What Is a Multi-Account Ledger System (And Why Fintech Platforms Need It to Scale)

April 26, 2026

Summary

TL;DR for fintech leaders

- A multi-account ledger system is a unified ledger system that records every financial event and keeps user, merchant, settlement, and internal accounts consistent in real time.

- Without it, teams stitch balances from PSPs, cores, and spreadsheets—reconciliation becomes investigation, not validation.

- The fix is architectural: one transaction ledger and payment ledger semantics at the center, with providers feeding in rather than owning truth.

- Modular platforms (for example Fintech Core) combine multi-account ledger design with orchestration so new products plug into the same financial ledger system instead of forking logic.

Most fintech roadmaps talk about features, APIs, and growth. Boards ask for new markets, new products, and higher conversion. Engineering tickets pile up for integrations, retries, and edge cases. Somewhere underneath all of that sits a quieter subject that rarely wins a keynote slide but determines whether the company can survive its own success: whether the platform has a coherent multi-account ledger system at the center, or a patchwork of partial truths about money.

This article explains what that means in practice, why fintech ledger system design is no longer optional at scale, and how a unified financial ledger system turns reconciliation from a permanent fire drill into a controlled process. If you already work with ledgers at a conceptual level, our complete guide to ledgers in banking and fintech layers vocabulary and mechanics; here we focus specifically on multi-account architecture and operating reality. The shift from a single product with one acquirer to a portfolio of products, rails, and entities is when “we will fix reporting later” stops being a schedule slip and becomes a balance-sheet risk. That is the inflection this piece is written for: leaders who need to make the right call before the next funding round, audit, or market expansion forces it.

TL;DR for fintech leaders

If you only read one section, carry a few clear ideas into your next architecture and risk review, not just your backlog grooming.

What the board should hear in one pass

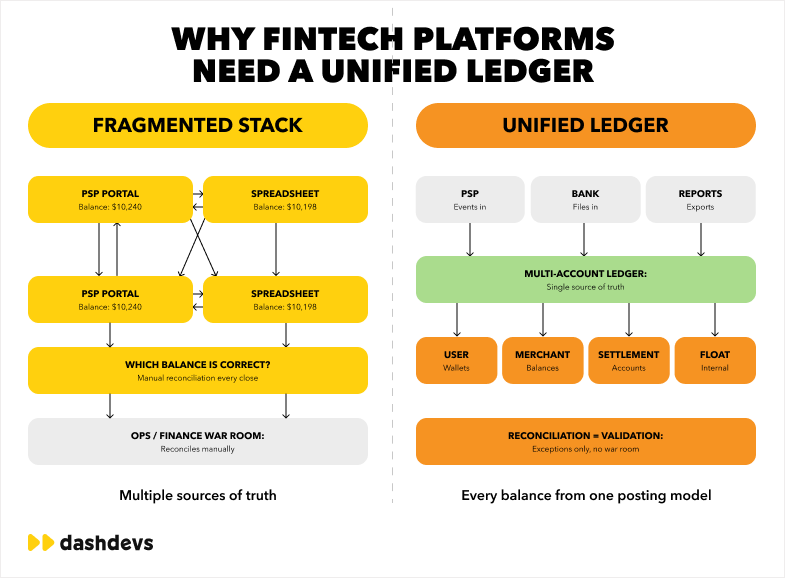

A multi-account ledger system is the platform’s single place where balances and movements are defined. It is not “a database table that stores transactions” in the abstract—it is the contract that says which transaction ledger entries are valid, how payment ledger events post, and how user, merchant, and house accounts relate when money moves, holds, or settles. The leadership question is not whether you have Postgres or a warehouse; it is whether your financial ledger system can tell you, in one place, who owes what to whom now, under your product and regulatory rules, with an audit trail you can show without a two-week data archaeology sprint.

Why fragmented stacks stop scaling when revenue still looks good

Second, fragmentation is expensive in a way quarterly reports understate. Teams respond with spreadsheets, manual controls, and heroic operations work. That can keep the business alive for a while; it does not produce a ledger system you can audit, explain to a regulator, or extend when you add another PSP, another country, or another product line. A typical mid-stage example: a wallet product reads “available” from a cache keyed by a PSP’s authorization file, while finance books settlement from a nightly batch, while risk tracks exposure in a separate model. All three can be locally correct; none of them is a substitute for a platform-owned view of the customer promise.

What “good” looks like: providers as inputs, not owners of reality

Third, the organizations that scale without constant re-platforming tend to invest in this layer early enough that external systems act as inputs, not as owners of financial reality. As Fintech Garden episode 150 frames the broader market shift, fintech is no longer rewarded for speed alone—reliability, operational clarity, and defensible infrastructure are the durable advantages. A unified financial ledger system is part of that story: it is how you prove what happened to money under real traffic. The practical test is a boring one that executives rarely ask for until it is late: can you freeze a day’s activity, replay postings, and explain every cent without opening five consoles?

Top pain points fintech companies face

Before discussing solutions, it helps to name the symptoms product, finance, and engineering all feel—often at the same time, with no single owner. Many teams call this “a tooling problem” or “a reporting project.” In our experience, if the same three symptoms recur every quarter, you are looking at a multi-account ledger system gap, not a dashboard shortage.

| Pain | What it feels like in the organization | Why it gets worse with scale |

|---|---|---|

| No single view of balances | Disputes, “which balance is right?” tickets, slow customer answers | More accounts, more products, more caches |

| Fragmented data | CSV tennis between ops, finance, and engineering | More providers, more time zones, more cut-offs |

| Conflicting reports | Month-end surprises, audit anxiety | More manual joins, more human interpretation |

| Integration sprawl | Every new rail adds its own “mini ledger” | State machines multiply; ownership blurs |

| Provider-led truth | Product roadmaps wait on file formats and exceptions | You optimize vendor timelines instead of your customers |

| Operations load | Headcount grows linearly with volume | Manual work does not scale; it compounds errors |

No real-time visibility into balances (and what “real-time” should mean)

The first is lack of real-time visibility into balances. Customer support sees one number, finance exports another, and a dashboard in the back office shows a third because each channel reads from a different partial ledger system or cached export. That is not merely inconvenient; it erodes trust internally and, eventually, with partners and customers when disputes arrive. Expert teams still distinguish between user-facing immediacy and books-closed cut-offs: you may show a pending state instantly while settlement remains T+1, but both states must be explainable and tied to the same transaction ledger, not to three ad hoc queries.

Financial data is delayed, sliced, and owned by the wrong layer

A second pain is that financial data arrives late or scattered. Payment service providers, banks, and internal services each emit their own files and events. Without a fintech ledger system that normalizes and posts those events into one model, the organization lives in a permanent lag between “what the business believes” and “what the providers eventually confirm.” A concrete pattern we see: engineering builds a streaming integration for webhooks, but finance still depends on a monthly file because no one ever mapped the provider’s “settled” event to a posting the GL recognizes. The technical pipeline works; the financial model does not.

Reconciliation is reactive, manual, and expensive

Third, reconciliation is often reactive, manual, and expensive. In the worst cases it behaves like damage control: teams compare three sources, decide which to trust, and adjust operational accounts after the fact. Fintech Garden episode 112 is a useful touchstone for why automation in payments and financial operations is not about convenience alone—it is about reducing the error surface when volumes rise. A mature team still runs reconciliation, but the work shifts from “we do not know what should have happened” to “we know what should have posted; we are matching rails to ledger.”

Multiple systems, multiple definitions of the same number

A fourth pain is inconsistent reporting: the PSP says “captured,” the card network file says “clearing in progress,” and the internal “success” event fired on authorization. For the product, a payment “worked” at checkout; for settlement, the money is not done moving. A multi-account ledger system does not remove network lifecycles, but it gives you a single place to name each stage, post each transition, and show customers language that matches the contract—instead of a generic “processing” that hides a dozen incompatible states.

Every new integration increases fragility, not just surface area

When you add a new acquirer, a local bank, or a B2B payout rail, the integration project often under-estimates the financial work: new exception codes, new settlement calendars, and new “who owns the idempotency key” questions. If each rail carries its own mini ledger or mapping table, you multiply failure modes. The fix is not fewer integrations; it is a single ledger system that can absorb a new source of events without a parallel shadow accounting stack.

When financial logic lives in providers and spreadsheets

Finally, there is a strategic pain. Financial logic that lives mostly inside providers—acquirer reports, processor portals, and bank statements as your primary “system of record”—limits how flexibly you price, how honestly you show balance states in the product, and how fast you can launch adjacent products. That constraint shows up in digital banking and platform plays alike; how to build a digital bank is as much a ledger and controls story as a licensing one. If your roadmap cannot answer “where does this fee post?” or “which account holds the float during this three-day hold?” without a custom script, the platform does not own the financial product—it rents it.

The uncomfortable pattern: the company does not have “a reconciliation problem” first—it has a transaction ledger ownership problem. Reconciliation is the tax you pay when no unified payment ledger model leads.

The root cause: no unified ledger at the core

In many early-stage builds, a transaction ledger is implicit. You store events in an application database, you mirror a provider’s idempotency keys, and you hope you can recompute a balance if asked. That works until the product surface branches: wallets, treasury accounts, marketplace payouts, interest, fees, reserves, and compliance holds each ask for a slightly different view of the same money.

Financial data is distributed by design, but nobody owns the merge

When financial data is distributed across multiple systems, each one maintains its own version of what balance means and when it changes. A PSP might know authorization state; your core might know the booked balance after settlement; a spreadsheet might track promotional credits. None of those is wrong in isolation. Together, without a multi-account ledger system to integrate them, they guarantee drift. A frequent expert observation in diligence is that the company has accurate components and an inaccurate story: the warehouse total matches nothing in the app because no one system defines “available” as a first-class, posted concept.

There is no single source of truth in that world—only a negotiated truce that lasts until the next exception: a return, a chargeback, a duplicate webhook, a partial settlement, or a holiday cut-off.

Reconciliation that fixes architecture instead of proving correctness

Reconciliation then compensates for architecture instead of confirming it. That is a crucial distinction. In a healthy design, you reconcile to detect problems early. In a fragmented design, teams reconcile to discover which version of reality they must book—often days later. That is also where ad hoc RFPs for “reconciliation automation” suites appear, trying to paper over the absence of a real fintech ledger system. Automation helps; it does not replace a coherent model. Intelligent matching and exception queues, when applied on top of a clear posting model, automate the boring matches; on top of chaos, they automate the wrong conclusions faster.

Why product teams deprioritize the fix (until it is expensive)

Igor has discussed the unbundling of fintech and banking models on Fintech Garden episode 122; a parallel lesson for engineering is that every “mini product” you bolt on top of a weak ledger system replicates complexity at the data layer. You do not feel it in week six. You feel it in year two, when a funding round or a regulator asks for traceability and the organization cannot generate it without a forensic project. The lesson for leadership is to fund ledger design with the same seriousness as a security review: it is not a refactor ticket, it is a risk control for customer money and regulatory credibility.

What is a multi-account ledger system

A practical definition is simple to say and hard to implement: a multi-account ledger system is a centralized financial ledger system that records all relevant transaction ledger activity and maintains balances for every account the business must reason about—customers, merchants, the platform’s own operational accounts, settlement accounts, and often partners or program managers—so that, at any time, the platform can answer “who holds what, under which rules, with what holds and pending states” from one system.

A definition you can use with engineering and compliance in the same room

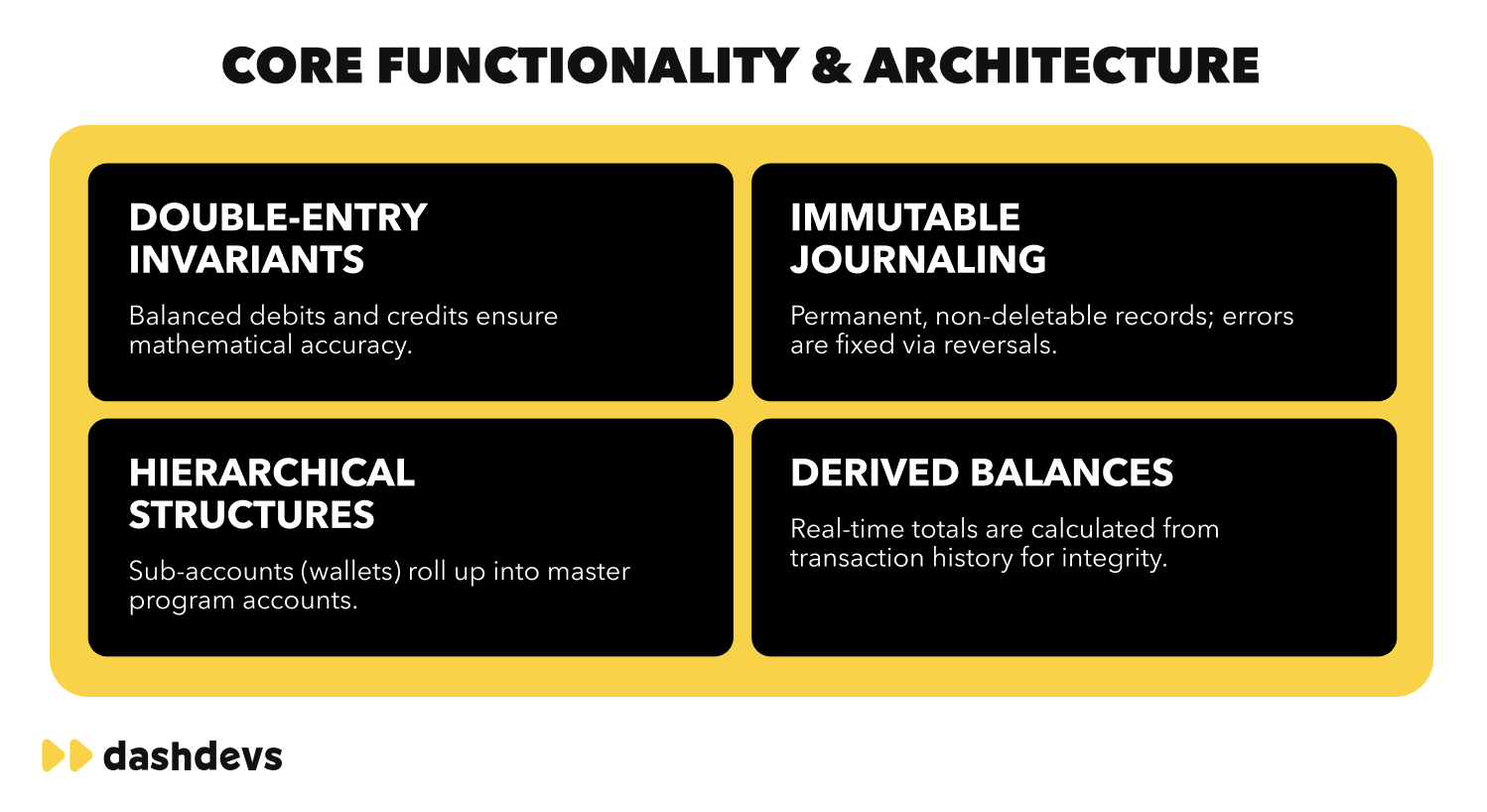

When teams ask “is our Postgres schema a financial ledger system?” the answer usually hinges on invariants, not storage. A transaction ledger in the strong sense is not only append-only events; it enforces which postings are valid, which accounts they may touch, and how balances and sub-balances (pending, available, held) are derived. A pure event log with balance recomputation in application code can work if the rules are central and testable, but the moment you fork those rules per service, you have exited the “single source of truth” property even if a single database still stores the bytes.

| Dimension | Transaction log / generic event store | Financial ledger system (multi-account) |

|---|---|---|

| Primary job | Persist what happened | Define what is allowed, derive balances, keep accounts consistent |

| Balance | Recomputed in app code (often per service) or not first-class | Balances and sub-ledgers (pending, held, available) are part of the model |

| Rules | Ad hoc, scattered in services | Posting rules, account types, invariants enforced at write time |

| Disputes and reversals | May be new rows without a clear link to original posts | Reversals, chargebacks, and adjustments post against defined accounts and links |

| Change impact | A new “kind” of event is easy; semantic drift is easy too | A new product flow extends the chart of accounts and posting types deliberately |

Productized ledgers and vendor-hosted infrastructure

In documentation you will still see the phrase ledger as a service in vendor decks. The useful idea behind that label is that ledger infrastructure can be productized: posting APIs, idempotent event ingestion, account schemas, and reporting hooks, so product teams are not re-solving double-entry on every feature. The implementation path—buy, build, or compose—depends on your jurisdiction, your banking partners, and how much of the model you need to own. What does not work is treating any provider’s reporting portal as a substitute for your own ledger system of record for customer-facing money. A vendor can host the ledger; your organization still has to own the product semantics—what a fee is, which entity earns it, and which balance moves when a dispute opens.

What “multi-account” means beyond “many users”

“Multi-account” is not only “many users.” It is many account types with different invariants. A payment ledger for card capture behaves differently from a stored-value wallet, which behaves differently from a credit line, even if the same customer experience touches all three. Your model must know how to represent each without corrupting the others. For example, a card authorization is not yet settled money; a wallet debit might be; a draw on a line creates different exposure and interest accrual rules. A multi-account design names those ledgers and their relationships so support and finance are not reverse-engineering the business from a flat list of “transactions” with opaque tags.

| Account class | Why it shows up in a platform | Typical expectations |

|---|---|---|

| User wallets or stored value | P2P, pay-in, spend, refunds | Real-time available vs pending, holds, limits |

| Merchant or sub-merchant balances | Marketplaces, platforms | Split logic, rolling reserves, payouts |

| Internal operational and float accounts | Treasury, working capital, fee recognition | Reconciliation to bank, audit trails |

| Settlement and provider clearing | PSP batches, card networks, ACH windows | Cut-offs, idempotent settlement posts |

| Partner or program accounts | BaaS, sponsor banks, program managers | Entitlements, pass-through, reporting boundaries |

The key principle: record once, reflect everywhere, in real time

The key principle is that all financial movements are recorded in one coherent transaction ledger model and that balances derive from the same rules everywhere they surface. That is how a fintech ledger system becomes an operational asset rather than a back-office afterthought. In practice, “real time” means: after a posting commits, any API that serves balance reads the same result (subject to your caching policy), and the same post drives customer notifications, limit checks, and finance extracts. A failure mode to watch is “fast” reads that skip posting rules, which reintroduces the multi-version balance problem in a new costume.

If your organization also moves money through multiple payment rails, it helps to read how we describe electronic payment services and orchestration: the payment ledger and routing layer must agree on which events are authoritative when the same business moment touches more than one provider. Orchestration without a clear ledger is routing without accountability; a ledger without orchestration is accurate books that never connect to a working checkout.

How a multi-account ledger system solves these problems

When a multi-account ledger system is in place, the benefits stack: visibility, controlled reconciliation, integration resilience, and product velocity, all on the same transaction ledger and payment ledger rules.

Real-time insight into position (without pretending settlement is instant)

The first shift is visibility. Balances, pending states, and holds are not “eventually consistent hopes”; they are properties of the ledger system with clear semantics. That does not remove every delay imposed by a bank file or a network settlement window; it does mean the platform knows it is waiting and can show a truthful pending state to users and to finance. For a marketplace, that might mean a seller can see “funds in clearing” and an expected value date, instead of a blank screen that generates support tickets. For a lender, it might mean a draw is visible as a liability the moment the contract says it is effective.

Reconciliation as validation, not a forensic project

The second shift is in reconciliation mindset. If postings are idempotent, events are versioned, and the transaction ledger records both sides of money movement, then reconciliation work becomes validation—matching expected settlement batches to what already posted—instead of a forensic search across silos. Strong platforms pair that with payment reconciliation automation for the predictable bulk of work and reserve human time for true exceptions. You still reconcile; you stop living inside spreadsheets as the primary system of record. A concrete win: a daily settlement file that used to require three hours of manual triage becomes exception-only review because “already posted, batch matched, variance zero” is the default.

A single source of truth for product, books, and regulators

A third benefit is a single source of truth for product, finance, and compliance. The same financial ledger system that powers the app can feed controlled extracts for the general ledger and regulatory reporting, with fewer brittle joins. That is when audit conversations become about policies and access controls, not about whether two exports use the same definition of “available balance.” Diligence questions such as “show us a complete trail for this customer for Q2” turn from a multi-week project into a query with guardrails, because the transaction ledger is already the spine.

Integrations that add rails without redefining your core

Fourth, integrations stop breaking internal logic every time a provider changes a file or adds a new event type, because the provider is integrated as a source of financial events into a known posting pipeline rather than as a private truth that each service interprets differently. Payment orchestration patterns often sit next to a fintech ledger system in mature architectures: routing decides which path money takes, while the payment ledger records what the platform must treat as true. When a new network adds a return reason code, you extend the posting catalog and mapping, not a dozen if-statements in random services.

Centralized control of pricing, fees, and product rules

Finally, control returns to the product organization. You cannot wish away sponsor banks, schemes, and regulators, but you can choose where the platform enforces invariants. When financial logic is centralized, pricing experiments, new products, and country expansion reuse the same ledger system instead of replicating ad hoc rules in three services and a task queue. That is the difference between “we can A/B a fee in two sprints” and “we can A/B a fee if three teams agree on a migration plan.”

How it works in practice

Operationally, every meaningful financial event—authorization, capture, refund, transfer, fee, interest accrual, chargeback, manual adjustment—arrives as an input to the same posting layer. The following mechanics are how high-performing teams keep that promise at scale.

One posting pipeline, many event sources

The transaction ledger records each event with the metadata future investigations need: which account, which product, which legal entity, and which idempotency key. That is how support can answer a customer with something stronger than “we see it on the provider portal sometimes.” A practical rule used in production systems: the same idempotency key a client sent must map to the same posting outcome, whether the first response was a timeout or a 200, so double-spend and duplicate credits from retries are not “handled in support.”

How balances are derived, not “edited” in the database

Balances are then derived, not hand-maintained, so the account always reflects a consistent state after each accepted post, including pending and settlement stages your product promises to show. The implementation details vary: double-entry, posting layers, and subledgers to the general ledger are common patterns, described in the broader ledger guide; the architectural invariant is the same for a payment ledger in a wallet product or a more complex financial ledger system in a banking stack. Hand-editing a balance in SQL is an emergency break-glass, not a design pattern—if you need a manual “true-up,” it should be a posted adjustment with an audit reason, the same as any other financial event.

How money flows end-to-end: pay-in, float, fee, pay-out, settlement

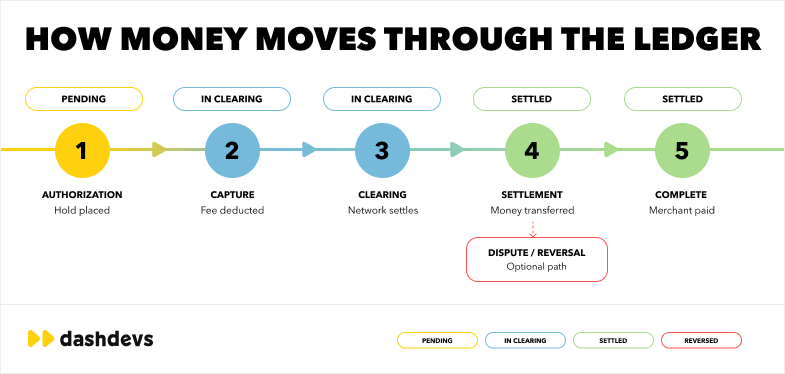

A mature design also makes all financial flows traceable in one picture: how pay-ins become spendable balance, when fees and FX hit, and how pay-outs settle against operational accounts. A helpful exercise for leadership workshops is to pick one end-user journey and walk the ledger: the funds land in a clearing account, a slice moves to fee income, a slice remains in transit for settlement, a reserve posts on a merchant. If that story cannot be told without opening five systems, the platform is still a collection of tools, not a financial product with a clear transaction ledger at the center. For readers comparing stacks, our overview of what core banking is can clarify how a ledger and core modules relate in banking use cases, even when your product is not a full bank in the traditional sense.

| Stage (example card or wallet) | What usually happens on the network or PSP | What the platform’s ledger should make explicit |

|---|---|---|

| Authorization / intent | Hold or pre-check; not final settlement | Pending exposure, user-visible “reserved” or “processing” if you promise that |

| Capture / presentment | Merchant capture; may batch | Movement from pending to a clearing or settlement path; correct fee treatment |

| Clearing | Network or scheme clearing, amounts net or gross | Splits, FX, interchange-related postings if you recognize them in product |

| Settlement to sponsor or bank | Money actually moves on bank rails; files arrive | Reconciliation: batch matches what already posted, exceptions only |

| Dispute / chargeback | Reversal, representment, possible loss | Linked reversal postings; reserve release or liability movement |

The labels differ by rail (card, SEPA, RTP, local schemes); the point is a single multi-account ledger system names each leg so product copy and support scripts do not improvise a fifth vocabulary.

External systems as inputs: PSP, bank, and file formats

External systems do not disappear—they remain essential—but they feed the fintech ledger system. The PSP is not the ledger system of record for your product unless you have consciously chosen that risk and have the controls to match. In practice, that means: webhooks, statements, and settlement files confirm and reconcile what you already modeled; they do not become the only place where a balance exists. That separation is what lets you change acquirer without rewriting your product’s view of a customer’s wallet.

A useful rule: if your engineers cannot list which service owns a balance dispute in two sentences, you do not yet have a multi-account ledger system; you have a set of services that happen to talk about money.

Business value of a unified multi-account ledger

The return on a serious ledger system investment is easy to under-model because many benefits sit in opex, risk, and time-to-market rather than a single new revenue line.

| Outcome | What improves | Example |

|---|---|---|

| Visibility | Decisions on liquidity, risk, and expansion | You see end-of-day float and exposure without a manual merge |

| Cost | Reconciliation, support, and finance hours | Exception queues shrink; fewer “rebuild the month” events |

| Velocity | Reuse of posting rules and accounts | A new card product reuses the same payment ledger invariants |

| Control | You define fees, holds, and disputes | Not every change requires a vendor ticket |

| Compliance | Traceable, consistent data | Diligence and audit answers are process, not firefighting |

| Scalability | New rails without a rewrite | Mappings and accounts extend; core semantics stay stable |

Better decisions, faster, because numbers match

The first business outcome is decision quality. When leadership sees a faithful real-time (or honest near-real-time) view of balances and pending exposure, you make different choices about working capital, pricing, and market expansion. A scenario we see often: treasury discovers only at month’s end that a new cohort’s behavior created float risk because “available” in the app was not the same as “freed for settlement” in the bank. A unified view does not remove risk; it makes it legible in time to act.

The hidden opex in reconciliation and exceptions

The second is cost. Reconciliation, finance operations, and exception handling are some of the largest opex lines that never appear on a pitch deck. A coherent ledger system does not remove operations; it reduces the proportion of unplanned work, which is what scales margin. A rough rule of thumb from mature programs: the cost curve should bend—each doubling of volume should not require a linear doubling of reconciliation headcount. If it does, the architecture is paying a tax the P&L often books under “G&A” instead of under “product debt.”

Product velocity: ship features on a stable spine

The third is speed to ship. A product team that reuses a stable fintech ledger system can add a new instrument or flow without renegotiating the laws of physics in three microservices. That is the practical meaning of “scalability without system redesign” in board language. New flows become configuration and new posting types, not new shadow databases. That is also how you avoid a “fintech of microservices, each with its own view of a penny” anti-pattern that sinks velocity.

Control, trust, and compliance that survive diligence

Control and compliance follow. Clear audit trails in the transaction ledger make reporting a matter of process and access policy, not heroic reconstruction. That is the difference between a team that can pass diligence and a team that promises diligence “soon.” For regulated or partner-heavy models—sponsor bank, scheme membership, or EMI—the partner’s first technical question is often: show us how you know what the customer is owed, end to end, with segregation of funds where required. A multi-account ledger system is the part of the stack that can answer with diagrams and data, not with narrative alone.

When do you need a multi-account ledger system

Not every pre-seed project should build a heavy financial ledger system on day one, but the warning signs arrive earlier than most teams expect.

| Signal in the org | What it often really means | Strong prompt to act |

|---|---|---|

| “Which balance is right?” every sprint | No single financial ledger system of record; channels read different snapshots | Unify read path from posted balances; freeze definitions for “available” and “pending” |

| Reconciliation is hiring faster than product | Drift and exceptions scale with volume; you are funding manual merge | Post expected settlement; automate matching; reserve humans for true exceptions |

| New PSP launch needs a re-plan every time | Per-rail shadow logic, not a composable payment ledger and posting pipeline | Refactor to event → map → post once; new rail is mapping work |

| Auditors or partners ask for a trail; you need a war room to answer | Narrative, not a queryable transaction ledger with audit fields | First-class account, entity, and idempotency on every post |

| You cannot A/B a fee or hold without three teams | Business rules and balances are coupled across services | Centralize invariants; extend posting types instead of forking code |

You run multiple money-moving products on shared customers

You should treat a multi-account ledger system as a serious program when you operate multiple financial products that touch the same customers or balances. If someone can have a card, a wallet, and a line of product in the same app, the alternative to one model is three reconciliation stacks and a permanent identity-merge problem. If you are building in that direction, the discussion in how to build a digital bank applies even for non-bank brands: the surface area is the same at the data layer.

You already juggle more than one provider or bank

A second trigger is when you already run multiple providers or banks, because each will ship its own “truth” in its own time zone. Without a single transaction ledger, you will spend your architecture budget on stringing files together. With one, a new file format is a mapping problem on a known spine.

Reconciliation and support have become a team, not a task

A third is when reconciliation is a team rather than a task: if every close involves war rooms, or if support’s average handle time is dominated by “we need to check with finance,” you are past the point where a spreadsheet policy will scale.

You cannot answer balance questions in one place, in one definition

A fourth is when real-time balance questions block sales, partnerships, or support because no one can sign off on a number. That is a direct signal that the financial ledger system is not yet product-grade.

You plan to scale into new markets or entity structures

A fifth is when the roadmap includes new markets with different settlement cycles, tax handling, and local rules. A fragment-friendly architecture makes every launch a reimplementation; a multi-account design makes most launches a matter of new accounts, mappings, and controls on the same engine.

If you are a platform with marketplace payouts, any delay in a coherent payment ledger becomes a trust problem for both sides of the market. The same is true for digital banks and EMI-style products: a fragmented fintech ledger system is how banks accidentally train customers to doubt their own balances.

Build vs buy: choosing the right approach

There is no universal answer, but the trade space is learnable, and the wrong choice is usually “none of the above—forever in spreadsheets.”

| Approach | Strengths | Risks | Typical fit |

|---|---|---|---|

| Build in-house | Maximum control, tailored invariants | Time, cost, hiring, long-term ownership | Mature fintech, ledger as core IP |

| Fragmented “best of breed” tools | Quick launch on narrow scope | Reconciliation, drift, complex changes | Prototypes, narrow MVPs with exit plan |

| Modular platform (core + modules) | Speed with shared ledger semantics | Must validate vendor flexibility | Most scaling product companies |

Building in-house: when the ledger is the product

Build in-house when ledger differentiation is the product and you have the senior engineering and financial operations talent to run it. In that world, your moat may be how you model risk, float, and multi-currency, not only your mobile UX. The cost is not only build time: it is ongoing ownership—schema evolution, compliance changes, and performance under peak loads. The upside is that you are not waiting on a vendor’s roadmap to ship a new fee structure your regulator just approved.

Fragmented tools: fast until they are your architecture

Fragmented tools feel fast in month three and painful in month eighteen, because you still have to build the invariants the tools do not share. A payout tool, a KYC store, a rewards engine, and a CRM can all be “best in class” and still not add up to a single transaction ledger. Teams that go this route should plan a deliberate consolidation phase before volume and regulation lock the mess in.

Modular platforms: speed without giving up a coherent model

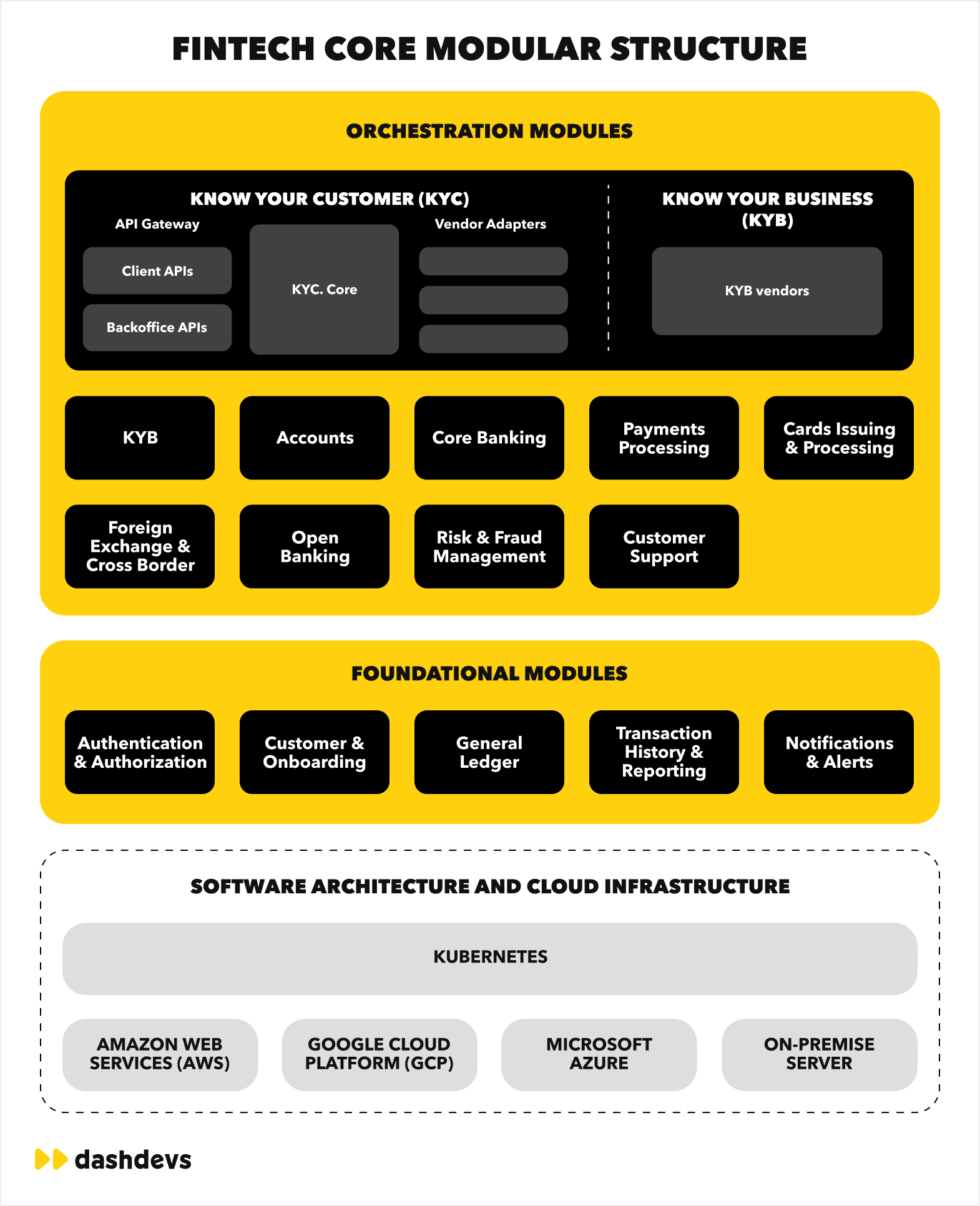

A modular fintech platform is often the balanced path: not a black box that blocks your differentiation, and not a from-scratch core ledger build repeated by every product team in isolation. The evaluation criteria are unglamorous and decisive: can you add an account type without a full migration? Can you get posting APIs and idempotency that match your compliance story? Can you run your own back-office and reporting on top, without turning the vendor’s UI into the system of record? That is the class of Fintech Core style architectures we build with when product velocity has to meet regulatory reality in the same release train.

How Fintech Core enables a multi-account ledger system

DashDevs Fintech Core is designed for teams that need a unified fintech ledger system without painting themselves into a corner. The goal is a single place to model accounts, post transaction ledger events, and expose the APIs and operational surfaces product teams need, while still fitting into real bank and PSP ecosystems.

Unified backend for money movement and state

A unified backend means the same ledger system that powers your customer-facing money view also underpins the operational and settlement accounts your treasury team reconciles, instead of a parallel set of “shadow” balances in spreadsheets. The practical benefit is fewer reconciliation classes: you are not maintaining two different definitions of “settled” because marketing used one database and operations used another.

Real-time visibility and reconciliation that match how money actually moves

That means real-time visibility and reconciliation-friendly exports by design, not as a bolt-on. In practice, product teams can expose pending, cleared, and failed states with consistent semantics, while finance can still close books on a schedule. The “real-time for users, batch for GL” model is a normal pattern, but both sides need to be derivable from the same transaction ledger.

Integrated payment orchestration and posting discipline

It also means integrated payment and orchestration around a coherent ledger model, so routing decisions and postings do not drift from each other—similar in spirit to what we have delivered in large-scale payment orchestration programs, but generalized for teams building end-to-end financial products. When a retry changes rails, the ledger still knows the user intent, the idempotency key, and the final outcome, without duplicate settlement risk.

Modular structure: grow products without replatforming every year

The modular structure matters because fintech scaling is rarely a single straight line. You add a country, a payment method, or a B2B flow; a rigid stack forces rewrites, while a modular ledger system should absorb new account types and posting rules with engineering effort that is proportional, not explosive. If your roadmap for the next 18 months includes more than one of “new scheme,” “new sponsor,” or “entirely new product line on the same customer,” that proportionality is the economic argument for a shared core in the first place.

Case example: Dozens digital banking platform

The challenge: multiple flows, partners, and regulatory expectations in one app

Dozens is a UK digital banking case where the product story depended on a coherent back end: not only mobile screens, but consistent financial data, regulator-grade behavior, and the ability to evolve without losing operational control. The challenge is familiar to many teams: multiple financial flows and integrations, strong compliance and conduct expectations, and a market that will not forgive balance mistakes—especially when trust is the product.

The approach: a unified transaction ledger and modular architecture

The through-line in such programs is a unified ledger and modular architecture so accounts, transactions, and partners do not each invent their own reality. Instead of a separate “ledger project” at the end, accounting and customer-facing balance semantics are part of the same design conversation from the first release train. That is how you avoid a mobile app that looks polished while the back office is still the real source of truth for “what the customer can spend.”

The outcome: consistent data, lower reconciliation load, and room to grow

In outcomes language, the platform reduces reconciliation drama because teams are not triangulating three sources for every business day. It creates room for product growth because the infrastructure can extend when new propositions are introduced. That is the same class of value a multi-account ledger system is meant to provide: a foundation that can carry the business when traffic and product scope expand at the same time. The lesson for readers is not to copy a single vendor stack, but to copy the discipline: one ledger system of record, clear mappings from rails to posts, and leadership that will not trade away financial clarity for a short-term feature checklist.

Common mistakes fintechs make

Treating the ledger as a “phase two” system

The first mistake is treating the ledger as a secondary component you “add when volume appears.” Volume is when defects hurt most; the ledger system is easier to get right before entitlements and workarounds calcify in application code. A classic failure mode: promo credits implemented as a separate table, forever unsynchronized with the main balance, and eventually someone builds a “true balance” field that only the founder understands.

Letting the provider’s portal become the product’s truth

The second is relying on providers for financial truth in places where the customer contract is with you. You may rely on a sponsor or processor operationally, but the fintech must still own the customer’s understanding of their money and the audit trail of how it moved. If support has to “check Stripe” to answer a wallet question, you have outsourced the customer relationship at the data layer, not just the payment rail.

Delaying a real transaction ledger model until a migration is riskier than the launch

The third is delaying a proper transaction ledger model because feature shipping feels more urgent. The tax is paid in delayed launches later—because every shortcut becomes a data migration, often under pressure. Migrations of money state are the highest-risk work in fintech; they deserve the same test harness discipline as your payments integration.

The biggest product risk in fintech is not that a single payment will fail. Networks and retries handle that every day. The deeper risk is inconsistent money state: when users, finance, and partners see different balances and nobody can say which is authoritative without a war room.

Final thoughts

A multi-account ledger system is not a theoretical elegant diagram. It is the mechanism that makes fintech products legible: to your customers, to your finance team, to your partners, and to your future you who has to add another country in twelve months. Without it, the financial ledger system of your product lives in parts—some in providers, some in services, some in human effort. That is how scaling becomes operational drag before it becomes a revenue story.

The strategic risk, in one sentence, is not payment failure but lack of financial consistency at the moment the business needs trust most—during disputes, during audits, and during growth. A unified multi-account ledger system is the antidote: a single, disciplined place where a transaction ledger and payment ledger tell the same story the business and the regulator can defend.

Early investment in the right ledger system and payment ledger invariants is often cheaper than a re-architecture after the facts are entangled. If you are at the point where the roadmap and the reconciliation load are both growing, it is a good time to make the multi-account decision explicit, not “some day after launch.” If your mobile and core ambitions are on the same roadmap, the way we often structure learning for teams—see our mobile banking development guide for the product and delivery side—applies in parallel: great UX on top of unclear money state does not last a funding cycle.

Contact DashDevs to map your current transaction ledger and target multi-account ledger system on a timeline your product and compliance teams can both defend.

Share article