How Stablecoins Are Changing Cross-Border Payments for Businesses

July 8, 2026

Summary

Key takeaways

- Stablecoins for cross border payments are production infrastructure in 2026—not a sandbox experiment—for corridors where correspondent banking fees and settlement delays hurt margins.

- Settlement on payment stablecoin rails typically completes in minutes, not the one-to-three business days common on SWIFT-led correspondent chains.

- The GENIUS Act creates a federal framework for US payment stablecoins, but institutional adoption still depends on custody, banking partners, and corridor-specific compliance.

- Cross-border supplier payments, intercompany treasury settlement, and contractor payroll are the three B2B use cases where stablecoin economics clearest beat traditional payment methods.

- Liquidity fragmentation, on/off-ramp friction, and custody counterparty risk remain the primary failure modes—dual-rail orchestration is the pragmatic adoption path.

A €500,000 supplier payment that clears in forty-eight hours is not a treasury inconvenience — it is a working-capital tax. Correspondent banking still moves most B2B cross-border payments through chains of intermediaries, each adding fees, cut-off times, and reconciliation gaps that finance teams absorb as permanent overhead.

Stablecoins for cross border payments are not replacing that stack overnight. They are giving payments and treasury leaders a second rail — one that settles in minutes, runs around the clock, and prices movement more predictably than wire transfers through opaque correspondent networks. The question for mid-market and enterprise operators is no longer whether dollar-pegged settlement rails exist. It is where they outperform traditional cross-border payments, where they fail, and what adoption actually requires.

Stablecoin cross border payments are infrastructure, not a pilot category

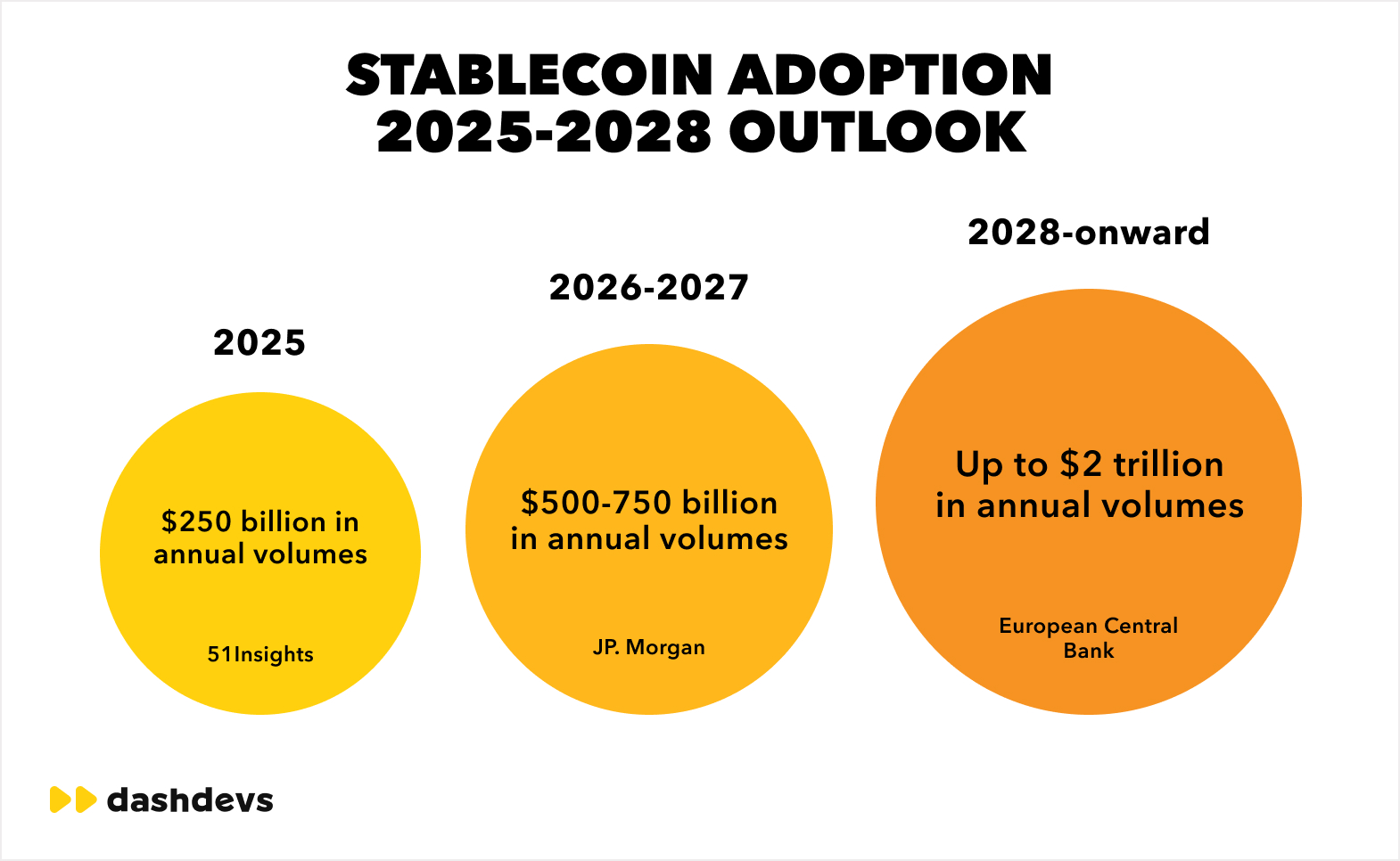

Corporate adoption accelerated after regulatory clarity improved in major markets and issuer scale crossed a threshold institutions could underwrite. Payment stablecoins — dollar-pegged tokens designed for settlement rather than speculation — now circulate at volumes that exceed many national payment systems. McKinsey estimates stablecoin circulation still represents less than one percent of global money flows, but B2B adoption concentrates in corridors where traditional payment methods impose the highest friction: emerging-market supplier bases, multi-entity treasury structures, and contractor networks paid across borders.

That concentration matters for evaluation. Stablecoins are not a universal SWIFT replacement. They are a competing rail for cross-border payments where speed, transparency, and all-hours settlement change unit economics enough to justify operational change.

On Fintech Garden Episode 162, Igor Tomych and David Birch discuss why stablecoins are the pathfinder for digital assets — not a payments novelty, but infrastructure where money and data move together. That operational lens is the right frame for treasury leaders evaluating stablecoins for cross border payments: treat them as payments infrastructure, not as a digital asset bet.

How an on-chain stablecoin transfer actually settles

Treasury teams do not need a blockchain tutorial. They need a clear picture of where money moves, who holds risk at each step, and how fiat currency re-enters the banking system.

A typical B2B flow moves through four layers:

- Initiation — The payer converts fiat currency to USDC or another approved dollar token through a bank, exchange, or institutional on-ramp, or draws on an existing custodial balance.

- On-chain transfer — The stablecoin moves wallet-to-wallet on a public ledger. Settlement is final when the transaction confirms — usually minutes, not days. No SWIFT message chain; no correspondent bank queue.

- Custody — Either party may hold tokens in a qualified custodian, enterprise wallet, or digital wallet provided by a regulated partner. Custody choice determines insurance coverage, key management, and audit posture.

- Off-ramp — The recipient converts stablecoin back to local currencies through a banking partner, exchange, or local payment rail. This step often defines total settlement time and cost more than the on-chain leg.

The on-chain segment is the fast part. On/off-ramp friction — KYC, banking hours, local FX, compliance holds — is where many pilots stall. Benefits of stablecoins for financial institutions and corporates are real, but they accrue only when the full path, not just the ledger transfer, is engineered for repeat use.

For a broader view of how stablecoin payment rails fit alongside fiat infrastructure, see DashDevs’ guide to stablecoin payment rails and why they matter for business.

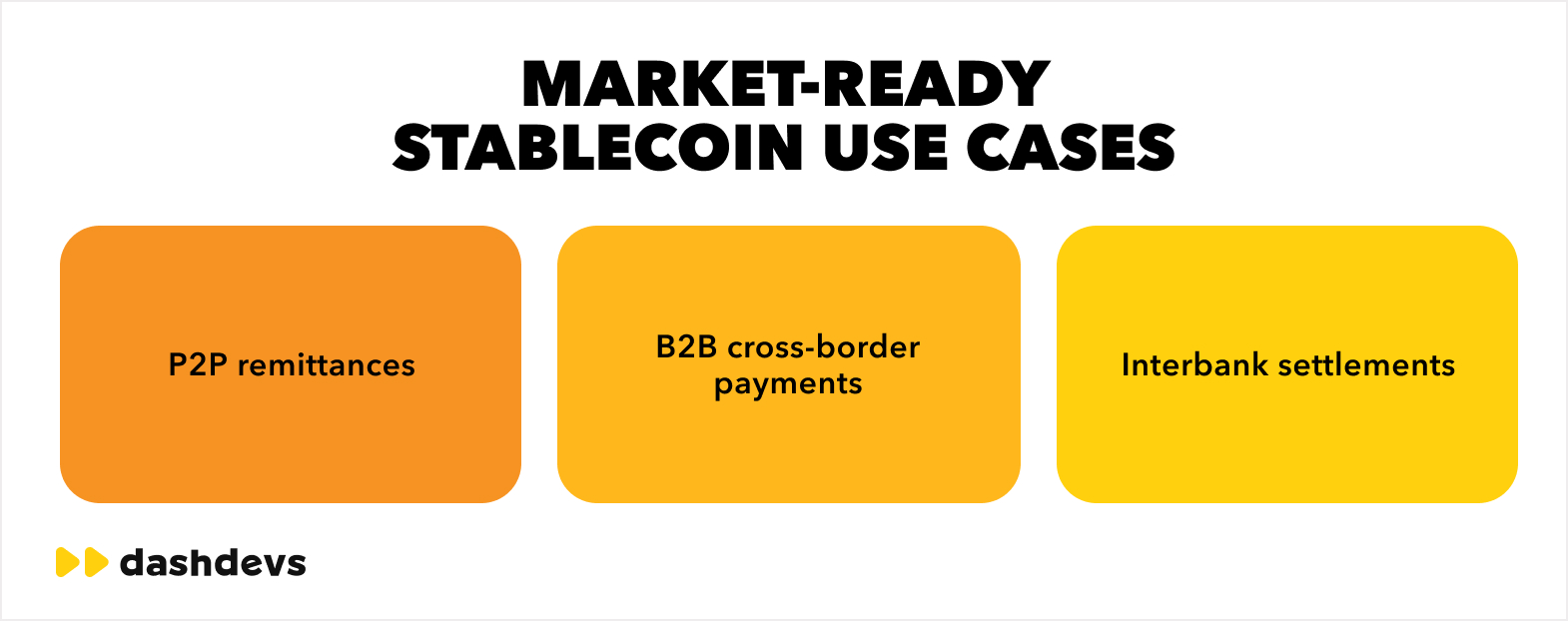

Where businesses use stablecoins today

Cross-border supplier payments

Manufacturers, retailers, and marketplaces paying suppliers in Asia, Latin America, and Africa face the clearest ROI from stablecoin for cross border payments. Correspondent fees on wire transfers often run 1–3% all-in when FX spreads and intermediary charges are counted; on-chain settlement on major networks frequently costs a fraction of that on the transfer leg, with total cost dominated by off-ramp pricing rather than chain fees.

Supplier payments also benefit from traceability. Each transfer carries an immutable on-chain reference — useful when AP teams dispute timing, amount, or status with vendors who previously waited days for SWIFT confirmation.

Intercompany treasury settlement

Multi-entity groups moving cash between subsidiaries traditionally pre-fund nostro accounts or accept two-day settlement windows on internal wire transfers. Tokenized dollar balances let treasury centralize liquidity and distribute to entities on demand — reducing trapped cash and improving cash flow visibility across borders.

This use case demands disciplined governance: which entities may hold tokens, how FX policy applies, and how intercompany balances reconcile against ERP records. It is not a workaround for transfer pricing or tax rules. It is a faster pipe for approved internal movement.

Contractor payroll

Distributed teams expose payroll operations to the same correspondent friction as supplier AP. Contractors in high-inflation or capital-control markets often prefer dollar-linked stablecoin remittances over local bank deposits that arrive late and expensive.

Employers gain predictable disbursement cycles; contractors gain faster access to spendable value. Compliance burden rises — payroll is a regulated activity in many jurisdictions — but the economic case is straightforward where traditional cross-border payments extract double-digit percentages from contractor take-home pay.

These three use cases share a pattern: high volume or high friction corridors where instant payments and transparent settlement outweigh the operational cost of adding a new rail.

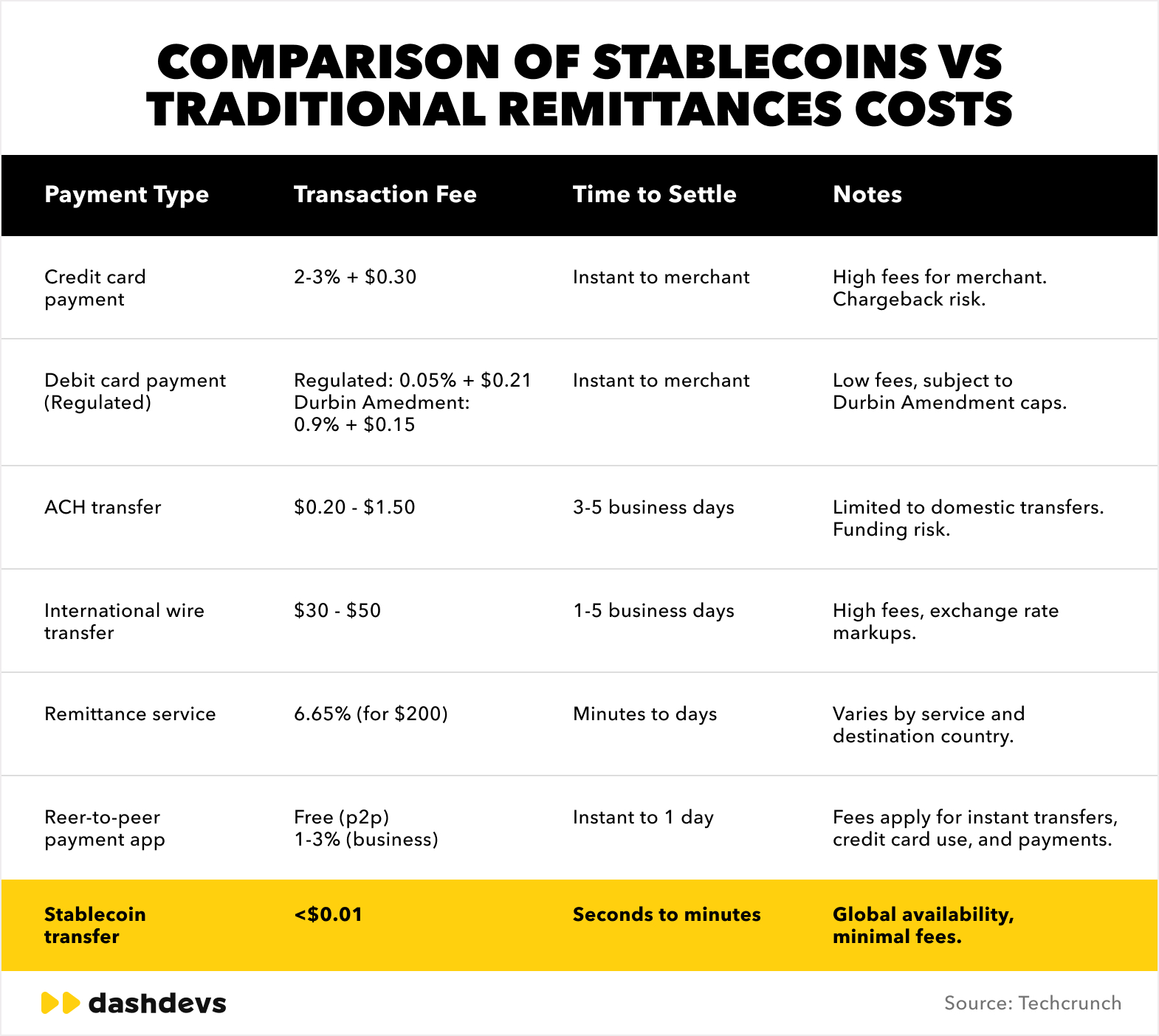

Stablecoins vs. SWIFT and correspondent banking

SWIFT is a messaging layer. It coordinates banks; it does not settle value. Actual money movement still passes through correspondent relationships, compliance reviews, and market-hour constraints. On-chain transfers move value directly — the message and the movement collapse into one step.

| Dimension | SWIFT / correspondent banking | On-chain stablecoin rail | Card rails (cross-border B2B) |

| Settlement time | 1–3 business days typical; same-day possible in select corridors | Minutes on-chain; hours to 1 day with off-ramp included | Instant authorization; settlement and FX timing vary |

| Cost (indicative) | $25–$50 wire fee plus FX spread; intermediaries may add more | Low network fees on major chains; off-ramp and FX dominate total cost | Interchange and cross-border fees; rarely optimal for large B2B transfers |

| Transparency | Fragmented status across banks; limited end-to-end visibility | On-chain confirmation with public transaction record | Merchant-facing status; limited treasury-level traceability |

| Operating hours | Banking hours and cut-offs apply at each hop | 24/7/365 on-chain settlement | 24/7 authorization; settlement windows still apply |

| Operational complexity | Familiar to treasury; bank relationships already in place | Requires custody, compliance tooling, on/off-ramp partners, ERP integration | Simple for small amounts; poor fit for treasury-scale flows |

Competing rails for cross-border payments — banks, fintechs, stablecoins — will coexist for years. The winning model for most enterprises is orchestration: route each payment through the rail that minimizes total cost and settlement risk for that corridor. DashDevs supports that approach through cross-border payment processing and fintech integration services that connect ERP, banking, and digital asset partners without forcing a single-rail bet.

Cost and speed: what treasury should model

Declarative benchmarks help internal business cases:

- Speed: On-chain transfers confirm in minutes. End-to-end supplier settlement including off-ramp commonly lands same-day to next-day — still faster than traditional cross-border payments on correspondent chains.

- Cost: World Bank remittance data shows traditional corridors averaging 6%+ on retail flows; corporate wires often look cheaper per transaction but hide FX spread. Stablecoin payments frequently reduce the transfer leg to under one percent before off-ramp — though illiquid corridors may carry premiums that narrow the gap.

- Cash flow: Faster settlement reduces pre-funding requirements. Treasury teams running nostro-heavy models in multiple local currencies may redeploy idle balances once stablecoin liquidity pools are approved.

These gains are corridor-specific. A payment from London to Singapore on mature banking rails may not justify rail change. A payment from the US to a supplier in Nigeria or the Philippines often does. Model your top ten corridors before building a global policy.

For corridor economics and FX context beyond stablecoins, DashDevs’ overview of cross-border payment and money exchange covers how traditional stacks price movement today.

Regulation after the GENIUS Act and what it changes for institutions

Regulatory frameworks for digital dollar tokens moved from theoretical to operational in 2025–2026. The GENIUS Act — federal US legislation governing payment stablecoins — establishes reserve requirements, redemption standards, and issuer oversight for dollar-pegged tokens that qualify as regulated instruments. That framework gives US institutions a clearer basis to hold and transmit tokens issued by compliant stablecoin issuers without treating every transfer as an unregulated digital asset experiment.

Europe’s MiCA regime already harmonizes issuance and custody rules across the bloc. The UK FCA published consultation papers on stablecoin issuance and prudential requirements. Switzerland maintains an established digital asset service provider framework. The patchwork has not disappeared — but the center of gravity shifted from “unclear” to “conditional yes, with defined guardrails.”

Federal Reserve stablecoin commentary has emphasized financial stability, run-risk on reserves, and the need for bank-grade oversight — cautioning that dollar-pegged settlement tokens must not circumvent deposit insurance and monetary policy transmission mechanisms. That framing matters for treasury policy: regulators treat large-scale adoption as a macro prudential question, not only a payments efficiency question.

Institutional adoption therefore tracks regulated issuers and qualified custodians — not every token on every chain. Stablecoin regulation is the gate; operational readiness is the bottleneck.

Risks and failure modes treasury must stress-test

Honest evaluation requires naming what breaks.

Liquidity fragmentation. USDC on one chain is not perfectly fungible with the same token on another without bridge risk. Issuer concentration creates single-point dependency. Treasury must define approved chains, issuers, and conversion paths — not leave choice to individual AP clerks.

Custody and counterparty risk. Holding tokens in self-managed wallets without institutional controls exposes firms to key loss, insider threat, and uninsured loss events. Qualified custodians and MPC wallet providers reduce but do not eliminate counterparty exposure to the custodian itself.

Regulatory patchwork. A GENIUS Act-compliant issuer does not automatically satisfy every market’s rules. Paying contractors in one country may require local licensing that stablecoin remittances trigger differently than wire transfers. Legal review by corridor remains mandatory.

On/off-ramp friction. The best bridge for cross-border stablecoin payments is only as good as its banking partnerships. Off-ramps freeze, delay, or reject flows that fail enhanced due diligence — exactly when suppliers most need reliability.

Compliance and AML. On-chain transparency aids investigation but does not replace KYC, sanctions screening, or travel rule obligations. Firms that treat blockchain for cross border payment as compliance-light invite enforcement action and partner derisking.

Effective fintech risk management applies fully here: stablecoins change the rail, not the regulatory duty.

What operational adoption requires

Moving from evaluation to pilot demands concrete capabilities — not a wallet and a slide deck.

Custody and banking partners

Define who holds tokens, under what insurance or guarantee, and which banks or regulated fintechs execute fiat conversion. Most enterprises avoid direct private-key management and instead use institutional custodians or payment partners already audited for financial crime controls.

Compliance posture

Document AML policies covering wallet screening, transaction monitoring, and record retention. Integrate blockchain analytics alongside existing KYC/KYB workflows. Payroll and supplier programs need beneficiary verification comparable to wire transfer controls.

Technology integration

Connect on-chain flows to ERP, treasury management, and AP systems. Stablecoin payments that do not reconcile automatically force finance teams into manual work that erases speed gains. Specialized payments-as-a-service providers and integrators reduce build time when internal engineering capacity is limited.

Treasury policy and corridor selection

Approve use cases explicitly: supplier AP above threshold X in corridors A, B, C; intercompany only between listed entities; contractor payroll where local banking is unreliable. Ban ad hoc wallet transfers. Dual-rail policies should specify when SWIFT remains mandatory — regulatory settlements, tax authority payments, or jurisdictions where off-ramps are immature.

Partner ecosystem

Evaluate top cross-border payment companies and stablecoin-native providers on settlement guarantees, not marketing claims. Closed proprietary loops may offer speed but create vendor lock-in similar to legacy banking — understand whether you are buying a closed-loop payment system or open-rail access.

Dual-rail orchestration is the realistic end state

Stablecoins will not eliminate SWIFT, ACH, SEPA, or local instant payment schemes. They will compress settlement time and cost on corridors where correspondent banking extracts the most rent. The enterprises that benefit earliest route each payment through the rail that minimizes total cost and settlement risk — selecting chain, issuer, and fiat exit based on amount, destination, urgency, and compliance tier.

That architecture mirrors how modern fintechs already orchestrate card, bank, and wallet rails — except the stablecoin leg adds a globally portable dollar balance that moves outside banking hours. Stablecoins and monetary policy transmission will remain linked in regulatory debate; treasury teams operate one level below that debate, on concrete corridor economics.

Conclusion

Stablecoins for cross border payments have crossed from experimental to operational for defined B2B use cases — cross-border supplier payments, intercompany treasury settlement, and contractor payroll chief among them. They beat traditional payment methods on speed and transparency where correspondent chains are slowest; they lose when off-ramps are immature, regulation is unsettled, or existing banking rails are already efficient.

Post-GENIUS Act federal standards remove one institutional objection in the US. It does not remove custody decisions, compliance investment, or corridor analysis. The firms that capture value treat on-chain settlement as treasury infrastructure — integrated, governed, and dual-rail — not as a speculative side project.

Evaluate your highest-friction corridors first. Model total cost including off-ramp, not chain fees alone. Build compliance before volume. Stablecoin payments earn their place in treasury when the economics justify the operational work — not before.

Share article