Stanhope for Fintech Payments: How to Launch SEPA, SWIFT, and Multi-Currency Flows Faster

March 15, 2026

Summary

TL;DR

- Stanhope Financial provides API access to global payment rails like SEPA and SWIFT for fintech platforms.

- Fintechs can enable virtual IBANs, multi-currency wallets, and cross-border payments without building banking infrastructure.

- Integrating payment infrastructure providers reduces launch timelines from months or years to weeks.

- Platforms like DashDevs Fintech Core help orchestrate these rails into scalable fintech architectures.

Building payment rails from scratch is one of the hardest parts of launching a fintech product. Teams need scheme access, bank partnerships, compliance controls, treasury logic, reconciliation, and secure money movement infrastructure before the product can scale.

That is why many fintechs use infrastructure providers like Stanhope (Stanhope Financial) instead of building direct connectivity themselves. Through one integration layer, fintech companies can enable:

- SEPA payments across Europe

- SWIFT-based international transfers

- virtual IBANs and named account structures

- multi-currency wallets

- FX conversion and treasury operations

This model helps product teams move faster because they do not have to negotiate and maintain every banking relationship on their own. Stanhope Financial is licensed as an electronic money institution in Lithuania, and Swift says its network connects 11,500+ institutions across 220+ countries and territories. The European Payments Council’s current SEPA scope also now extends beyond the EU and includes new additions such as Albania, Montenegro, North Macedonia, Moldova, and Serbia entering on phased readiness dates.

For DashDevs clients, this is exactly where infrastructure strategy matters. The question is rarely “can we connect to payments?” The real question is “what is the fastest, safest, and most scalable way to do it?”

Why This Problem Exists in the First Place

Sending money looks simple in a product demo. In production, it is not.

A fintech app that supports account funding, payouts, treasury transfers, or international supplier payments usually needs far more than a frontend and a ledger. It needs access to the right banking rails, plus operational layers around them:

- scheme connectivity

- safeguarding and account structures

- AML and sanctions controls

- payment routing

- reconciliation

- liquidity and FX handling

- failure management and monitoring

This is why so many teams underestimate the back-end effort behind “just add SEPA” or “support SWIFT wires.”

The scale of the infrastructure explains the challenge. In 2024, Swift says it averaged 53 million+ FIN messages per day, with 75% of payments reaching destination banks within 10 minutes and 99.999% FIN availability. The eurozone also processed 77.7 billion non-cash payments worth €116 trillion in the first half of 2025, with credit transfers representing more than 90% of total value.

That is the environment fintechs are plugging into.

What Stanhope Financial Actually Is

For this article, the name users search for is often “Stanhop,” but the regulated entity is Stanhope Financial.

Stanhope Financial is licensed by the Bank of Lithuania as an electronic money institution, with licence No. 78 issued on December 17, 2020. The Bank of Lithuania also lists UAB Stanhope Financial among financial market participants and among payment system participants in Lithuania.

In practice, that means fintech teams can use Stanhope Financial as an infrastructure layer to access capabilities such as:

- SEPA payments

- SWIFT transfers

- business accounts

- virtual IBAN structures

- currency exchange

- multi-currency flows

That is a very different path from becoming a direct scheme participant or assembling several banking vendors yourself.

Why Fintechs Use Providers Like Stanhop Instead of Building Directly

The first is to build direct access yourself. That usually means handling banking relationships, compliance design, scheme onboarding, operational support, and routing logic internally.

The second is to integrate a provider that already sits on top of those rails. For most product teams, the second path is the more realistic one.

Build it yourself usually means dealing with:

- banking partner negotiations

- scheme access requirements

- AML and transaction monitoring setup

- safeguarding model design

- treasury and FX relationships

- reconciliation logic

- operational support and exception handling

Integrating a provider usually means:

- one API-led integration path

- faster access to SEPA and cross-border payments

- less fragmented vendor management

- reduced infrastructure risk in the first release

This is similar to what we often explain in DashDevs content around core banking, digital bank architecture, and BaaS provider selection: the bottleneck is rarely code alone. It is orchestration, compliance, and infrastructure fit.

The Rails You Can Enable Through This Model

1. SEPA for European Money Movement

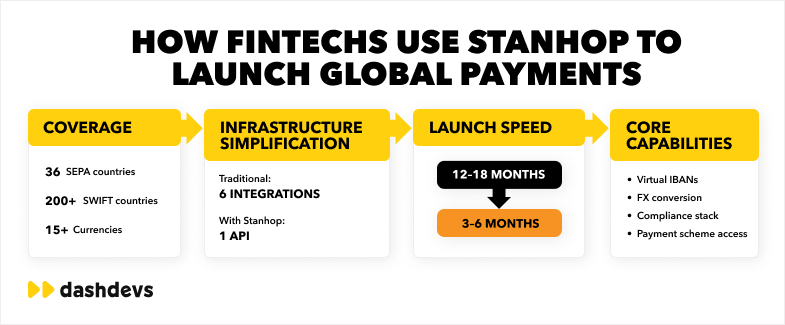

SEPA gives fintechs access to standardized euro payments across a broad European area. The EPC’s current list includes 36 countries and territories, and that scope has expanded further through recent board decisions.

For fintechs, SEPA is useful for:

- wallet top-ups

- merchant settlements

- payroll flows

- customer transfers

- marketplace payouts

- treasury movement inside Europe

The strategic benefit is not just lower-cost euro payments. It is the ability to make your product feel local in Europe.

Good fit for:

- digital wallets

- neobanks

- B2B finance tools

- marketplace and platform payouts

- payroll and expense products

2. SWIFT for Global Coverage

When the product needs broader geographic reach, SEPA is not enough.

Swift says its network connects 11,500+ institutions in 220+ countries and territories, which is why it remains central to international payments.

For fintechs, SWIFT is still relevant for:

- cross-border business transfers

- treasury operations

- supplier payments

- international customer payouts

- corporate and SME payment products

That matters especially for platforms serving import/export businesses, remote teams, global sellers, or treasury-heavy B2B flows.

The challenges of correspondent banking and slow cross-border settlement are discussed in more detail in the Fintech Garden podcast episode “Stablecoins Without the Volatility,” where I explore how new payment rails are reshaping global money movement.

3. Virtual IBANs and Named Receiving Accounts

One of the most practical infrastructure features for fintech products is not the rail itself. It is account structure.

Virtual IBANs let platforms assign a unique account reference to a customer, merchant, or business user while keeping settlement and treasury logic centralized. That is incredibly useful for:

- reconciliation

- customer identification

- pooled account models

- marketplace collections

- fiat on-ramp flows

- treasury segmentation

This is the sort of feature that looks small in product copy but has major operational impact once volumes grow.

4. Multi-Currency Wallets and FX Operations

The more international the product becomes, the more treasury starts to matter.

Multi-currency capabilities help teams avoid building separate operating logic for every new corridor. They make it easier to:

- hold balances in several currencies

- route payouts more efficiently

- reduce unnecessary conversions

- support international merchants or users

- manage internal treasury flows across markets

This is where a payments article should stop sounding like a feature checklist and start sounding like business strategy. Payment infrastructure is not only about “can a transfer happen.” It is also about margin, failure rates, support load, and launch speed.

Where Stanhop Fits in a Real Fintech Architecture

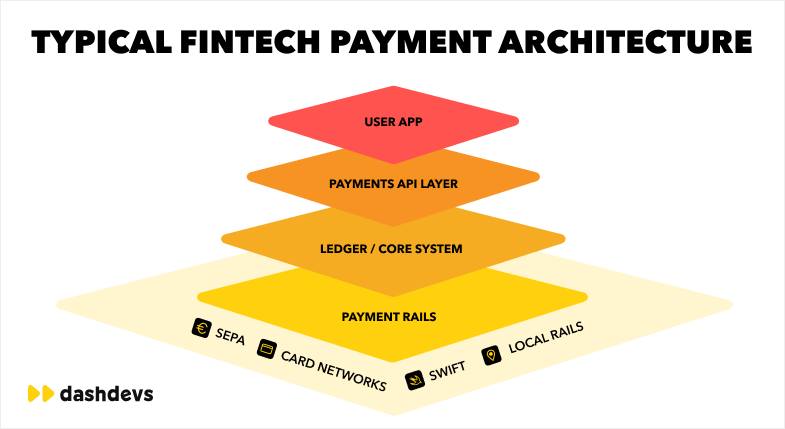

Here is the cleaner way to explain it. A modern fintech product usually has:

- customer-facing applications

- a backend or orchestration layer

- a ledger and balance engine

- compliance and monitoring services

- payment and banking integrations

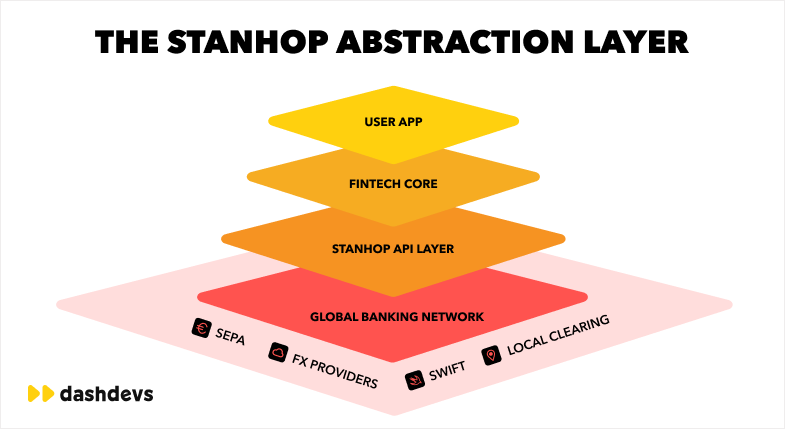

Stanhop sits in the banking connectivity layer.

****

That architecture is especially effective when paired with a modular internal platform rather than a pile of one-off integrations.

This is exactly why DashDevs built Fintech Core: to give teams a composable orchestration layer for wallets, ledgers, compliance, payments, and integrations without forcing them into a rigid monolith.

How We Would Position This in a DashDevs Build

The most useful way to embed your expertise here is not to force a sales paragraph. It is to show how infrastructure decisions actually work in delivery.

At DashDevs, we typically see three recurring scenarios:

1. A fintech needs to launch fast

The team has product-market timing pressure and cannot wait for direct banking relationships in every market.

2. A platform has rails, but no orchestration

Payments work, but routing, reconciliation, failover, and treasury visibility are weak.

3. A company wants optionality

They do not want to hard-code their entire business into one provider forever.

That is why we usually recommend a modular architecture:

- keep the ledger, wallet, and product logic under your control

- connect providers like Stanhop through an orchestration layer

- design the system so providers can evolve without rewriting the whole stack

That approach is also reflected in our work on payment orchestration, our BNPL payment orchestration case study, and our KYC services for onboarding and compliance infrastructure.

Who Usually Benefits Most from This Setup

Providers like Stanhop are especially useful for teams that need regulated payment capability without becoming a bank.

Typical fit:

- neobanks and EMI-style products

- B2B payment platforms

- marketplace payout systems

- international payroll tools

- digital wallets

- treasury and FX products

- crypto platforms that need fiat rails

For crypto and digital asset products, this becomes even more important because the product often needs both blockchain logic and traditional banking rails in the same operating model. That is very similar to the architecture patterns DashDevs uses in hybrid wallet, custody-adjacent, and fiat-to-crypto platform builds.

Build vs. Integrate: The Founder-Level Decision

This is the section business readers care about most.

Build direct if:

- payments are your core proprietary advantage

- you have time for longer rollout cycles

- you need custom control over scheme relationships

- your compliance and operations teams are already mature

Integrate a provider if:

- speed to market matters

- you need working rails sooner, not later

- you want to reduce complexity in release one

- your team should focus on product and distribution first

The answer is often not binary.

A smart architecture usually means:

- integrate first

- orchestrate well

- keep core product logic modular

- avoid unnecessary lock-in later

That is the same principle behind DashDevs’ “buy now, build later” view of fintech infrastructure, which we discuss across our content and product strategy work. You can see the logic behind that approach in our fintech app development guide and Fintech Core materials.

Security and Compliance Still Matter Either Way

Using an infrastructure provider does not remove compliance responsibility. It changes how responsibility is distributed.

If your product moves money, you still need to think carefully about:

- customer onboarding and KYC

- sanctions and AML controls

- transaction monitoring

- reconciliation and auditability

- account safeguarding logic

- incident and exception handling

This is where product teams often make a strategic mistake: they compare vendors by API features, but not by operating model.

The better question is: How much regulated complexity are we taking on ourselves, and how much are we intentionally abstracting?

That is why infrastructure planning should involve not only engineering, but also compliance, operations, finance, and product leadership.

Timeline: Building Payment Rails vs Integrating Infrastructure

One of the most underestimated challenges in fintech product development is the time required to connect to payment rails. Founders often assume that once a frontend application and backend ledger are ready, payments can be enabled quickly. In reality, the infrastructure behind global money movement involves a long sequence of regulatory, operational, and technical steps.

To connect directly to payment schemes such as SEPA or SWIFT, companies typically need to establish banking partnerships, undergo compliance onboarding, configure treasury and settlement processes, and integrate operational monitoring systems. Each of these steps requires coordination between product teams, compliance officers, and banking partners.

The timeline can grow even longer when fintech companies operate across multiple jurisdictions or plan to support multi-currency payments.

Below is a simplified comparison between building payment infrastructure internally and integrating a provider like Stanhope Financial.

| Infrastructure Step | Build Directly | Integrate Infrastructure Provider |

| Banking partnerships | 6–12 months | Already established |

| Scheme connectivity (SEPA/SWIFT) | 3–6 months | Included |

| Compliance infrastructure | 4–8 months | Integrated |

| FX and treasury setup | 3–6 months | Available |

| Total launch timeline | 12–24 months | 2–4 months |

This difference in launch timelines is one of the main reasons fintech companies rely on infrastructure providers. Instead of spending years establishing direct scheme access, teams can begin building their product experience immediately while leveraging existing banking connectivity.

For fintech startups competing in fast-moving markets, reducing infrastructure timelines often determines whether a product launches successfully or misses its market window.

If you want to understand the broader architecture behind these systems, our guide on how fintech backend infrastructure works explains the layers required to launch financial products.

Example: Cross-Border Payment Flow in a Fintech Platform

Understanding how payment infrastructure works becomes easier when looking at a real payment flow.

Imagine a fintech platform offering international payouts for businesses. A company using the platform wants to send funds to a supplier located in another country. Behind the scenes, several systems coordinate to process this transaction securely and compliantly.

The simplified payment flow looks like this:

- A user initiates a payment inside the fintech application.

- The fintech backend verifies the request and checks compliance requirements.

- The platform ledger records the transaction and updates internal balances.

- The payment orchestration layer routes the transaction through Stanhope Financial.

- The payment is sent via the appropriate rail, such as SEPA or SWIFT.

- The receiving bank processes the transfer and credits the recipient account.

Architecture example:

User Application ↓ Fintech Backend ↓ Payments Orchestration Layer ↓ Stanhope Financial Infrastructure ↓ SEPA / SWIFT Network ↓ Recipient Bank

Each of these layers plays a different role. The frontend application handles the user experience, while the backend systems manage transaction logic and compliance checks. Payment infrastructure providers such as Stanhope Financial handle the connection to global banking networks.

At DashDevs, we typically recommend introducing a dedicated orchestration layer between the application and the banking infrastructure. This approach allows fintech companies to manage routing, retries, failover logic, and payment analytics more effectively while keeping the architecture flexible for future integrations.

If you want to explore how payment routing improves reliability and conversion rates, read our detailed guide on payment orchestration and payment routing strategies.

Cost of Building Payment Infrastructure

Payment infrastructure is not only complex from a technical perspective. It is also expensive to build and maintain internally.

Launching a fintech product that supports international payments requires investment in several infrastructure components, many of which must operate continuously and meet strict regulatory requirements.

Below are typical cost areas fintech companies encounter when building payment infrastructure internally.

| Infrastructure Component | Typical Investment |

| Compliance systems (AML, monitoring) | $200k–$500k |

| Banking integrations | $100k–$300k |

| Payment scheme membership | varies by region |

| Treasury and FX infrastructure | $100k+ |

| Monitoring and reconciliation systems | $50k–$150k |

These estimates do not include ongoing operational costs such as compliance teams, payment operations staff, and incident response support.

Infrastructure providers significantly reduce these upfront costs by consolidating banking integrations, scheme connectivity, and treasury services into a single platform.

Instead of building multiple integrations with different banks, fintech companies can connect to a single infrastructure layer that already aggregates financial services from multiple providers.

Companies planning such systems should also consider the role of a core financial ledger, which acts as the backbone of transaction processing. Our article explaining core banking architecture and ledger infrastructure explores how modern fintech platforms manage balances and transactions internally.

Common Mistakes Fintech Teams Make When Launching Payments

Launching a fintech product with payment capabilities involves many decisions that affect scalability and operational reliability. Over the years, several common mistakes appear repeatedly in fintech infrastructure projects.

Understanding these pitfalls early can save teams months of development time and significant operational risk.

Underestimating compliance complexity

Payments are heavily regulated. Anti-money laundering rules, transaction monitoring requirements, sanctions screening, and customer identity verification must all be implemented correctly before transactions can be processed.

Many teams focus on product features first and only address compliance infrastructure later, which often delays product launches.

Connecting directly to too many banking partners

Some fintech startups attempt to build relationships with multiple banks simultaneously to increase payment coverage.

While diversification can be useful, managing several banking integrations dramatically increases operational complexity. Infrastructure providers often simplify this problem by aggregating multiple banking partners behind a single integration layer.

Ignoring treasury and liquidity management

Payment infrastructure does not only move money. It must also manage liquidity across currencies and jurisdictions.

Without proper treasury planning, fintech companies may experience settlement delays, unexpected FX costs, or operational inefficiencies.

Building payment routing too late

Payment routing determines how transactions are processed across different rails and providers. Designing routing logic early allows fintech platforms to optimize transaction costs, increase reliability, and support future payment methods.

“Payments infrastructure decisions made early in a product lifecycle often determine how easily that platform scales globally.”

Planning payment architecture early allows fintech companies to build flexible systems capable of supporting new rails, providers, and regulatory requirements as the business grows.

Key Takeaways

Launching a fintech product that moves money across borders requires far more than a clean user interface. Behind every transfer sits a complex infrastructure of banking rails, compliance systems, treasury operations, and payment routing logic. Building that infrastructure from scratch can take years and demand significant engineering and regulatory expertise.

Platforms like Stanhope Financial simplify this challenge by providing fintech companies with access to global payment rails such as SEPA and SWIFT, along with multi-currency accounts, virtual IBAN structures, and FX capabilities. By integrating an infrastructure layer instead of building every connection internally, fintech teams can dramatically reduce time to market while maintaining the flexibility needed to scale internationally.

However, successful fintech products still require thoughtful architecture around these integrations. Payment orchestration, ledger systems, compliance controls, and treasury management must all work together to ensure reliability and regulatory readiness as transaction volumes grow.

DashDevs helps fintech companies design scalable payment architectures and integrate infrastructure providers like Stanhope Financial using Fintech Core. From wallet systems and payment orchestration to compliance integrations and treasury management, our team supports the full lifecycle of modern fintech platforms.

Talk to our fintech experts and start building your payment infrastructure today.

Share article