | Licensed partner bank | Accounts, cards, ACH | Partner oversight + your ops |

| EMI | You (safeguarded e-money) | Wallets, payments | AML, safeguarding, reporting |

| Full banking license | You (deposit-taking) | Deposits, lending, cards | Capital, liquidity, full prudential |

Do neobanks have a banking license? Often not directly at launch. Many operate under EMI or BaaS until scale justifies a full banking licenses application—a multi-year capital and governance commitment.

For a broader digital bank playbook, see how to build a digital bank.

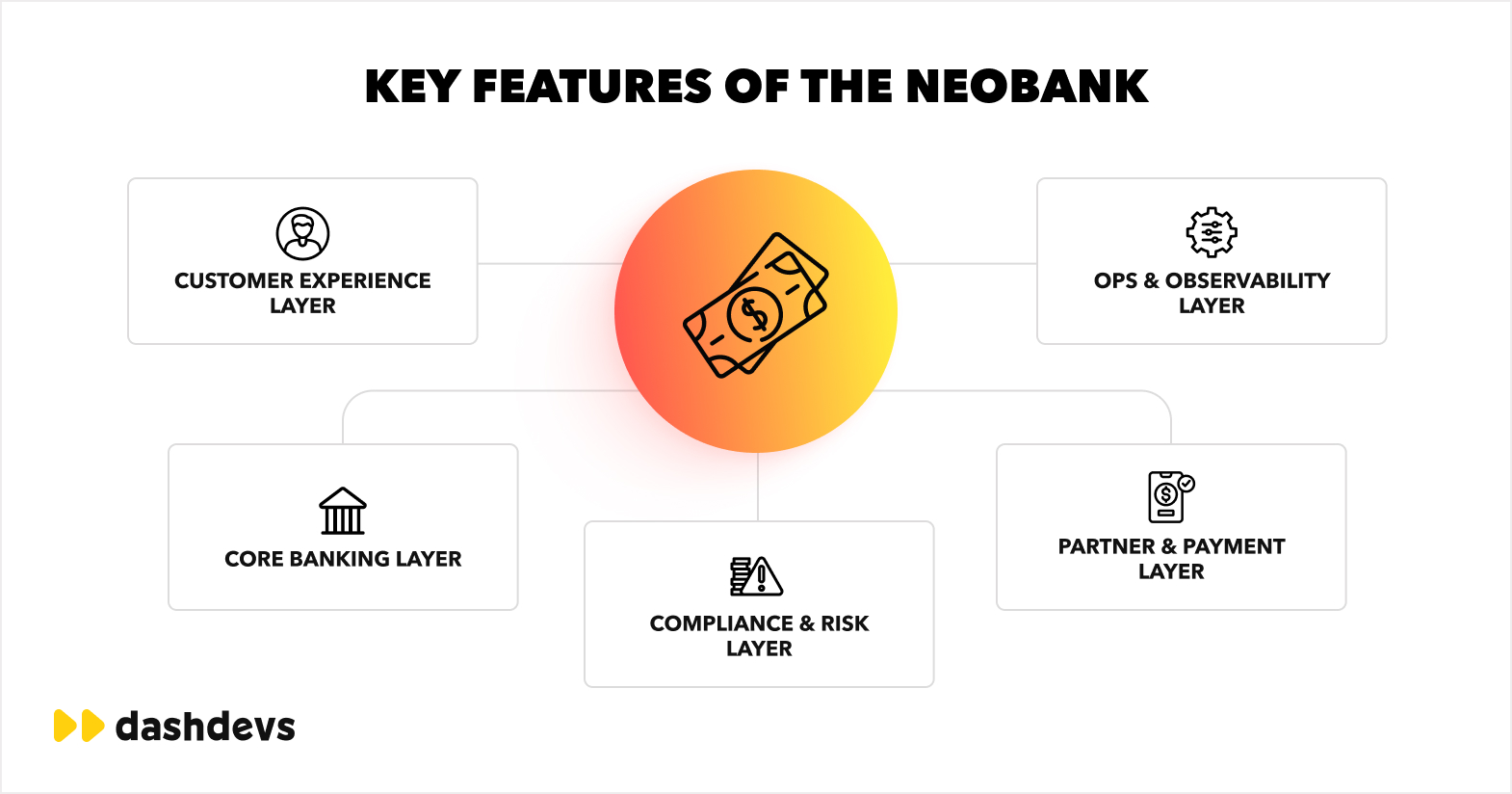

Neobank Features: Delivery Layers, Not a Flat Checklist

Neobank features do not live in isolation. They connect to ledger logic, neobank compliance workflows, and sponsor-bank integrations. In production, feature velocity is defined by architecture—not UI speed.

Group capabilities into five delivery layers:

1. Customer Experience Layer

Digital onboarding, account management, card controls, P2P payments, transaction history, push alerts, and in-app support. Differentiators—cashback, savings goals, referrals—depend entirely on backend layers.

2. Core Banking Layer

Double-entry ledger, balance logic, fees, limits, multi-currency support. Without a proper ledger, reconciliation breaks and audit risk rises. See how a multi-account ledger system supports fintech scale.

3. Compliance and Risk Layer

KYC/KYB, AML monitoring, transaction screening, fraud detection, audit trails, regulatory reporting. Onboarding and payments are compliance-gated in regulated markets.

4. Partner and Payments Layer

Sponsor bank integrations, card schemes, payment gateway integration services, neobank API connections, and BaaS platforms. Poor orchestration here creates settlement and expansion bottlenecks.

5. Operations and Observability Layer

Monitoring, vendor uptime tracking, incident management, reconciliation dashboards. Often skipped at MVP—critical before volume spikes.

During the Dozens build, everyday features were tightly coupled to ledger architecture and sponsor-bank APIs. That production lesson shaped Fintech Core’s modular layer design—onboarding, payments, compliance, and ledger as composable modules rather than flat checklists.

Traditional Bank App vs Neobank: Build Implications

| Factor | Incumbent digital channel | Neobank from scratch |

|---|---|---|

| Core dependency | Legacy core change requests | API-first or modular core |

| Compliance | Established programs | Must design flows early |

| UX ownership | Often constrained by core | Full product control |

| Launch speed | Slower (core politics) | Faster with BaaS/orchestration |

| Long-term flexibility | Migration-heavy | Depends on vendor choices |

Quote-worthy rule: Neobank UX is the visible layer. Settlement, safeguarding, and audit trails are the product.

How to Build a Neobank: Vendors vs. Platforms vs. APIs

When founders ask whether to use a white-label platform or build their own system, the better question is: how much control do we need in 2–3 years—and how much complexity can we operate today?

Three approaches dominate neobank app development solutions. Each works under different conditions.

| Approach | Best for | Speed | Control | Risk |

|---|---|---|---|---|

| White-label platform | MVP, fundraising, market validation | Highest | Lowest | Vendor lock-in |

| API-first orchestration | Growth-stage neobanks, multi-vendor setups | Medium | High | Integration debt |

| Custom core | Licensed banks, balance-sheet control | Lowest | Highest | Capital + regulatory load |

White-Label and White Label Neo Bank Development

White-label stacks package onboarding, payments, cards, and compliance into one integration. White label neo bank development makes sense when you need speed to validate demand—but the vendor owns roadmap gravity.

When it works: Fundraising MVPs, single-market pilots, teams without deep integration engineering yet.

When it breaks: Multi-market expansion, sponsor-bank switches, custom lending logic, or moving from BaaS to own license—each can require partial re-architecture.

Implementation reality: Contracts must define data portability, webhook SLAs, and who owns reconciliation when the vendor changes fee schedules.

API-First Orchestration

Integrate sponsor-bank rails, KYC integration providers, card schemes, and payment processors directly while owning the orchestration layer.

When it works: Growth-stage products with engineering capacity and a clear vendor map per corridor.

When it breaks: Teams underestimate reconciliation, idempotency keys, and multi-vendor incident response—integration debt compounds silently until volume spikes.

Implementation reality: Budget for observability from month one: transaction tracing, vendor health dashboards, and automated reconciliation alerts.

Custom Core

Building ledger + compliance + orchestration suits teams holding or pursuing a full banking license and long-term infrastructure ownership. Not a speed play—a sovereignty play. Evaluate top core banking solutions before committing to a core vendor.

When it works: Licensed digital banks, balance-sheet lending, institutions with multi-year transformation budgets.

When it breaks: Pre-PMF startups that over-build before validating a wedge product—rigid systems become expensive to unwind.

Implementation reality: Regulators will scrutinize ledger design, capital reporting, and operational resilience tests before scale—not after.

What We Learned in Production

On the Dozens build, we avoided a rigid white-label stack and implemented API-first orchestration around sponsor-bank rails with a custom ledger and dedicated compliance workflows. That structure reduced vendor lock-in and supported FCA scrutiny during licensing—later informing Fintech Core’s modular orchestration design.

How to Launch Your Own Neobank: 9-Step Roadmap

With 15+ years in fintech delivery—including developing a neobank from scratch in nine months—here is a practical sequence that avoids repeating licensing and architecture topics already covered above.

Step 1. Define Vision and Product Scope

Clarify your USP, target segment, and first monetizable workflow. Create a neobank strategy around one wedge—payments, accounts, or lending—before expanding. Inspiration: Monzo (simplicity), Chime (US mass market), Revolut (multi-product).

Document what success looks like at 6, 12, and 24 months: active accounts, transaction volume, revenue per user, and regulatory milestones. Investors and regulators both respond to clarity—not feature breadth on slide one.

Step 2. Lock Licensing and Regulatory Path

Confirm sponsor bank, EMI, PI, or full banking license before writing vendor contracts. Many US neobanks operate without a direct license via partner banks. For EMI vs PI detail, see our EMI vs payment institution guide.

Neobank regulatory requirements to map early: safeguarding rules, AML program, complaints handling, and audit reporting. Engage legal counsel in target markets before signing BaaS agreements—exit clauses and data ownership matter when relationships change.

Step 3. Assemble a Fintech-Capable Team

Neobank app development needs product, compliance, engineering, and ops—not only mobile designers. Partner with a fintech app development services team that has shipped ledger, KYC, and payment integrations in production.

Look for teams that understand double-entry ledger events, not only React Native screens. A neobank fails in reconciliation and compliance long before it fails in UI polish.

Step 4. Design UX and Go-to-Market

Prioritize user friendly onboarding and clear identity verification flows. Marketing and UX differentiation often matter as much as backend choice—especially in crowded markets.

Reduce steps to first funded transaction. Every extra screen in onboarding drops conversion—and increases support load when users abandon mid-KYC.

Step 5. Embed Compliance and Security by Design

Integrate KYC and AML screening into onboarding—not as a post-launch patch. Security should run behind the scenes: biometrics, step-up auth, and fraud monitoring without friction.

Build audit trails as first-class data: who approved onboarding, which rules fired, what changed in risk scoring. Regulators and sponsor banks will ask—often with short deadlines.

Step 6. Document Business Processes First

Define onboarding, transaction handling, dispute flows, and reconciliation before coding. Process clarity reduces rework when sponsor-bank SLAs and regulator requests arrive.

Run tabletop exercises: failed payment, chargeback spike, sponsor-bank outage, KYC vendor downtime. Ops playbooks written early prevent panic at 2 a.m. production incidents.

Step 7. Select Technology Stack

Align cloud, APIs, encryption, and observability with regulatory and scale requirements. Core choices: cloud hosting (AWS/Azure/GCP), REST/GraphQL neobank API design, encryption standards, and CI/CD tooling.

Prefer boring, proven infrastructure for money movement. Experimentation belongs in UX—not in how balances post to the ledger.

Step 8. Architect for Scale and Audit

Plan ledger idempotency, multi-region failover, and integration boundaries early. Monzo’s scaling journey showed that performance bottlenecks, security hardening, and regulatory compliance compound quickly without upfront architecture discipline.

Separate release trains for compliance rule changes vs. UX experiments. Coupling them slows both and increases regression risk.

Step 9. Evaluate BaaS and Modular Platforms

If custom build timelines exceed fundraising runway, explore top BaaS platforms or Fintech Core’s modular components. Develop a neobank faster when KYC, payments, and ledger modules are pre-connected—but validate you can change partners later.

Run a technical due diligence workshop: simulate swapping one vendor (KYC or PSP) and estimate engineering weeks. If the answer is “unknown,” orchestration is not yet under your control.

Embedded finance teams should also review how embedded finance companies structure distribution without owning a full core.

Neobank Tech Stack: Architecture for Regulated Scale

A neobank tech stack is not core banking + mobile app + APIs. In regulated fintech, architecture is layered—each layer supports compliance, scale, and partner orchestration.

| Layer | Components | Failure mode if weak |

|---|---|---|

| Customer | iOS/Android, web, auth, support | Poor UX—but not systemic |

| Orchestration | API gateway, workflows, vendor integrations | Vendor lock-in, brittle releases |

| Core and ledger | Double-entry ledger, balances, fees | Reconciliation breaks, audit failure |

| Compliance | KYC, AML, monitoring, reporting | Regulatory sanctions |

| Payments | Sponsor bank, cards, rails, open banking | Settlement risk |

| Observability | Monitoring, reconciliation dashboards | Ops collapse at scale |

Customer Layer

Keep financial logic out of the app. This layer handles UX: authentication, support, and mobile banking flows. Biometric login, push notifications for transaction events, and in-app dispute initiation belong here—but balance calculation does not.

Design for accessibility and low-friction identity verification without sacrificing AML requirements. Regulators care about outcomes; users care about seconds to first payment.

Orchestration Layer

Connects sponsor banks, card networks, KYC providers, and payment processors. Without strong orchestration, vendor dependency becomes structural.

This layer owns business rules: spending limits, fee logic, hold states, and workflow routing between vendors. It is where most neobank API integrations converge—sponsor bank webhooks, card processor callbacks, and KYC result events must be idempotent and traceable.

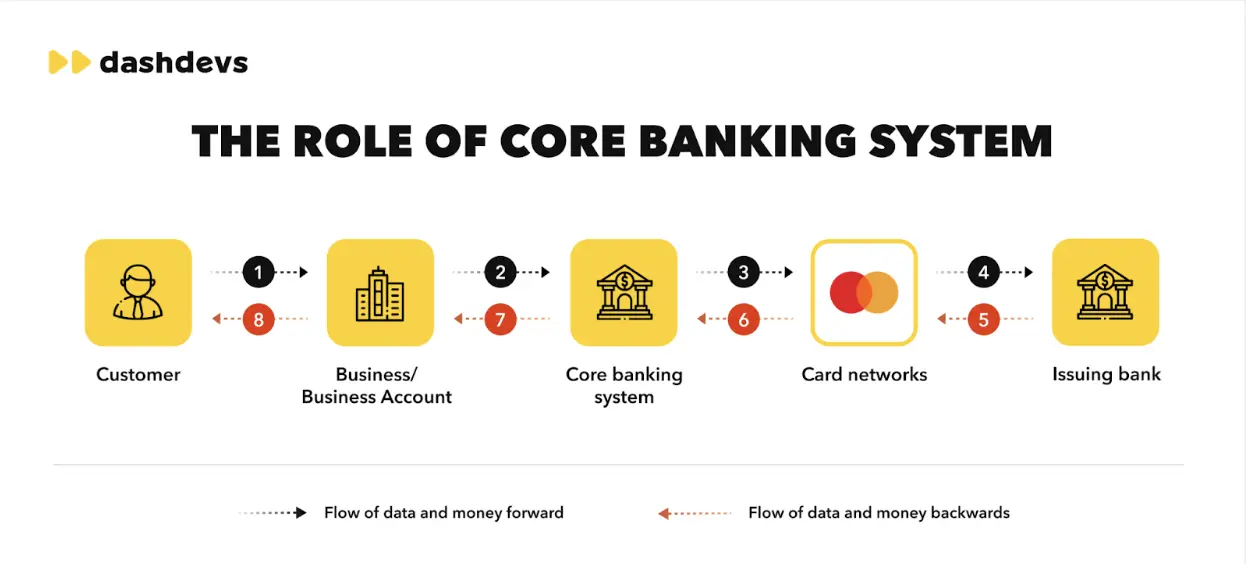

Core and Ledger Layer

The ledger determines reconciliation accuracy and regulator confidence—not a feature, infrastructure.

Every customer-facing balance must map to ledger entries sponsor banks and auditors can reconcile. Multi-currency, pending states, and fee accrual should be modeled explicitly—not inferred from vendor dashboards.

Compliance Layer

Compliance shaped core decisions on the Dozens build: ledger design, reporting exports, and orchestration were defined around FCA scrutiny. Fintech Core embeds these primitives at the foundation.

Neobank compliance is continuous: transaction monitoring, periodic KYC refresh, sanctions screening, and suspicious activity reporting. Batch monthly reviews are insufficient once daily active users exceed low thousands.

Payments Layer

Sponsor-bank integrations, card schemes, SEPA/Faster Payments/ACH, and open banking APIs. Settlement and reconciliation live here.

Payment failures are customer-facing incidents even when root cause is a partner outage. Architecture should support status transparency, retries with limits, and manual ops queues for edge cases.

Observability Layer

Monitoring, incident management, SLA tracking, and reconciliation dashboards. Regulators expect operational resilience.

Define SLOs per vendor: KYC completion rate, payment success rate, card auth latency. Alert on drift before customers flood support.

Fintech Core covers orchestration, ledger, onboarding, payments, and compliance as modular components—so teams plug in sponsor banks without rebuilding the core for every market shift.

Build vs Buy vs Orchestrate: Decision Snapshot

| Stage | Typical approach | Why |

|---|---|---|

| Pre-seed MVP | White-label or BaaS | Speed and capital efficiency |

| Series A scale | API orchestration | Vendor flexibility, own UX moat |

| Licensed bank | Custom core + SI partners | Balance-sheet control |

Teams that skip this sequencing often rebuild at the worst moment—during fundraising diligence or first regulator review.

Who Should Launch a Neobank?

Neobank infrastructure is not only for standalone banking startups. Three profiles commonly adopt it:

Fintech-native companies extending beyond a single product—lending platforms, payment apps, or personal finance tools adding bank accounts and cards. Square’s banking services for merchants show how payment-led distribution can evolve into account-led retention.

Non-financial brands embedding finance to improve conversion and lock-in. Shopify Balance and Uber Money demonstrate how faster payouts and in-app wallets reduce friction—usually via BaaS rather than a full core build.

Licensed banking innovators pursuing challenger positioning with mobile-first UX and lower cost bases than branch networks. Fully licensed paths take longer but remove sponsor-bank dependency over time.

Shared motivations: new revenue streams, better customer experience, faster product iteration, and richer behavioral data. The build-vs-partner decision depends on whether finance is the core business or an enabler inside another product.

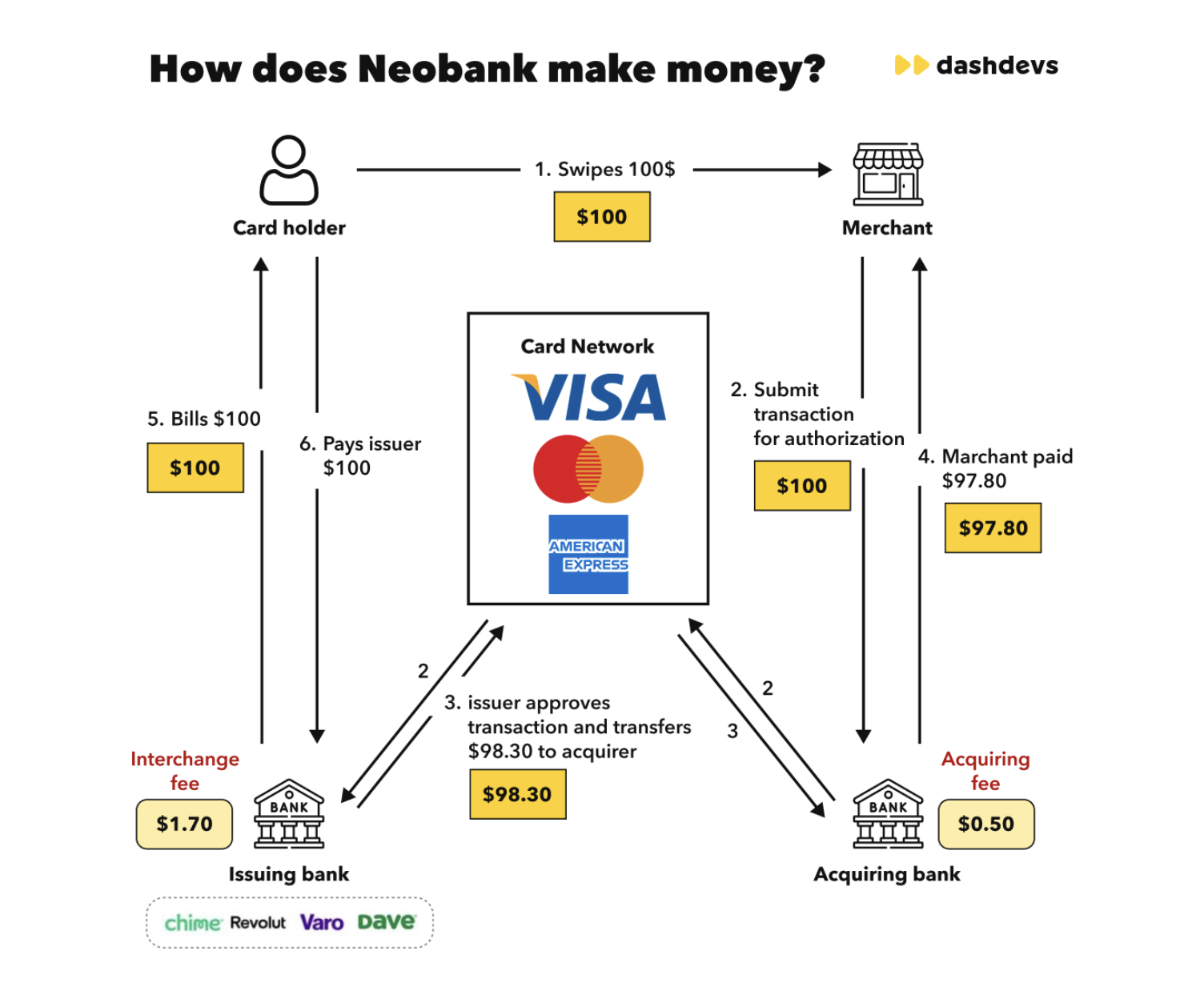

How Do Neobanks Make Money?

Neobanks monetize through multiple streams. We have described proven UK challenger models in detail—here are the most common:

- Interchange fees — revenue when users pay with debit cards

- Loans and overdrafts — interest and fees on credit products

- Account interest spreads — margin on deposits held via partner banks

- ATM and FX fees — charges on withdrawals and currency conversion

- Premium tiers — subscription services for high-value clients

Digital banking solutions that keep users engaged through budgeting tools and transparent transaction history tend to grow interchange and premium conversion faster.

Interchange-heavy models depend on card activation and recurring spend—product teams should instrument card usage from week one, not quarter three.

Common Neobank Launch Mistakes to Avoid

Even strong teams stumble on predictable patterns:

- Choosing vendors before licensing clarity — contracts signed, then discovering the sponsor bank does not support your target product.

- Treating compliance as a launch gate — KYC and AML designed late, forcing onboarding rewrites under regulator pressure.

- No reconciliation ownership — assuming the BaaS vendor reconciles everything until month-end breaks expose balance drift.

- Over-customizing white-label too early — building proprietary logic on closed APIs that cannot migrate.

- Underestimating ops headcount — fraud review, disputes, and vendor incidents require humans long before AI fully automates them.

- Single-vendor dependency — one PSP, one KYC provider, one card issuer with no fallback path documented.

Quote-worthy rule: The cheapest MVP is rarely the cheapest 18-month program if it locks you into the wrong infrastructure.

Neobank App Development: Cost and Timeline

Building a neobank app requires careful planning and substantial investment. Cost drivers: licensing path, vendor model, feature scope, and team geography.

Custom Development Costs

Full custom builds—like the Pi-1 BaaS platform DashDevs delivered—can reach multi-million-dollar budgets over 9–24 months. North American engineering rates often run $150–$250/hour; experienced fintech teams in other regions may charge $60–$90/hour. Scope matters more than hourly rate.

A fully custom neobank with core integrations, compliance tooling, and scalable architecture often exceeds $1M in build cost before operating expenses. Budget separately for licensing applications, legal, card scheme fees, and ongoing AML monitoring.

White-Label and Modular Costs

Launch a neobank faster with modular infrastructure: Fintech Core ships pre-configured integrations for KYC, payments, and ledger modules. MVP launches commonly fall in the $150,000–$400,000 range; modular white-label paths may start near $30,000 depending on scope and markets.

Timeline Benchmarks

| Path | Typical MVP | Regulated scale |

|---|---|---|

| White-label / BaaS | 3–6 months | 9–12 months |

| API orchestration | 6–9 months | 12–18 months |

| Custom licensed bank | 12+ months | 18–36 months |

Quote-worthy range: Speed depends on licensing clarity more than engineering velocity. A team with senior developers but no sponsor-bank agreement will still stall.

Ongoing costs—cloud, compliance staff, vendor fees, customer support—often exceed initial build spend within 18 months. Model unit economics before launch, not after.

Conclusion

How to start a neobank successfully means aligning licensing, compliance, vendor orchestration, and long-term control from day one—not shipping a banking app in isolation.

Customers expect speed and mobile-first digital banking solutions. Regulators expect resilience, auditability, and operational maturity. Teams that win make structural choices early: sponsor bank vs. license, white-label vs. orchestration, modular vs. monolithic.

Architecture is strategy in regulated fintech. The neobank from scratch path and the BaaS path can both succeed—but only when licensing, ledger design, and vendor contracts align with a 24-month roadmap, not a demo deadline.

If you are planning to launch a neobank, design architecture before aesthetics. DashDevs brings 15+ years of regulated fintech delivery—from challenger bank launches to modular Fintech Core deployments.

Share article