Mobile Banking App Development Guide (2026)

A practical guide to mobile banking app features, architecture, security, costs, and launch strategy for banks and fintech teams in 2026.

March 17, 2026

Summary

Mobile Banking App Development in 60 Seconds

- Mobile banking apps are now the primary banking interface, not a secondary channel.

- Successful apps depend on backend infrastructure, payments, compliance, and security, not just UX.

- Development costs vary significantly based on integrations, compliance requirements, and product complexity.

- A hybrid approach combining custom engineering with vendor infrastructure often provides the best balance of speed and flexibility.

Mobile banking has quietly become the primary product layer for financial institutions.

For most customers, the banking relationship no longer starts in a branch or on a website. It starts with an app icon. But building a mobile banking app today is no longer a simple UI project. It is an infrastructure decision involving onboarding, payments, compliance systems, card integrations, security architecture, and scalable backend services.

Banks, fintech startups, and payment institutions that treat mobile banking as “just another mobile app” often discover too late that the real complexity lies behind the screens.

This guide explains how mobile banking app development works in 2026, including the architecture, features, security requirements, costs, and strategic decisions that shape successful digital banking products.

Why mobile banking app development matters now

For most customers today, the mobile app is the bank. They open accounts, transfer money, manage cards, monitor spending, and contact support entirely through mobile devices. Branch visits and even desktop banking are becoming secondary touchpoints.

According to Statista, more than 70% of banking customers globally use mobile apps as their primary banking interface, and adoption continues to grow across both developed and emerging markets.

This shift changes how financial products must be designed. Mobile apps are no longer just digital access points. They are the core user experience layer connecting customers to banking infrastructure.

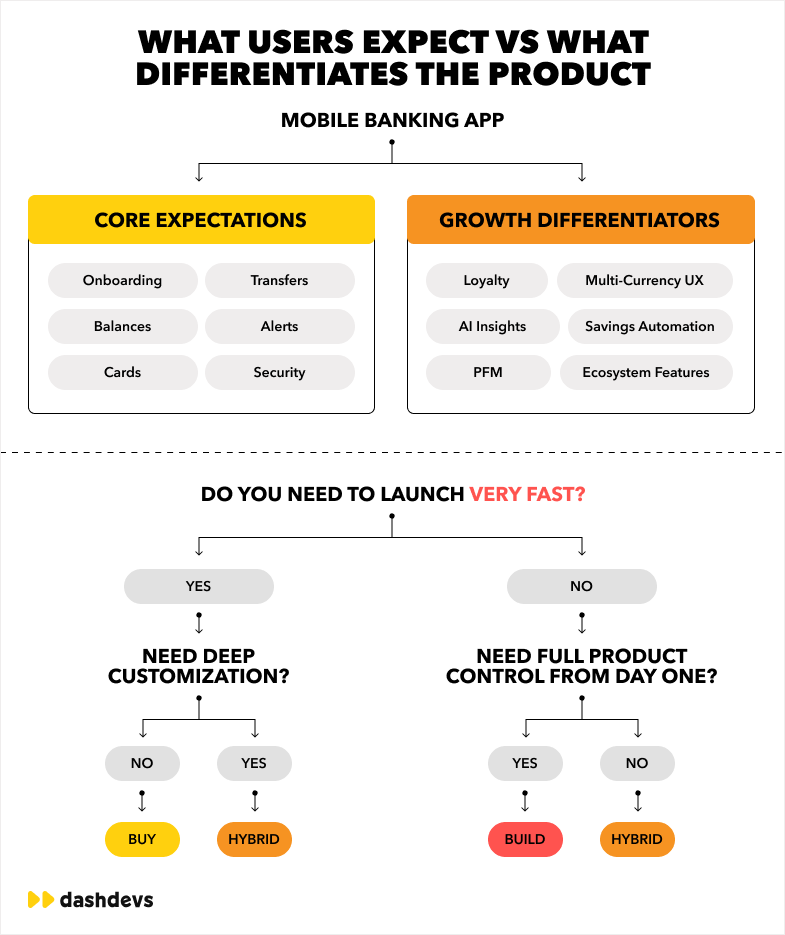

User expectations go beyond basic account access

Early banking apps simply allowed users to check balances and review transactions. Today users expect far more:

- instant account onboarding

- real-time payments and transfers

- card controls and security alerts

- spending analytics and budgeting tools

- integrated customer support

- seamless authentication across devices

The bar has been raised by neobanks like Revolut, Monzo, and Nubank, which treat mobile apps as complete financial operating systems.

Why banks, fintechs, and EMIs continue investing in mobile

Several industry forces are accelerating mobile banking development:

| Driver | Why it matters |

|---|---|

| Customer expectations | Users expect real-time, mobile-first financial services |

| Cost efficiency | Digital channels reduce operational costs compared to branch banking |

| Fintech competition | Neobanks and embedded finance platforms raise UX standards |

| Regulatory innovation | Open banking and digital identity systems enable new products |

| Global digital adoption | Mobile-first markets are expanding financial inclusion |

For both traditional banks and fintech companies, the mobile app is increasingly the main competitive advantage.

What is mobile banking app development?

Mobile banking app development is the process of designing, building, integrating, and maintaining a secure mobile application that allows customers to access banking services through smartphones or tablets.

These services typically include:

- account management

- payments and transfers

- card operations

- onboarding and identity verification

- transaction monitoring

- financial insights and alerts

Unlike typical consumer apps, banking apps must integrate with multiple financial systems simultaneously.

Mobile banking app vs digital wallet vs fintech app

These terms are often confused but represent different product models:

| Product type | Key function | Example |

|---|---|---|

| Mobile banking app | Full banking experience with accounts, cards, payments | Monzo |

| Digital wallet | Payment-focused product storing cards or balances | Apple Pay |

| Fintech app | Specialized financial product (lending, investing, insurance) | Robinhood |

A mobile banking app typically combines multiple fintech capabilities into one platform. For a deeper look at fintech app development models, see our guide to fintech mobile app development.

Who needs mobile banking app development?

Mobile banking products are being built by several types of organizations.

Traditional banks modernizing digital channels

Legacy banks are upgrading outdated mobile apps to compete with modern fintech platforms. Key priorities usually include:

- improving onboarding UX

- enabling instant payments

- integrating open banking APIs

- modernizing backend infrastructure

Neobanks and challenger banking startups

Digital-first banks rely almost entirely on mobile apps as their customer interface. These companies typically focus on:

- rapid onboarding

- card-first experiences

- automated savings tools

- subscription-based services Learn more about this model in our guide on how to start a neobank.

EMIs and payment institutions expanding into banking

Many payment institutions now offer features traditionally associated with banks:

- accounts with IBANs

- debit cards

- cross-border payments

- personal finance tools

These services require mobile banking infrastructure even without a full banking license.

Fintech platforms adding accounts and cards

SaaS platforms and marketplaces increasingly embed financial services directly into their apps. Examples include:

- expense management tools

- B2B payment platforms

- investment platforms

- digital marketplaces

Must-have banking app features (MVP scope)

A typical MVP banking app includes the following core capabilities. However, for business owners, it’s important to understand that these are not just “features”—they are revenue enablers, cost drivers, and compliance touchpoints.

| Feature | What it does | Business impact | Key considerations |

|---|---|---|---|

| Registration & authentication | User account creation and login | First conversion point (onboarding funnel) | Drop-off rates often exceed 40–60% without optimization |

| Digital KYC onboarding | Identity verification (ID, selfie, AML checks) | Enables regulatory compliance and account activation | KYC automation can reduce onboarding time from days to under 5 minutes |

| Account opening | Creates user account and ledger entry | Core product activation moment | Requires integration with core banking or ledger system |

| Balance & transaction history | Real-time account visibility | Drives daily engagement and retention | Needs accurate, real-time data synchronization |

| Internal & external transfers | Money movement between accounts and banks | Core monetization driver (fees, interchange) | Requires payment rails (SEPA, Faster Payments, etc.) |

| Bill payments | Utility and recurring payments | Increases stickiness and daily usage | Often requires third-party integrations |

| Debit/virtual card management | Card issuance, controls, freezing | Generates interchange revenue | Integration with card processors (Visa, Mastercard) |

| Transaction alerts | Real-time notifications | Reduces fraud and increases trust | Requires event-driven architecture |

| Biometric login | Fingerprint / Face ID authentication | Improves UX and security | Standard expectation across modern apps |

| Customer support chat | In-app assistance | Reduces churn and support costs | Needs integration with CRM/support tools |

| Document center | Stores statements, agreements | Regulatory requirement | Must support audit and compliance |

From a business perspective, these features directly influence three critical KPIs:

1) Customer acquisition and conversion

The onboarding flow (registration + KYC + account opening) is where most fintechs lose users:

- industry data shows onboarding drop-offs can reach 60%+ if flows are too complex

- reducing onboarding time to under 5 minutes can increase conversion rates by 20–30%

- automated KYC reduces manual review costs by up to 70%

This means onboarding is not just a feature—it is your primary growth engine.

2) Revenue generation

Core banking features directly tie into monetization:

- card usage generates interchange revenue (0.2–1.5% per transaction depending on region)

- transfers and FX operations enable fee-based income

- increased transaction frequency drives lifetime value (LTV)

Apps that successfully embed payments and cards into daily user behavior typically see:

- 2–3x higher engagement rates

- significantly higher revenue per user compared to “view-only” apps

3) Retention and product stickiness

Features like transaction alerts, spending insights, and bill payments increase daily usage:

- users who enable notifications are 2x more likely to stay active

- apps with personal finance tools see up to 30% higher retention

- in-app support reduces churn by resolving issues instantly

Advanced features that differentiate mobile banking products

Once core functionality is stable, banks and fintech companies begin adding features that improve user retention, engagement, and long-term revenue. Common examples include:

- subscription management and recurring payments

- automated savings goals and smart rules

- multi-currency accounts and FX support

- rewards, cashback, and loyalty programs

- family or shared accounts

- open banking account aggregation

- AI-powered financial insights and recommendations

These features help transform a banking app from a simple utility into a daily financial companion, increasing usage frequency and customer stickiness.

However, successful teams avoid adding too many features too early. Advanced functionality only delivers value when the core infrastructure is stable and scalable.

As discussed in Fintech Garden Episode 108: BaaS in the Wild, Igor Tomych emphasizes:

“The biggest mistake fintech teams make is building too many features before they build reliable infrastructure.”

This is why the most effective mobile banking products focus first on reliability, compliance, and transaction flows — and only then expand into advanced features that drive differentiation.

The architecture behind mobile banking apps

A mobile banking app is only the visible layer of a much larger financial system. The underlying architecture typically includes the following components:

| Layer | Purpose |

|---|---|

| Mobile frontend | iOS and Android applications |

| API gateway | Handles communication between app and backend |

| Backend services | Business logic and orchestration |

| Core banking or ledger | Account balances and transactions |

| Payment integrations | Card processors and payment networks |

| Compliance systems | KYC, AML, and monitoring |

| Admin and support tools | Operations dashboards |

| Monitoring and analytics | Performance and user insights |

This architecture ensures the system can support high transaction volumes and regulatory reporting requirements. For reliability considerations, see our article on high availability and fault tolerance in fintech applications.

Security requirements in mobile banking app development

Security is one of the most critical aspects of mobile banking app development and digital banking app development.

For banks, fintech startups, and EMIs, security is not just a technical requirement — it is a core product feature that directly impacts user trust, retention, and regulatory approval.

Modern users expect banking apps to be secure by default. At the same time, regulators require strict controls to protect financial data, prevent fraud, and ensure system integrity.

In practice, this means that mobile banking application development must include security at every layer of the architecture, not as an afterthought.

Essential security features in banking app development

Below are the key security components every mobile banking software development project must include:

| Security layer | Purpose | Business impact |

|---|---|---|

| Multi-factor authentication (MFA) | Prevent unauthorized access | Reduces account takeover risk and fraud losses |

| Biometric login (Face ID, fingerprint) | Secure and convenient authentication | Improves UX while maintaining high security |

| Data encryption (in transit and at rest) | Protect sensitive financial data | Required for compliance and user trust |

| Device recognition and binding | Detect unknown or risky devices | Prevents unauthorized access attempts |

| Fraud monitoring systems | Identify suspicious transactions in real time | Reduces financial losses and regulatory risk |

| Session management | Prevent hijacked or inactive sessions | Ensures safe user interactions |

| Audit logging | Track all system actions and transactions | Required for compliance and investigations |

Why security drives business outcomes

For business owners, security directly affects:

- Customer trust and retention: users will abandon apps that feel unsafe. Security features like real-time alerts and biometric authentication increase confidence and engagement.

- Fraud prevention and cost reduction: advanced fraud detection systems can reduce fraud losses by 30–50%, depending on implementation maturity.

- Regulatory approval and scalability: without proper security infrastructure, launching in regulated markets (EU, UK, MENA) becomes impossible.

Security as infrastructure, not a feature

A common mistake in fintech mobile app development is treating security as an add-on. In reality:

- authentication must be integrated into every user flow

- transaction monitoring must be real-time and automated

- encryption must cover all data layers

- audit logs must be available for regulators and internal teams

This is why security architecture is tightly connected to banking app architecture and backend systems.

Compliance and regulatory considerations

Alongside security, compliance is a defining factor in mobile banking app development in 2026.

Financial applications must operate within strict regulatory frameworks that vary by region but share common principles: identity verification, transaction monitoring, data protection, and auditability.

Key compliance requirements in digital banking app development

Every mobile banking application development project must address the following:

- KYC (Know Your Customer) and AML (Anti-Money Laundering) verification

- transaction monitoring and suspicious activity detection

- data privacy regulations (GDPR, local equivalents)

- card scheme compliance (Visa, Mastercard requirements)

- audit logging, reporting, and traceability

These are not optional features — they are mandatory for operating in regulated financial environments.

How compliance shapes product design

Compliance is not just a legal layer. It directly affects how your product works.

For example:

Onboarding flows

- must collect identity data

- must include document verification and checks

- must support regulatory reporting

Transaction systems

- must detect suspicious patterns

- must enforce limits and rules

- must trigger alerts and reviews

Support and operations tools

- must store audit trails

- must allow investigation of transactions

- must provide regulator-ready reporting

This is why compliance architecture must be designed alongside product UX, not added later. Explore the case here.

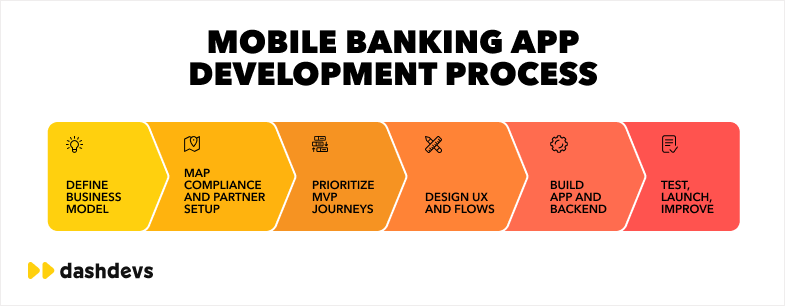

Mobile banking app development process

Launching a mobile banking app is a multi-stage process that combines product strategy, fintech architecture, compliance, and engineering execution.

Below is a simplified view of how mobile banking application development typically unfolds:

| Stage | Key activities |

|---|---|

| Strategy | Define business model, target market, and regulatory setup |

| Product design | Map user journeys, onboarding flows, and UX structure |

| Architecture | Select core banking, payment, KYC, and integration partners |

| Development | Build mobile apps, backend systems, and admin tools |

| Testing | Validate security, performance, and edge cases |

| Launch | Gradual rollout with monitoring and support |

| Growth | Expand features, integrations, and geographic coverage |

What makes banking app development different

Unlike typical mobile apps, mobile banking software development requires tight coordination across multiple teams:

- product teams define user experience and priorities

- compliance specialists ensure regulatory alignment

- engineers build scalable backend and integrations

- designers optimize onboarding and usability

- QA teams validate security and reliability

- operations teams manage support and monitoring

The key difference: you are not just building an app—you are launching a regulated financial product.

Pro tip

The most successful teams invest heavily in:

- onboarding flows (conversion driver)

- backend architecture (scalability)

- admin and support tools (operations efficiency)

These layers often matter more than the number of screens in the app.

How much does mobile banking app development cost?

The cost of mobile banking app development varies significantly depending on product scope, infrastructure, and compliance requirements.

Instead of fixed estimates, it is more useful to evaluate costs based on product maturity stages.

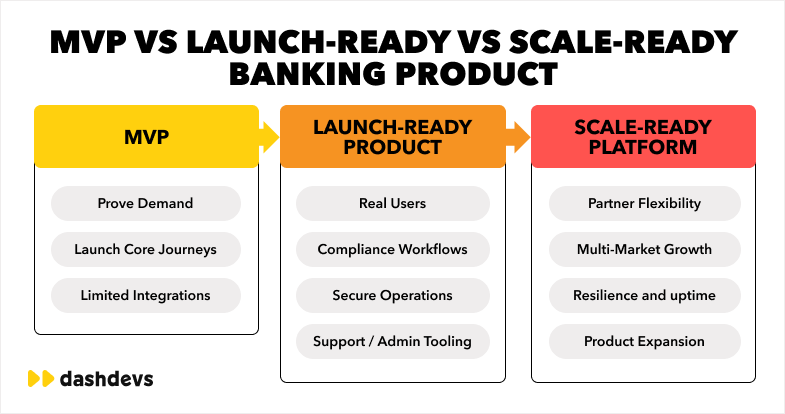

Cost by product stage

| Product stage | Typical scope | Relative complexity |

|---|---|---|

| Prototype | UX concept or clickable demo | Low |

| MVP | Onboarding, accounts, payments | Medium |

| Launch-ready banking app | Full backend, integrations, compliance systems | High |

| Multi-market platform | Localization, orchestration, regulatory expansion | Very high |

Key cost drivers in banking app development

Several factors influence the final cost of a digital banking app development project:

- regulatory requirements (KYC, AML, reporting)

- number and complexity of integrations (payments, cards, open banking)

- backend architecture (ledger, orchestration layer, APIs)

- security infrastructure (fraud detection, monitoring, encryption)

- development team composition and expertise

In most cases, backend complexity and compliance requirements drive costs more than UI development.

Why cost estimates often go wrong

Many teams underestimate costs because they focus on:

- screen design instead of infrastructure

- features instead of integrations

- UI instead of compliance

In reality, building a banking app is closer to building a financial system with a mobile interface, not just a mobile product.

For a detailed breakdown, read our article on fintech app cost.

Real-world DashDevs mobile banking examples

DashDevs has supported multiple mobile banking and digital banking platforms across Europe and MENA, helping teams launch products that combine strong UX with reliable infrastructure.

UK challenger bank

Dozens, a challenger bank in the UK, was built with a custom architecture designed for rapid scaling and long-term flexibility.

This project highlights how mobile banking app development must align with backend infrastructure from day one.

Compliance-first digital banking platform

In Saudi Arabia, DashDevs developed a digital banking platform where compliance was embedded directly into the architecture. The platform included:

- real-time monitoring and alerts

- automated compliance workflows

- audit-ready infrastructure

This approach ensured regulatory readiness and operational reliability at launch.

Open banking platform in MENA

DashDevs contributed to the launch of Tarabut Gateway, one of the first regulated open banking platforms in the MENA region.

This project demonstrates how mobile banking apps increasingly rely on open banking infrastructure to deliver connected financial experiences.

Key takeaway

Across all cases, one pattern is clear: successful mobile banking products are built not just with strong UX, but with scalable architecture, compliance-first design, and flexible integrations.

Conclusion

Mobile banking app development is no longer just a UX initiative. It is a strategic investment that combines product design, financial infrastructure, compliance systems, and scalable architecture.

Banks and fintech companies that treat mobile banking as a core platform rather than a front-end project are far more likely to launch products that scale successfully.

By aligning technology, compliance, and product strategy from the beginning, organizations can build mobile banking platforms that deliver both great user experiences and operational reliability.

Share article