Real-Time Trading Platform Development: What It Takes to Process 1,000 Orders per Second

July 4, 2026

Summary

Key takeaways

- Real-time trading platform development is a coordinated system — OMS, matching engine, trigger monitor, ledger, and liquidity router — not a single matching algorithm.

- Each order type (market, limit, stop) and time-in-force modifier (IOC, FOK, GTC) is a distinct execution contract with its own validation, storage, and failure modes.

- Throughput at 1,000 orders per second turns invisible latency into queue backlog, race conditions, and retry-driven duplicate fills unless idempotency and atomic balance reservation are designed in from day one.

- Trade execution is not complete until the ledger is correct — double-entry settlement and transactional outbox patterns belong in the hot path, not as downstream afterthoughts.

- Dopay demonstrates production-grade crypto-fiat trading: price-time priority matching, USDC intermediary routing, platform liquidity fallback, and an off-chain trade ledger under concurrent load.

- Available, reserved, and settled balances are three distinct ledger states — conflating them is the fastest path to overdrafts, phantom fills, and reconciliation nightmares under concurrent order submission.

- Market data feeds, trigger monitors, and matchers have different freshness requirements; stale tick data silently breaks stop orders long before the matching engine shows stress.

At 09:31:04.218, a user submits a market order for 0.4 BTC. By 09:31:04.241, their EUR balance is reserved, a counterparty is matched, a fill is recorded, two ledger legs post, and a confirmation event lands in the UI. Twenty-three milliseconds. One atomic financial truth.

That number is not the hard part. The hard part is the other 999 orders arriving in the same second — each with its own order type, time-in-force rule, reservation state, and dispute potential if anything lands half-written. Real-time trading platform development is where fintech engineering stops tolerating eventual consistency and starts treating every millisecond as a liability surface.

Most teams discover this too late. They ship a matching engine demo, wire up a price chart, and call it a platform. Then production load arrives: concurrent reservations race, stop triggers fire on stale ticks, retries duplicate fills, and the ledger no longer sums to zero. The UI still says “filled.” The finance team knows otherwise.

This guide is for CTOs, engineering leads, and product owners deciding whether to build, rebuild, or evaluate trading infrastructure. It explains why traditional application patterns break under exchange-grade load, how market, limit, and stop orders each rewrite the architecture, what actually happens between submit and filled, and why 1,000 orders per second is a different problem — not a faster version of ten. It draws on DashDevs’ work on Dopay, a crypto-fiat exchange with USDC intermediary routing, internal matching, and platform liquidity fallback — plus the reference architecture, latency budgets, and load-test scenarios we use when a trading UI has to stay financially honest at volume.

Why real-time trading is harder than it looks

Every trading platform has two layers. The visible layer is the one your users interact with: a price ticker, an order form, a confirmation toast. The invisible layer is everything that has to happen correctly for that confirmation to be true — order validation, funds reservation, matching against a live order book, execution, ledger updates on both sides of the trade, and an auditable record of what just occurred.

Most engineering intuition comes from systems where correctness is important but not existential, and where a slow response is an annoyance rather than a liability. Trading systems break that intuition in three specific ways.

State changes must be atomic. A half-completed order — funds reserved but no trade recorded, or a trade recorded but a balance not updated — is not a bug you patch later. It is a discrepancy between what the platform believes and what is financially true, and it compounds with every order that follows. Mature fintech trading platform development programs reach for patterns rarely needed elsewhere: write-ahead logs for durability before acknowledgment, single-writer ownership per account or instrument, and idempotent state machines instead of imperative update-and-hope logic.

Latency is a product feature, not just a technical metric. In most software, a 200ms delay is invisible. In a trading system, the same delay changes the price a user actually gets, changes whether a limit order matches before the book moves, and directly affects platform competitiveness. Teams building high-frequency trading infrastructure track latency as a distribution — p50 tells you almost nothing; p99 and p99.9 tell you what your worst-treated users experience, and in trading, the tail is where regulatory and reputational risk lives.

Errors are financial events, not just bugs. A null pointer in a reporting dashboard is an inconvenience. The same class of failure in an execution path can mean an order fills at the wrong price, a balance is double-counted, or a user is charged for a trade that never completed. Deterministic replay — reconstructing exact system state at any past point by replaying the event log — is a hard requirement, not a nice-to-have. When a fill is disputed, “we believe this is what happened” is not an acceptable answer.

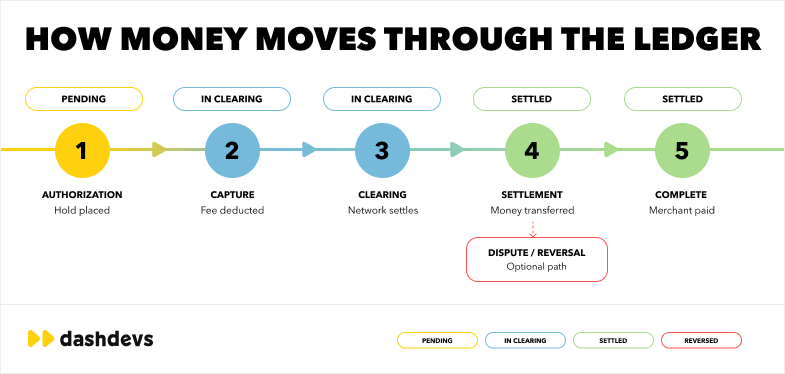

Trade execution is not complete until the ledger is correct. Execution and settlement are not the same step — and treating them as one is a common source of state that looks fine in the UI but is wrong underneath.

The compounding complexity is structural: each order type adds a distinct execution path, each concurrent user adds contested state, and each millisecond of delay has a direct, measurable cost. None of this complexity is visible in a UI mockup. To understand why matching engine architecture looks the way it does, it helps to first understand what the system is actually being asked to process.

Order types and why each one changes the architecture

It is tempting to treat order types as a UI-layer detail — a dropdown with a few options. In practice, each order type is a distinct execution contract with its own lifecycle, storage requirements, and failure modes. A platform that supports five order types needs five validated execution paths, not one order matching engine with flags bolted on.

Market orders

A market order executes immediately against the best available price in the book. There is no waiting, no resting state — the order either fills now at whatever price is available, or it does not fill at all.

Architecturally, this requires real-time access to the live order book at submission, logic to handle partial fills and slippage when liquidity at the top level is insufficient, and balance reservation that happens before execution, not after. A market order that executes before funds are confirmed available is a direct path to an overdraft. Reservation is usually implemented as a pessimistic lock on available (not total) balance, excluding funds tied up in open orders — a distinction that breaks under concurrent submission if implemented carelessly.

Limit orders

A limit order only executes at a specified price or better, which means it may rest in the order book until a counter-order arrives, gets cancelled, or expires.

This changes the storage model entirely. Limit orders need persistent, queryable state and a defined lifecycle — open, partially filled, filled, cancelled — with transitions tracked and exposed in real time. Most limit order books are modeled as a sorted map of price levels (red-black tree, skip list, or flat array indexed by tick size), where each level holds a FIFO queue enforcing time priority within a price level. That queue makes price-time priority a property of the book itself rather than something recomputed on every match.

Stop orders

A stop order is dormant until a trigger price is hit, at which point it activates as either a market or limit order. Until triggered, it should not be part of the active book — it lives in a separate monitoring layer evaluating incoming price data against pending triggers.

This is one of the more consequential architectural decisions in the whole system. A common implementation groups pending stops into a min/max-heap or bucketed index keyed by trigger price, so each incoming tick only checks stops near the current price — O(log n) trigger evaluation versus a linear scan that degrades as the platform grows.

Time-in-force modifiers: IOC, FOK, GTC

Time-in-force rules layer on top of order type and change how the matching engine resolves partial matches:

- IOC (Immediate-or-Cancel): fill whatever is available right now, cancel the remainder immediately.

- FOK (Fill-or-Kill): fill the entire order in one shot, or cancel entirely — partial fills are not allowed.

- GTC (Good-Till-Cancelled): the order persists until fully filled or manually cancelled.

FOK requires the matcher to evaluate whether sufficient aggregate liquidity exists across the book before committing — simulate the fill first, confirm full quantity, then commit. A naive level-by-level greedy match produces incorrect partial fills on orders that should have been killed. IOC FOK GTC orders against the same book can produce completely different outcomes for functionally similar submissions, which is why they need distinct, well-tested code paths.

Every order type is a distinct execution contract, not a UI variation. Treating them as interchangeable is one of the fastest ways to introduce subtle matching bugs — the kind that only surface under specific book conditions and are extremely difficult to reproduce after the fact.

What happens behind one trade

To make the invisible layer concrete, walk through the full lifecycle of a single order from submission to audit record.

- Order submission. The user submits via API or UI — asset pair, order type, quantity, price (if applicable), time-in-force.

- Validation. Parameter checks, circuit-breaker ranges, account permissions, and pre-trade risk gates — max position size, max order value, rate limits per account.

- Balance reservation. Relevant funds are locked before matching begins to prevent double-spending under concurrency — typically a conditional decrement with optimistic concurrency control rather than a long-held database lock.

- Routing. The order enters the order management system (OMS). Stop orders route to the trigger-monitoring layer instead of the active book.

- Matching. The order matching engine applies price-time priority against the active book. High-performance implementations often run one single-threaded matcher per instrument — the single-writer principle removes locking from the hot path.

- Execution. Full or partial fill recorded; counterparty order state updated.

- Ledger update. Internal balances adjusted on both sides — part of execution, not a side effect. Financial-grade trade ledger implementations use double-entry postings where every trade produces balanced debit and credit entries.

- Confirmation event. Status updates emit to both users; audit record written. The transactional outbox pattern writes the event in the same database transaction as the trade, with a publisher relaying to the event bus at least once and consumers deduplicating on trade ID.

- Fallback path. If no internal match, route to platform liquidity fallback / market-maker layer.

Pre-trade risk checks at validation mirror the gatekeeping regulators expect under market-access rules — the same category of control covered in depth in KYC and fraud detection for fintech apps, where velocity limits and anomaly monitoring protect execution paths before bad orders enter the book.

The three-balance model most platforms get wrong

Production order management system (OMS) design almost always requires three balance states per asset, not one:

| Balance state | Definition | Typical failure if missing |

|---|---|---|

| Available | Funds free to spend or allocate to new orders | User submits two orders against the same cash; both pass validation |

| Reserved | Funds locked for open orders or in-flight execution | Overdraft after partial fill leaves reservation stale |

| Settled | Funds reflecting completed ledger postings | UI shows “filled” while ledger still shows pre-trade balance |

Reservation moves value from available to reserved before matching. Execution moves reserved to settled (and adjusts counterparty balances) in the same atomic transaction as the fill record. Cancellation releases reserved back to available. Teams that model only “balance” and “pending” often discover the gap during the first concurrent load test — when two market orders both pass a single-balance check milliseconds apart.

For crypto-fiat platforms like Dopay, the model applies per asset leg: a user buying BTC with EUR needs EUR reserved at submission, but BTC credited only after settlement — and USDC intermediary hops may introduce a transient third leg that must be tracked in the ledger, not approximated in the UI.

1,000 orders per second — why throughput creates new problems

Every step above works fine sequentially at low volume. At ten orders a second, a mostly-synchronous pipeline validates, reserves, matches, executes, and logs without noticeable delay. At 1,000 orders a second, the same pipeline hits problems that do not exist at low volume.

Concurrency and race conditions. Two orders can hit the same liquidity at the same instant. If balance reservation is not atomic, both can pass a check only one should have passed — the path to overdrafts and phantom fills.

Order book contention. High-frequency updates to the same price levels mean many writers competing for the same state. Without lock-free structures or sequenced writes, the book becomes the bottleneck. Event-sourced, single-writer architectures — the pattern popularized by systems like the LMAX Disruptor — process a sequenced stream of pre-validated commands on one thread, removing lock contention from the critical path.

Latency accumulation. A 2ms validation step is invisible at 10 orders per second. At 1,000, that 2ms multiplied across every order and downstream consumer is the difference between a responsive platform and a queue that never drains. Performance-sensitive components favor append-only, in-memory-first structures with durable commit logs over synchronous database writes on every hot-path step.

Retry and idempotency risk. At scale, network retries are routine. Without idempotency controls, a retried request produces duplicate trade events and ledger entries that no longer reflect reality. Client-supplied idempotency keys checked against a short-lived deduplication store before acceptance are among the highest-leverage safeguards in the system.

Observability gaps. At volume, a stuck order or missed trigger is silent by default unless the system is instrumented to surface unmatched orders, stale prices, and missed stop triggers. Latency percentiles, queue depth metrics, and reconciliation jobs that verify the ledger sums to zero stop being nice-to-have and become the primary way anyone finds problems before users do.

The cascade problem. Delayed ledger updates back up confirmations. An unresponsive UI generates retries. Retries add load to a system already behind — a feedback loop that turns local slowdown into platform-wide incident. Mature systems break the loop with backpressure: rate limiting at the gateway, circuit breakers between services, and queue-depth-aware admission control that rejects orders explicitly rather than accepting them into a falling-behind pipeline.

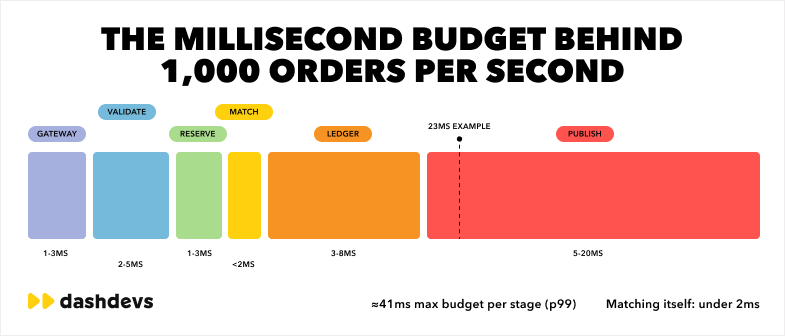

Latency budget at 1,000 orders per second

At target throughput, every stage needs an explicit budget. These are representative internal SLOs for a retail crypto-fiat platform — institutional high-frequency trading infrastructure targets are tighter, but the discipline is the same:

| Pipeline stage | Typical p99 budget | What blows the budget |

|---|---|---|

| Gateway + auth | 1–3 ms | JWT validation hitting a remote store on every order |

| Validation + risk | 2–5 ms | Synchronous DB lookups instead of in-memory account cache |

| Balance reservation | 1–3 ms | Row-level locks held across network calls |

| Matching | sub-ms to 2 ms | Lock contention on shared book structures |

| Ledger + outbox write | 3–8 ms | Synchronous cross-service RPC before ack |

| Event publish + UI push | 5–20 ms | Blocking on WebSocket fan-out before order ack |

If validation and ledger writes each consume 5ms p99, end-to-end p99 exceeds 15ms before matching runs — and queue depth grows linearly with arrival rate. That is why hot-path components stay in-memory with durable logs, and why the matcher acks only after the commit log records the fill, not after every downstream consumer has processed it.

These are the exact failure modes that shape production trading platform architecture. Here is how DashDevs encountered and addressed them while building Dopay.

Dopay — how DashDevs built this in practice

Project context

Dopay is a platform that lets users exchange crypto and fiat assets against each other. The core challenge was not any single component — it was supporting multiple order types, matching users directly, and gracefully falling back to platform liquidity when no internal match existed, all while keeping an off-chain trade ledger accurate under concurrent load.

What DashDevs built

| Component | What it does |

|---|---|

| Crypto/fiat trading logic | Unified execution across asset classes |

| USDC intermediary layer | Bridges crypto/fiat pairs via stablecoin routing |

| Market, limit, and stop orders | Full order type coverage with distinct execution paths |

| GTC / IOC / FOK behavior | Time-in-force logic wired into matching resolution |

| User-to-user order matching | Internal book matching before external routing |

| Price-time priority | Deterministic, auditable match sequencing |

| Internal balance updates | Real-time reservation and settlement |

| Off-chain trade ledger | Full record of every execution event |

| Platform liquidity fallback | Market-maker layer for orders that do not match internally |

| Foundation for future integrations | Architecture ready for live charts and third-party liquidity providers |

The full program is documented in the digital assets trading platform case study — a licensed fintech stack combining fiat, stablecoins, and crypto liquidity with automated risk controls.

A notable design choice: the USDC intermediary layer

Crypto/fiat platforms face a combinatorial problem: every asset pair multiplies order books, pricing feeds, and matching paths. Supporting even a modest set of crypto assets against multiple fiat currencies directly requires a dedicated book, feed, and path for every pair — and every new asset multiplies that surface.

Routing trades through a USDC intermediary layer collapses complexity: instead of managing N×M direct pairs, the system manages conversions in and out of a single stable asset — an exponential integration problem becomes linear.

The trade-off is an extra conversion step on some trades and stablecoin-specific considerations — peg risk and issuer counterparty exposure — that a purely fiat ledger would not carry. In exchange, the platform gets simpler pair management, a single deep liquidity pool to route through, and a smaller surface to test, monitor, and reconcile as new assets are added.

Engineering decisions that survived production load

Three choices on Dopay matter more in retrospect than any single algorithm:

USDC as hub, not every direct pair. EUR→BTC and BTC→EUR do not each maintain independent deep books. Both route through USDC conversion legs with explicit spread and fee postings in the trade ledger — so reconciliation can prove each hop balanced independently. When a leg fails mid-route, the system can unwind or hold in USDC without corrupting unrelated balances.

Internal match first, platform liquidity second. User-to-user matching runs to completion before the liquidity fallback router engages. That ordering prevents unnecessary external exposure and keeps spread revenue on-platform when natural counterparties exist — but it requires the router to detect “no match” quickly, not time out waiting for a book that will never fill.

Single-writer matcher per symbol shard. BTC/EUR and ETH/EUR each get a dedicated matching thread fed by a sequenced command queue. Cross-symbol contention disappears; scaling adds shards, not threads fighting over one book. The OMS still handles cross-asset reservation — the matcher never touches balances directly.

On a trading platform, the matcher should not know user balances, and the ledger should not decide match priority. Blurring those boundaries is how teams ship fast and reconcile slowly.

What this took

None of this was built as a single matching engine with everything else attached. It was a coordinated system: an OMS for lifecycle and validation, a matching engine for execution, a trigger monitor for stop orders, a ledger service for settlement, and a liquidity router for fallback. Each is a natural service boundary with different consistency requirements, scaling characteristics, and failure modes — the kind of divergence that justifies separation rather than monolith deployment.

Teams planning greenfield real-time trading platform development should map these boundaries early. The modular service patterns in fintech system architecture — policy separated from execution, event logs for replay, reconciliation as a first-class concern — apply directly to trading stacks.

Reference architecture: five services and their contracts

Before debating cloud vendor or language, define service boundaries and consistency requirements. This is the reference model DashDevs used on Dopay and applies to most real-time trading platform development programs:

| Service | Owns | Consistency model | Scales by |

|---|---|---|---|

| OMS | Order lifecycle, validation, reservations, user-facing state | Strong per account | Horizontal sharding by account ID |

| Matching engine | Order book, price-time priority execution | Single-writer per instrument shard | Adding symbol shards |

| Trigger monitor | Stop and conditional orders pre-activation | Eventual (ms-level) on price ticks | Partitioning by price range or symbol |

| Ledger service | Double-entry postings, balance truth | Strong, transactional | Account-based sharding |

| Liquidity router | External fallback, market-maker integration | At-least-once with idempotent hedge | Async workers + rate limits |

The OMS publishes commands; the matcher emits fill events; the ledger consumes fills and confirms settlement. No service skips the event log — if the matcher crashes mid-batch, replay reconstructs book state from the log, not from a database snapshot taken minutes ago.

Architecture principles that hold at scale

The specifics of Dopay are project details. The principles generalize to any real-time trading system.

Separate the OMS from the matching engine. The OMS owns lifecycle, validation, user state, and trigger logic. The matching engine owns execution only. Mixing them creates one component scaling for two different workloads — I/O-heavy validation versus CPU-bound matching — which usually means it scales well for neither.

Keep stop orders out of the active book. Stop orders belong in a dedicated monitoring layer and enter the active book only once triggered. An active book evaluating conditional logic on every price tick degrades as resting stop volume grows — exactly when volatile markets already stress the matcher.

Use deterministic matching rules. Price-time priority must be consistent, documented, and auditable. Users and regulators need to reconstruct why a fill happened — the practical foundation of best-execution obligations. Non-deterministic tie-breaking is a liability the moment anyone asks why an order filled at that price.

Treat ledger updates as core infrastructure. A trade that executes but leaves an incorrect balance is a financial liability immediately. Double-entry accounting turns reconciliation from forensic investigation into a query that either sums to zero or does not.

Design for idempotency. Idempotency keys on every mutating request, deduplication at every event consumer, and “set to value X given prior state Y” operations instead of blind increments wherever the ledger allows.

Build for observability from day one. Latency histograms per pipeline stage, continuous automated reconciliation between ledger and custody balances, and alerting on the absence of expected events — a stop that should have triggered but did not — not just explicit errors.

API design for order submission, balance queries, and fill notifications should follow the same idempotency and versioning discipline described in the API in banking guide — trading endpoints face the same retry storms and audit requirements as payment APIs, with higher financial stakes per millisecond.

Market data: the layer teams under-scope

Stop orders, circuit breakers, mark-to-market risk checks, and UI price displays all depend on a market data layer that is logically separate from the order matching engine. Conflating “price on screen” with “price that triggers a stop” is a recurring production bug.

| Feed type | Freshness requirement | Typical source |

|---|---|---|

| Display ticker | 100ms–1s acceptable | Aggregated websocket push |

| Stop trigger evaluation | Tick-level, gap-aware | Internal trade prints + external reference |

| Pre-trade risk / circuit breaker | Sub-second, monotonic sequence | Reference mid with staleness flag |

| Fallback pricing | Deterministic snapshot at route time | Platform liquidity quote, not last UI tick |

When external reference feeds lag, triggered stops may fire late — or not at all. Production systems stamp every tick with sequence ID and source timestamp; the trigger monitor rejects stale inputs rather than silently using outdated prices. On Dopay, USDC reference rates for intermediary legs use the same staleness rules as crypto pairs — a fiat user seeing a fresh EUR/BTC quote while the router prices off a stale USDC leg is a classic cross-asset reconciliation failure.

Build vs. integrate: where to own and where to buy

Not every layer rewards custom engineering equally. For fintech CTOs evaluating fintech trading platform development scope:

| Layer | Build custom when… | Integrate when… |

|---|---|---|

| Matching engine | You need full control of price-time rules, internal crossing, and audit replay | You operate a broker-dealer model routing to external venues only |

| OMS | Order types, reservation logic, and risk gates are product differentiators | MVP scope is single-asset, single order type |

| Ledger | Multi-asset, multi-leg (USDC hub) settlement is core | Simple single-currency wallet suffices |

| Market data | Internal crossing sets the reference price | You rely entirely on external exchange feeds |

| Custody / fiat rails | Never — regulated counterparty | Always partner; build orchestration only |

Dopay owned matching, OMS, ledger, and routing because internal crossing and USDC hub logic were the product. Custody, banking, and compliance integrations were partners — the engineering value was orchestrating them into one coherent execution path, not rebuilding regulated infrastructure.

Disaster recovery and deterministic replay

Regulators and dispute teams ask: prove this fill at 14:32:07.412. That requires an append-only event log capturing every order command, fill, cancellation, and ledger posting in sequence. Snapshots accelerate recovery, but the log is the source of truth.

Replay workflow for incident response:

- Freeze new submissions (kill switch at gateway — not at matcher; you want to stop ingress, not strand in-flight reservations).

- Restore matcher state by replaying commands from last known good sequence number.

- Reconcile ledger sum-to-zero per asset; compare against custody balances.

- Re-enable ingress only after discrepancy count is zero or explicitly waived with human sign-off.

Teams that treat the database row as truth without an event log cannot replay — they can only guess. That gap surfaces the first time a user disputes a fill the support team cannot reconstruct.

Common mistakes fintech teams make

A few patterns show up repeatedly in teams building trading infrastructure for the first time:

- Treating matching as the whole problem. The matching engine is often less than a third of production engineering effort once OMS, ledger, and fallback layers are accounted for.

- Building one execution path for all order types. Flags crammed into a generic path become unmaintainable when a second or third order type arrives.

- Skipping balance reservation. Processing before funds are locked is a direct path to race conditions under concurrent load.

- Ignoring partial fills. Partial execution is routine in any real order book — not an edge case to defer.

- No idempotency on execution events. Retry logic without idempotency keys is a leading cause of duplicate trades and ledger corruption.

- Deferring observability. Monitoring added after launch means operating blind during the period most likely to encounter unexpected load.

- Conflating execution and settlement. Confirmations before ledger update create a window where UI state and system state diverge.

- Underestimating reconciliation. Without automated jobs verifying ledger against custody or exchange balances, discrepancies surface via angry users or auditors instead of the system itself.

Getting the matching algorithm right is a necessary condition for a production trading platform — it has never been a sufficient one.

Checklist for teams evaluating trading infrastructure

Before you build:

- Defined all order types and execution contracts individually?

- Balance reservation atomic and occurring before execution?

- Stop orders in a separate trigger layer, outside the active book?

- Matching engine enforcing price-time priority deterministically?

During development:

- OMS and matching engine architecturally separated?

- Every execution path handling partial fills correctly?

- All execution events idempotent?

- Ledger update synchronous with execution, not downstream?

- Ledger double-entry with automated reconciliation against source-of-truth balances?

Before launch:

- Observability into open orders, failed orders, and liquidity — including per-stage latency, not just end-to-end?

- Load-tested at or above target throughput, including burst cancellations and volatile stop triggers?

- Liquidity fallback path for orders without internal match?

- Every fill reconstructable from audit records independent of live state?

Load-test scenarios that expose real defects

Checklist items above are necessary but not sufficient. These scenarios routinely break platforms that passed happy-path testing:

| Scenario | What it stress-tests | Pass criteria |

|---|---|---|

| Burst submit + cancel | Reservation release, book cleanup, idempotency | Zero orphaned reservations after 60s |

| Stop storm on volatile tick | Trigger monitor lag, matcher ingress spike | All eligible stops fire within staleness SLO |

| Empty book + market order | Liquidity fallback routing, slippage handling | Fill or explicit reject — never hang |

| Duplicate client retry | Idempotency store, dedup on fill events | Exactly one ledger posting per intended order |

| Single-shard saturation | Hot-symbol contention | p99 matcher latency stable; no cross-shard bleed |

Run reconciliation continuously during tests, not after. A fill rate of 99.9% with a ledger that does not sum to zero is a failed test.

For a broader view of platform scope — asset classes, regulation, and modular infrastructure choices — see how to build a trading platform in 2026. The present article focuses on the execution path and throughput constraints that determine whether a trading UI is financially truthful under load.

The bottom line

Real-time trading platform development is not a single engine — it is a coordinated system in which every component, from validation to ledger settlement, must work correctly under load, not just in isolation. The order form is what users see; the OMS, matching engine, trigger monitor, ledger service, and liquidity router determine whether the platform is trustworthy.

Dopay is a working example: full order type coverage, deterministic matching, real-time balance and ledger updates, and a liquidity fallback path built to hold up under production load — not just in a demo.

Building a trading platform or evaluating your current infrastructure? DashDevs has deep experience designing fintech trading platform development programs — from order management and matching logic to ledger integrity and liquidity fallback. Talk to our team.

Share article