Open Banking Infrastructure Explained: How Brankas Powers Embedded Finance

March 18, 2026

Open banking is no longer a side topic for fintech teams. It is production infrastructure.

If you are building embedded finance products, the question is no longer “Should we use open banking?” It is “Do we have an open banking stack that can support growth without breaking customer trust, compliance obligations, or unit economics?”

That distinction matters. The UK FCA reported more than 16 million active open banking users and 53% year-over-year growth in open banking payments in 2025. Adoption is real, and expectations are rising. Customers now expect fast account linking, smooth pay-by-bank checkout, transparent consent flows, and reliable post-payment status.

At the same time, many companies still treat open banking as a connector project. They wire an API, pass compliance checks, and move on. Then scale arrives: more banks, more use cases, more edge cases, and more operational pressure.

This is where infrastructure strategy separates teams that scale from teams that stall.

In this article, we explain how open banking infrastructure actually works, why it matters for embedded finance, how Brankas fits into this landscape, and what executives should prioritize before integration debt starts compounding.

“Instead of building a bank from scratch, companies can partner with infrastructure providers to access pre-built rails and focus on the product experience.” - Fintech Garden episode 108

From a CEO viewpoint, open banking infrastructure should be treated as a growth multiplier only when it improves three outcomes at once: faster launch of new use cases, lower cost-to-serve per transaction, and stable conversion under peak volume. If one of those three gets worse over time, the stack is likely creating hidden debt.

If you want a wider strategic baseline before implementation choices, this overview of trends in banking to follow helps align infrastructure priorities with market direction.

| Executive objective | Infrastructure question to ask | Early warning signal |

|---|---|---|

| Revenue growth | Can we launch a new bank flow in weeks, not quarters? | Integration timelines keep increasing |

| Margin protection | Does automation reduce manual payment/consent ops? | Support workload grows with volume |

| Risk control | Can we prove consent/payment state in audits quickly? | Incident root cause takes days |

What is open banking infrastructure?

Open banking infrastructure is the combination of technical rails and regulatory controls that allow authorized third-party providers to access account information and initiate payments with customer consent.

In plain business terms, it is the operational foundation behind:

- account aggregation

- pay-by-bank checkout

- financial-data-driven onboarding

- automated reconciliation workflows

- embedded payments and money movement experiences

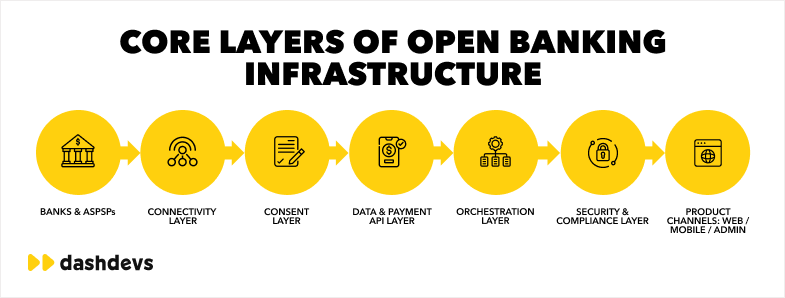

Most explainers stop at “bank APIs.” That is only one layer. Real open banking infrastructure usually includes:

| Layer | What it does | Why it matters commercially |

|---|---|---|

| Connectivity layer | Connects to banks and financial institutions | Determines coverage and go-live speed |

| Consent layer | Manages customer permissions and revocation | Determines trust and compliance resilience |

| Data/payment API layer | Retrieves account data and initiates payments | Determines product capability and UX quality |

| Orchestration layer | Normalizes formats, routes requests, handles retries | Determines reliability and operating efficiency |

| Security/compliance layer | Applies IAM, logging, auditability, controls | Determines risk posture and regulator readiness |

When this stack is designed well, product teams can launch and iterate quickly. When it is not, every new partner increases fragility.

If you need the baseline API concepts first, start with DashDevs’ open banking API guide. It gives a broad foundation before deeper architecture decisions.

For teams comparing API models and standards in more detail, this API in banking guide is also useful.

Open banking vs embedded finance: what leaders should not confuse

Open banking and embedded finance are connected, but they are not interchangeable.

Open banking is infrastructure. Embedded finance is distribution.

Open banking gives you access to account data and payment initiation rails. Embedded finance is the business model that uses those rails inside non-bank products: marketplaces, SaaS tools, payroll apps, e-commerce checkouts, and industry-specific workflows.

This matters because strategy changes by layer:

- Infrastructure decisions affect reliability, compliance, and scalability.

- Product decisions affect conversion, retention, and monetization.

Many teams overinvest in surface UX and underinvest in infrastructure resilience. That trade-off looks good in demos and expensive in production.

The practical leadership mistake is measuring feature delivery but not infrastructure maturity. Teams then celebrate shipped features while conversion losses, dispute handling cost, and integration latency quietly rise.

If pay-by-bank is one of your growth channels, this focused pay-by-bank guide helps evaluate conversion and settlement trade-offs.

McKinsey has framed embedded finance as a fast-growing convergence between financial and non-financial platforms, with winners emerging around infrastructure ownership and distribution leverage.

If your team is defining roadmap priorities, this practical article on embedded finance implementation is a good companion to this infrastructure guide.

“As fintechs evolved, their once-simple models became multi-layered ecosystems.” - Fintech Garden episode 122

Why infrastructure quality now decides embedded finance outcomes

In early stages, many products can survive on basic integrations. At scale, infrastructure quality becomes visible through business metrics:

- checkout conversion

- failed payment rate

- support workload per transaction

- reconciliation speed

- partner onboarding cycle time

Juniper Research projected open banking payment transaction values to exceed $330 billion globally by 2027, up sharply from 2023 levels. As this volume grows, weak infrastructure gets punished faster.

Here is the practical executive view:

| Infrastructure quality | What users see | What the business experiences |

|---|---|---|

| Strong | fast account linking, predictable pay-by-bank flow | lower support cost, faster launch cycles |

| Moderate | occasional linking/payment friction | higher manual ops and patching effort |

| Weak | frequent failures and trust erosion | margin leakage, delayed expansion, compliance pressure |

A good internal benchmark is whether your platform gets easier to operate as volume grows. If operations scale linearly with transactions, architecture debt is already accumulating.

For board-level reviews, add two infrastructure KPIs beside product KPIs: “failed payment journey rate” and “integration lead time by provider.” These two metrics are often enough to detect whether growth is compounding or decaying.

How Brankas powers embedded finance in practice

Brankas (sometimes misspelled as “Brancas”) is one of the notable open-finance infrastructure players in Southeast Asia. Their positioning is relevant for teams building embedded finance in APAC markets where bank connectivity is fragmented and local banking behavior differs by country.

Based on public customer stories, Brankas supports use cases such as:

- direct bank payments in checkout experiences

- disbursements and payout flows

- account opening journeys

- API partnership infrastructure for financial ecosystems

Examples include public case stories with PayMongo, UNObank, and PERA HUB, where embedded banking/payment flows were integrated into broader product experiences.

From an architecture perspective, providers like Brankas typically matter most when a team needs:

- regional connectivity acceleration,

- standardized API operations across banks,

- compliance-friendly consent and security flows,

- faster time to market for embedded finance products.

The strategic decision is not “Brankas or custom.” It is usually “which capabilities we should rent now, and which capabilities we should own over time.”

That ownership split should be explicit in the business plan. A clear model might be: rent regional bank connectivity early, own orchestration and risk policy logic in-house, and review this split every two quarters as transaction volume and margin targets change.

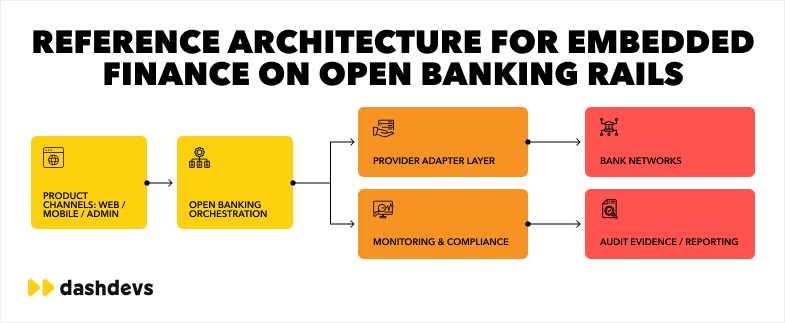

What a production-ready open banking architecture looks like

A production-ready stack is less about one API and more about clean boundaries between provider integration and product logic.

A practical architecture often follows this flow:

Product channels -> Open banking orchestration layer -> Provider connectors -> Bank networks

Inside the orchestration layer, mature teams usually centralize:

- consent lifecycle states,

- account-linking event logic,

- payment status normalization,

- retry and timeout policies,

- monitoring and evidence logging.

This separation protects product teams from provider-specific complexity and makes future provider changes less disruptive.

| Component | Common anti-pattern | Better pattern |

|---|---|---|

| Consent handling | consent logic scattered across frontends/services | centralized consent service with auditable state |

| Payment status | provider-specific statuses in product code | normalized internal status model |

| Error handling | ad hoc retries per integration | centralized retry and fallback policy |

| Observability | logs by service only | business-event observability across flows |

| Provider strategy | hardwired single provider | adapter pattern with controlled switching path |

If your integration layer is currently tightly coupled, the fintech integrations guide gives useful context on designing cleaner API boundaries.

For a provider-integration checklist, this guide on integrations with open banking providers can help your team avoid common rollout pitfalls.

Where teams usually fail (and how to avoid it)

Most failures are not caused by one broken endpoint. They are caused by architecture and governance choices that seemed harmless early.

In executive terms, these are not technical mistakes alone. They are operating-model mistakes: unclear ownership, underfunded reliability work, and no governance cadence tied to business targets.

1) Treating integration as a one-time project

Open banking integrations are living systems. Bank-side behavior changes, provider APIs evolve, and compliance expectations tighten. If you budget only for launch, operations debt appears quickly.

2) Building product logic around provider specifics

When payment and consent behavior are implemented directly against provider contracts, every provider change becomes product risk.

3) Ignoring consent UX and edge-case states

Consent failure and timeout paths are often underdesigned. Customers experience this as “your product does not work” even when the bank is the failing component.

4) Underinvesting in observability

Without business-event tracing, incident response slows dramatically. Teams spend hours proving where a failure occurred.

5) No clear ownership model

If no team owns cross-provider reliability and compliance evidence, issues stay unresolved across squads.

| Mistake | Technical consequence | Business consequence |

|---|---|---|

| Launch-only integration mindset | fragile post-launch operations | rising support and incident cost |

| Provider-specific product logic | high change propagation | slower roadmap and integration velocity |

| Weak consent flow design | high drop-off and user confusion | lower conversion and trust |

| Poor observability | slow root-cause diagnosis | longer downtime and higher SLA risk |

| Diffuse ownership | unresolved reliability gaps | unpredictable performance and accountability |

“Vendor relationships can make or break a product’s success.” - Fintech Garden episode 110

One practical rule: if infrastructure incidents are discussed only in engineering meetings, leadership is already too far from the risk surface.

Vendor concentration risk should be managed explicitly, and this article on how to avoid vendor lock-in traps gives a practical starting point.

Regulatory alignment should also be reviewed early, especially for multi-market products; this summary of fintech regulations for businesses US, EU, UK, MENA is relevant here.

Build vs buy vs hybrid for open banking infrastructure

This is the most practical decision for CTOs and founders. There is no universal winner.

Buy-first approach

Best when speed is the top constraint and the use case is relatively standard.

Build-first approach

Best when infrastructure logic is a competitive differentiator and the team has enough domain and engineering maturity.

Hybrid approach

Often the most pragmatic route: launch with provider infrastructure, then progressively own orchestration, risk controls, and key product logic.

| Model | Best when | Main risk | Typical mitigation |

|---|---|---|---|

| Buy-first | fast launch, limited in-house open banking expertise | provider lock-in | adapter layer + clear exit criteria |

| Build-first | long-term control is a strategic priority | slower time to market | phased rollout + strict scope control |

| Hybrid | need both speed and ownership over time | complexity of transition | architecture roadmap from day one |

For many teams, the right strategy is hybrid with explicit checkpoints every 2-3 quarters to decide what to keep external and what to internalize.

The value of a hybrid is commercial leverage. It gives a faster initial launch while keeping a path to better margin control and lower dependency over time.

For teams evaluating ownership strategy in regulated products, this guide on how to build a neobank using vendors, platforms, or APIs adds useful decision context.

DashDevs’ perspective: infrastructure is only valuable if operations stay sane

DashDevs has been involved in open banking and integration-heavy fintech programs where architecture choices directly affected speed and cost.

A strong reference is the Tarabut Gateway case study, where regulatory constraints, ecosystem complexity, and scaling goals had to be balanced in one delivery model.

The core lesson from this type of work is consistent:

- Teams do not fail because they picked the “wrong API.”

- Teams fail when architecture governance is weaker than business growth pressure.

That is why we recommend evaluating open banking stacks across three dimensions at once:

- product velocity (can we ship safely and often?),

- operational resilience (can we detect and recover fast?),

- strategic flexibility (can we evolve provider strategy without major rewrites?).

To make this actionable, assign an executive owner to each dimension. Without named ownership, these decisions drift into tactical compromise, and debt reappears quickly.

If your team is comparing providers, DashDevs’ open banking providers overview is useful for shortlisting, while financial data aggregation guidance helps with data-layer architecture decisions.

What most competitor guides miss about open banking infrastructure

After reviewing common provider and explainer content in this space, the same pattern appears: most articles explain definitions and API flow basics, but skip the operating model that determines whether embedded finance is profitable after launch.

The missing layer is usually execution governance. Teams get advice on account connectivity and payment initiation, but less guidance on ownership boundaries, failure accountability, incident cost control, and vendor-switching readiness.

For executive teams, those are not edge details. They are the difference between a scalable platform and a permanently fragile one.

| Topic | Common competitor coverage | What leadership actually needs |

|---|---|---|

| Open banking vs embedded finance | definitions and examples | ownership model and P&L impact |

| API integration | onboarding and auth flows | post-launch reliability and change cost |

| Provider selection | feature comparisons | switching risk and governance maturity |

| Compliance | high-level regulatory overview | evidence model, controls, and operating responsibilities |

If your internal planning still looks like “integration project” instead of “infrastructure operating model,” this fintech architecture guide can help reset the framework.

Executive KPI scorecard for open banking infrastructure

Most teams track product KPIs and treat infrastructure as engineering telemetry. That creates blind spots. Infrastructure needs its own executive KPI layer tied directly to conversion, cost, and risk.

A practical scorecard should be reviewed monthly at the leadership level and weekly by delivery leads.

| KPI | Why it matters | Healthy direction | Escalation trigger |

|---|---|---|---|

| Account-link success rate | top-of-funnel conversion | stable or improving | sustained drop over 2 releases |

| Failed payment journey rate | direct revenue leakage signal | trending down | spike after provider changes |

| Mean time to resolution (MTTR) | incident cost and trust impact | trending down | recurring multi-hour incidents |

| Support tickets per 1,000 transactions | operational efficiency | flat as volume grows | grows faster than transaction volume |

| Provider onboarding lead time | expansion agility | predictable and shortening | large variance by provider |

| Consent re-auth drop-off | retention and repeat usage | stable or improving | steady erosion in returning cohorts |

This scorecard gives CEOs and product leaders a simple answer to one core question: is our open banking infrastructure compounding growth, or compounding risk?

Provider due diligence checklist before signing contracts

Selecting Brankas or any other provider without a due diligence framework creates avoidable risk. The right process is not “which provider has more features.” It is “which provider fits our operating model and risk appetite.”

Use these contract-stage questions before signing:

| Due diligence area | Question to validate | Why it matters |

|---|---|---|

| Coverage quality | How many institutions are production-ready in our target markets? | prevents expansion assumptions from failing later |

| Reliability model | What are real uptime, latency, and failover commitments? | protects conversion and SLA expectations |

| Incident workflow | Who owns triage, evidence, and resolution timelines? | reduces ambiguity during outages |

| Data model stability | How often do payloads/status semantics change? | influences change-management overhead |

| Sandbox quality | Does test data reflect real production edge cases? | reduces launch surprises |

| Commercial terms | What costs scale with volume or extra endpoints? | protects margin as usage grows |

| Exit readiness | How hard is it to migrate critical flows away? | limits long-term vendor lock-in |

For teams formalizing this process with procurement and product, a structured how to write RFP approach helps keep decisions measurable and comparable.

12-month scaling blueprint: from launch to resilient infrastructure

A lot of embedded finance programs move from pilot to complexity shock in under a year. A simple 12-month blueprint helps avoid that jump.

Quarter 1: launch with control boundaries

Go live with one or two high-priority journeys, but define architecture boundaries from day one: where provider logic ends, where product logic starts, and where observability lives.

Quarter 2: stabilize and instrument

Focus on failed-journey reduction, status normalization, and incident response discipline. Add business-event tracing before adding major feature scope.

Quarter 3: optimize unit economics

Use KPI data to improve conversion, reduce support load, and refine consent/payment paths. This is the quarter where margin gains usually become visible.

Quarter 4: expand with governance

Only expand providers/markets after establishing repeatable onboarding, risk controls, and executive ownership for infrastructure decisions.

| Quarter | Primary goal | Success signal |

|---|---|---|

| Q1 | controlled launch | reliable core journeys in production |

| Q2 | reliability and observability | lower incident volume and faster triage |

| Q3 | efficiency and margin | lower cost-to-serve per transaction |

| Q4 | scalable expansion | faster provider/market rollout with predictable risk |

This roadmap turns open banking from a feature dependency into an infrastructure asset.

Conclusion

Open banking infrastructure is no longer optional plumbing. It is a strategic growth layer for embedded finance products.

Brankas and similar providers can accelerate launch and reduce initial complexity, especially in fragmented regional ecosystems. But long-term outcomes depend on architecture discipline: normalization, orchestration, observability, and clear governance.

The teams that win are not the ones with the most integrations. They are the ones with the cleanest operating model behind those integrations.

If you are building or scaling embedded finance, treat open banking infrastructure as a product capability with executive ownership, not a background integration task.

Share article