Top 10 Banking Software Development Companies to Compare in 2026

February 17, 2026

Picking banking software development companies used to be a “build a mobile app and connect an API” decision. In 2026, it’s closer to assembling a regulated machine: licensing constraints, audit trails, transaction monitoring, provider dependencies, and a stack that has to evolve without breaking production.

That’s why the right banking software development company is rarely “the cheapest dev shop” — it’s the team that can design for regulation, orchestrate multiple vendors, and get you to a first compliant release in months, not years.

If you want more context on what’s changing in digital banking right now, DashDevs’ breakdown of 2026 banking shifts is a solid starting point. And if you’re planning timelines, this reality check on delivery duration will save you from fantasy roadmaps.

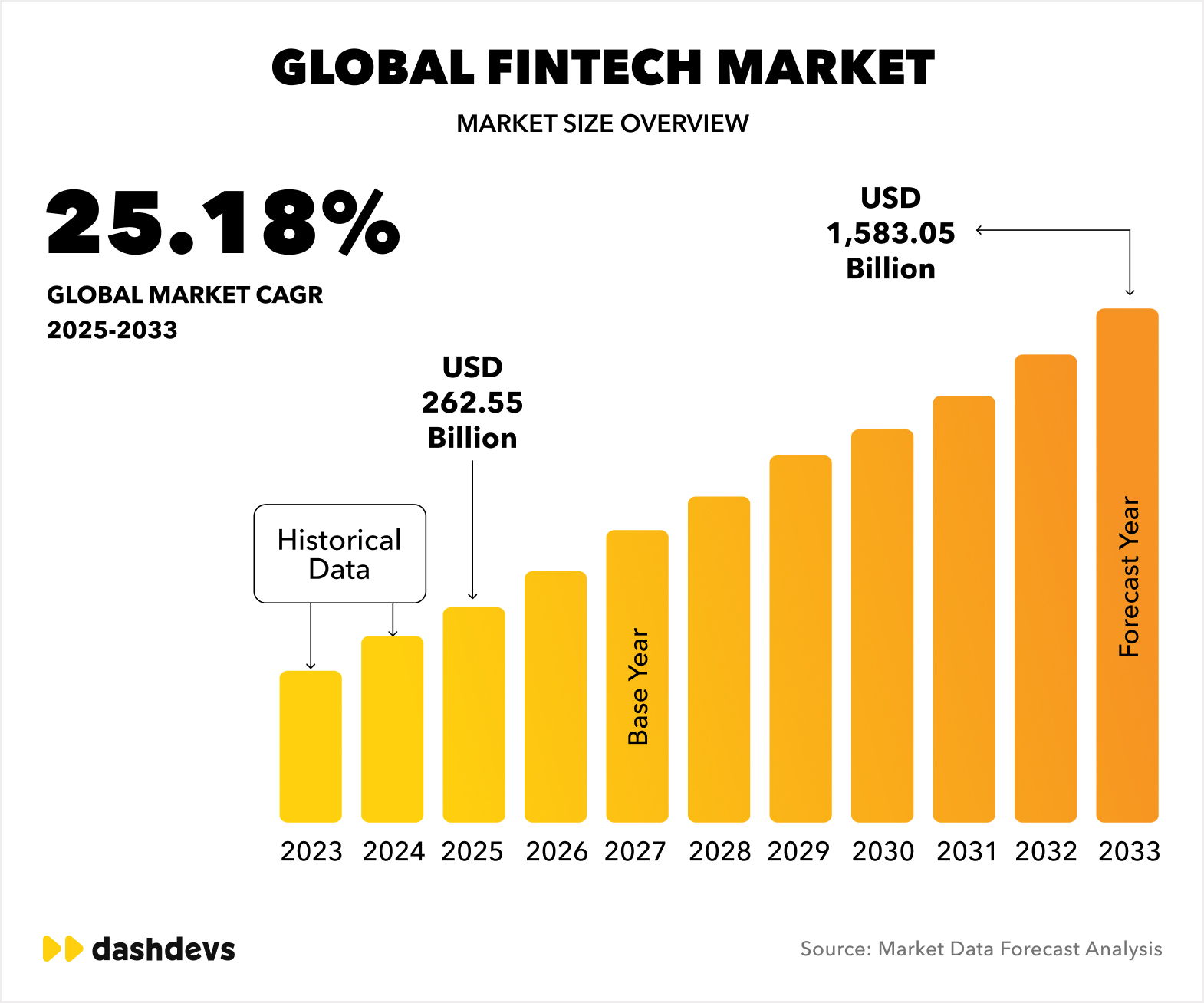

Market Overview: Fintech Is Now An Infrastructure Race

The fintech and digital banking market has moved from “launch fast” to “launch compliant, composable, and scalable.” Teams are increasingly mixing BaaS providers, payment processors, KYC vendors, and internal components into modular stacks instead of betting everything on a single platform.

That composable shift is becoming the default. Accenture’s 2026 banking trends report highlights composable architectures built from modular components as a key direction for banks.

At the same time, AI is changing how software gets built: Deloitte predicts AI tools could reduce banking software investment by 20%–40% by 2028 by boosting productivity across the SDLC.

The result: demand is growing for financial software development companies that can do the hard part — not just “build features,” but orchestrate ecosystems (BaaS + PSP + KYC + ledger), ship a regulated MVP, and keep the architecture flexible so you don’t get trapped in Vendor Lock-in 2.0.

If you’re mapping the platform landscape, this core-banking overview helps frame where platforms fit — and where engineering ownership still matters. And if you’re choosing BaaS vendors, use a checklist by our experts (seriously).

How We Ranked These Banking Software Development Companies List

There’s no shortage of banking software development companies claiming fintech expertise. But in 2026, glossy portfolios and long service lists aren’t enough. What matters is whether a partner can actually ship a regulated financial product — on time, compliant, and architected for scale.

Instead of ranking vendors by size, revenue, or brand recognition, we evaluated them through a practical delivery lens. The focus was simple: can this team design, build, and launch regulated fintech infrastructure under real-world constraints?

Because modern banking software development isn’t about building an app interface — it’s about building the system behind it.

Our Delivery-Focused Evaluation Criteria

Here’s what we looked at when assessing each banking software development company:

| Criterion | Why It Matters |

| Regulated fintech experience (EMI, PSP, VASP, banking) | Real regulatory exposure reduces launch risk. |

| MVP delivery in < 6 months | Speed-to-market is critical for licensing, fundraising, and validation. |

| Core banking & ledger expertise | The ledger is the backbone of any financial product. |

| Payments orchestration depth | Modern fintech stacks require multi-provider integration. |

| Compliance-by-design (KYC/AML, monitoring, auditability) | Compliance must be embedded, not added later. |

| BaaS & vendor ecosystem experience | Fintech today is composable and integration-heavy. |

| Architecture flexibility (no lock-in) | The ability to swap vendors protects long-term strategy. |

| Production case studies | Live systems matter more than prototypes. |

| Post-launch scaling & ops support | Stability after launch defines real success. |

| Product + engineering in one team | Strategy and architecture must work together. |

Why This Approach Matters

The market has shifted from “build vs buy” to build vs buy vs compose. Most fintech products now combine BaaS providers, payment processors, onboarding vendors, fraud systems, and internal ledgers into modular stacks.

That complexity is why companies increasingly choose specialized financial software development companies that understand orchestration, compliance, and composable architecture — not just code delivery.

In short, we ranked partners based on their ability to:

- Launch regulated MVPs quickly

- Design flexible fintech infrastructure

- Orchestrate multi-vendor ecosystems

- Support scaling beyond launch

Because when evaluating top banking software companies, delivery credibility beats marketing every time.

#1 Dashdevs — Fintech & Digital Banking Engineering Partner

DashDevs is #1 on this list because they match the 2026 reality: regulated delivery, composable architecture, and vendor orchestration — not just “software development services.”

Where DashDevs stands out for teams evaluating banking software development companies:

- Regulated fintech specialization: delivery in digital banking, payments infrastructure, open banking, onboarding/KYC layers, and compliance automation.

- Composable fintech stack execution: building modular stacks across providers instead of forcing single-vendor platforms (ledger + payments + onboarding + monitoring).

- Productized backbone: Fintech Core: a white-label modular foundation designed to accelerate compliant launches while staying flexible (use what you need, replace what you don’t).

- Launch mindset: real production outcomes and scale support — not PoCs that die after a demo.

If you’re trying to plan time-to-market, start here (it sets expectations properly). Teams often underestimate how long regulated fintech delivery actually takes — and where the “hidden delays” come from (vendors, compliance, audit trails, certification). DashDevs packaged real patterns into a short guide: Buy Now, Build Later — a guide to faster fintech launches.

The Engineering Teams Behind Modern Fintech

Before diving into names, it’s important to clarify what this shortlist represents.

These are not core banking platforms, BaaS providers, or low-code fintech tools. They are engineering and product partners. That distinction matters. Platforms sell software licenses. Engineering partners design the architecture, orchestrate vendors, build the system, and share responsibility for delivery outcomes with your team.

If you’re evaluating banking software development companies, this difference changes everything. One gives you tools. The other helps you assemble and launch a regulated financial product.

Below is how the shortlisted companies typically position in the market.

Tier 1: Global Engineering Partners with Fintech Depth

This group includes large, globally recognized financial software development companies that operate at enterprise scale.

They are best suited for:

- Large banks

- Regulated financial institutions

- Multi-country transformation programs

- Long-term modernization initiatives

Their strengths typically include:

- Deep enterprise architecture expertise

- Large distributed delivery teams

- Experience with complex regulatory environments

- Structured governance and compliance-heavy programs

However, that scale comes with tradeoffs. MVP cycles can be slower, processes heavier, and budgets significantly higher compared to more specialized fintech-focused teams.

Companies in this tier: EPAM, Thoughtworks, Endava, Grid Dynamics

These firms are strong choices for institutions prioritizing enterprise transformation over rapid product experimentation.

Tier 2: Fintech-Focused Engineering Boutiques

This tier consists of more specialized banking software development companies with strong fintech domain focus.

They are typically best for:

- Fintech startups

- Digital banks

- Embedded finance teams

- Platform builders launching new regulated products

Their strengths usually include:

- Deep fintech domain expertise

- Faster MVP cycles

- Modular, composable architecture design

- Strong vendor orchestration experience

Because they operate with more focused teams, they may have smaller overall scale compared to Tier 1 providers. Capacity can be more selective, especially for very large enterprise programs.

Companies in this tier: GFT Technologies, SoftServe (Fintech Unit), Luxoft (Fintech & Banking Practice), 10Clouds

For teams looking to launch or scale regulated fintech products quickly, this group often strikes a balance between speed and domain expertise.

Tier 3: Regional Fintech Specialists & Verticalized Global Players

The third tier includes financial services software development companies that either focus strongly on specific regions or operate large global organizations with verticalized fintech practices.

They are generally best suited for:

- Mid-market banks

- Fintech scale-ups

- Regional market launches

- Cost-sensitive transformation programs

Typical strengths include:

- Competitive delivery rates

- Strong regional compliance familiarity

- Reliable engineering capacity

- Multi-industry experience

The tradeoff is that these firms may be more services-led than product-led. Fintech-specific productization and reusable architecture patterns can vary by team.

Companies in this tier: DataArt, Cognizant (Fintech Vertical)

Competitor Profiles: Quick Buyer-Oriented Notes

Below is a practical breakdown of each shortlisted player. This isn’t a feature comparison — it’s a decision-making lens to help you understand where each firm typically fits, and how they differ from fintech-native banking software development companies focused on regulated speed.

EPAM

Best for: Large enterprises modernizing core banking systems or running multi-year transformation programs across regions.

EPAM is known for enterprise-scale delivery, strong governance frameworks, and deep engineering capability. They are particularly effective in complex modernization initiatives involving legacy systems and global rollout coordination.

Tradeoff: Heavyweight processes and enterprise governance structures can slow MVP cycles and early-stage product validation.

Difference vs. DashDevs: EPAM is built for enterprise transformation at scale. DashDevs is optimized for fintech speed, composable stacks, and launching regulated products in months rather than years.

Thoughtworks

Best for: Organizations undergoing deep digital transformation with strong product culture and agile adoption goals.

Thoughtworks brings strong methodology, transformation strategy, and agile coaching. They excel at helping organizations rethink delivery processes and modern engineering culture.

Tradeoff: Fintech infrastructure and regulated financial systems are not their core specialization.

Difference vs. DashDevs: Thoughtworks brings transformation expertise. DashDevs brings hands-on fintech architecture, ledger design, payments orchestration, and regulated delivery experience.

Endava

Best for: Banks and financial institutions seeking delivery capacity across multiple geographies.

Endava supports enterprise-scale programs and cross-border delivery models, often working with established financial institutions.

Tradeoff: Broader industry focus can dilute fintech platform specialization.

Difference vs. DashDevs: Endava is strong in scaling enterprise programs. DashDevs focuses on composable fintech stacks and faster regulated launches.

Grid Dynamics

Best for: Data-driven financial platforms and institutions building analytics-heavy systems.

Grid Dynamics has strong platform engineering and data architecture capabilities, particularly in analytics and performance optimization.

Tradeoff: More focused on data and platform engineering than full end-to-end fintech product delivery.

Difference vs. DashDevs: Grid Dynamics excels in deep platform and data work. DashDevs combines product strategy, core/ledger architecture, and regulated fintech delivery under one roof.

GFT Technologies

Best for: Financial institutions modernizing digital banking and payments infrastructure.

GFT has strong experience in enterprise financial services environments and modernization initiatives.

Tradeoff: More execution-led than productized fintech-stack-led.

Difference vs. DashDevs: GFT supports enterprise-level delivery. DashDevs adds fintech-native reusable building blocks through Fintech Core and a stronger focus on rapid, regulated product launches.

SoftServe (Fintech Unit)

Best for: Banks and fintechs running cloud migration or modernization programs.

SoftServe offers scale, engineering capacity, and cross-industry experience with a fintech vertical.

Tradeoff: Fintech depth can vary depending on the assigned team and business unit.

Difference vs. DashDevs: SoftServe brings enterprise scale. DashDevs is purpose-built for regulated fintech delivery and composable architecture design.

Luxoft (Fintech & Banking Practice)

Best for: Complex enterprise banking transformations and legacy modernization initiatives.

Luxoft works extensively with large financial institutions and legacy-heavy systems.

Tradeoff: Enterprise-first delivery models may slow early experimentation and MVP validation.

Difference vs. DashDevs: Luxoft modernizes at enterprise scale. DashDevs helps launch and scale new fintech products faster using modular stacks.

10Clouds

Best for: Fintech startups and early-stage product teams needing rapid MVP execution.

10Clouds is well suited for experimentation, web3-related initiatives, and product prototyping.

Tradeoff: Smaller scale for complex, multi-market regulated banking programs.

Difference vs. DashDevs: 10Clouds is strong in early experimentation. DashDevs covers the full path from regulated MVP to production fintech infrastructure.

DataArt

Best for: Mid-market banks and fintechs seeking reliable engineering delivery across regions.

DataArt offers strong engineering teams and broad industry exposure.

Tradeoff: Less fintech-specific productization compared to more specialized teams.

Difference vs. DashDevs: DataArt delivers solid engineering execution. DashDevs brings deeper fintech domain specialization and reusable architecture patterns tailored for regulated environments.

Cognizant (Fintech Vertical)

Best for: Large financial institutions running global digital transformation programs.

Cognizant operates at enterprise scale with extensive cross-industry capabilities.

Tradeoff: Enterprise complexity and governance layers can slow innovation cycles and MVP speed.

Difference vs. DashDevs: Cognizant is built for global enterprise programs. DashDevs is optimized for faster fintech product launches with composable, regulation-ready architectures.

Global engineering partners excel at scale and enterprise modernization. But fintech-native teams increasingly choose specialized banking software development companies that combine regulated delivery experience, composable architecture, and MVP speed.

That’s the gap DashDevs is designed to fill: bridging product strategy, compliance-by-design, and modular fintech engineering to help teams launch and scale regulated financial products faster.

How to Choose a Banking Software Development Partner in 2026

Choosing between banking software development companies in 2026 is not about comparing hourly rates or tech stacks. It’s about understanding who can actually deliver a regulated financial product without delays, rewrites, or vendor lock-in.

The market has shifted. Most fintech builds today involve BaaS providers, payment processors, KYC/KYB tools, fraud systems, card issuers, and internal ledger layers. The complexity is no longer development — it’s orchestration and compliance.

Here’s how to evaluate a banking software development company properly.

#1 Validate Regulated Case Studies

Ask for proof of live regulated systems — not just prototypes or mobile apps.

Look for:

- EMI / PSP / banking-related delivery

- Real transaction processing environments

- Audit exposure

- Compliance workflows embedded into architecture

A strong financial services software development company should be comfortable discussing licensing constraints, reporting requirements, and transaction monitoring logic — not just UI decisions.

#2 Ask About Delivery Timelines & Milestones

Speed matters — but realistic speed.

Instead of asking, “How fast can you build an app?”, ask:

- How long to first compliant release?

- What does the MVP include?

- What dependencies can delay launch?

If you want a grounded view on timelines, this breakdown helps reset expectations.

#3 Check BaaS + PSP + KYC Integration Experience

Modern fintech is ecosystem-driven. Very few teams build everything from scratch anymore.

A qualified banking software development company should have real integration experience with:

- BaaS providers

- Payment processors

- Card issuing platforms

- KYC/KYB vendors

- AML & fraud tools

If they can’t clearly explain how orchestration layers work across vendors, that’s a red flag.

For vendor complexity awareness, use this checklist approach.

#4 Assess Architecture Flexibility

Ask directly:

- Can we replace a payment provider without rewriting the system?

- Is the ledger decoupled from experience layers?

- Are integrations abstracted or tightly coupled?

The best financial software development companies design modular systems that allow you to swap components without starting over.

Vendor lock-in is rarely obvious at the beginning — but extremely expensive later.

#5 Look for Post-MVP Scaling Experience

Launching is step one. Surviving growth is step two.

You want a partner that understands:

- Transaction scaling

- Monitoring & observability

- Incident response

- Reconciliation at scale

- Performance optimization

Many teams can ship an MVP. Fewer can support 10x growth without instability.

#6 Ensure Product + Compliance Thinking Is Embedded

A pure engineering vendor may write solid code — but fintech delivery requires product logic and compliance logic working together.

Strong banking software development companies combine:

- Product discovery

- Regulatory awareness

- Architecture design

- Engineering execution

If product and compliance thinking are outsourced or bolted on later, delivery risk increases dramatically.

The Bottom Line

In 2026, choosing among banking software development companies is no longer about who can write code the fastest. It’s about who can design compliant architecture, orchestrate complex vendor ecosystems, and get you to a regulated release without locking you into fragile infrastructure.

The market has moved from “build an app” to build a financial system. That means ledger integrity, auditability, modular architecture, BaaS orchestration, and post-launch scalability are no longer optional — they’re baseline requirements.

Global engineering firms bring scale. Platforms bring tools. But if your goal is to launch and scale a regulated fintech product with speed and architectural flexibility, you need a partner that combines:

- Product strategy

- Compliance-by-design

- Core banking & ledger expertise

- Payments orchestration depth

- Real production delivery experience

That’s exactly what DashDevs was built for.

Ready to discuss your fintech build? If you’re evaluating banking software development companies and want a practical conversation about timelines, licensing constraints, architecture decisions, and vendor strategy — let’s talk.

Share article