Best Core Banking Solutions and Platforms for Modern Financial Products

May 22, 2026

Summary

In this guide we cover:

- how core banking solutions differ by provider type — enterprise cores, composable SaaS, modular fintech infrastructure

- best-fit provider categories for neobank launch, legacy migration, embedded accounts, and lending stacks

- legacy vs modern core banking architecture and what implementation success actually requires

- top 10 core banking solutions and providers compared for 2026 — with operational fit notes, not generic rankings

- how to choose a core banking platform by functionality, integration cost, regulatory fit, and scalability

Most fintech founders and banking innovation teams evaluating core banking solutions start with the same question: buy a licensed core, compose modular APIs, or partner through BaaS? The answer depends on product type, regulatory scope, and how fast you need to ship — not on vendor brand recognition alone.

In finance, the stack often centers on a core banking solution: the banking software that runs accounts, ledgering, and payments processing behind a digital bank, wallet, or embedded finance flow. Teams comparing core banking providers are usually deciding how much of the banking core to own versus orchestrate.

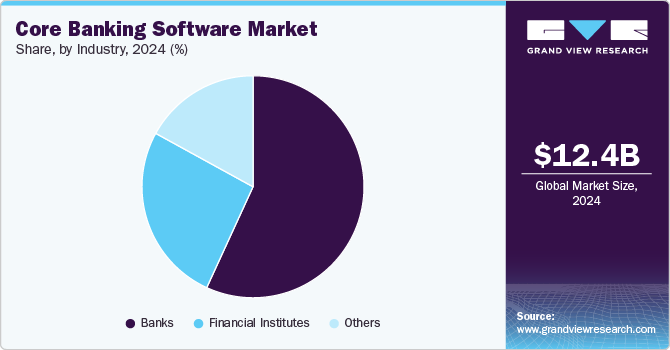

The global core banking software market reached approximately USD 13.8 billion in 2025, with forecasts pointing to USD 21.6 billion by 2030 at roughly 10.2% CAGR. Growth is driven by modernization programs at financial institutions, real-time payment expectations, and demand for cloud-based, API-first core banking platforms.

Best-Fit Guide: Core Banking Platforms by Business Need

Use this table before reading individual vendor profiles. It maps common product goals to provider categories — not a single “winner.”

| Business need | Best-fit provider type | Typical examples | Time-to-market signal |

|---|---|---|---|

| Launch a neobank or wallet fast | Modular fintech infrastructure + BaaS | Fintech Core, Mambu + sponsor bank | Weeks to months |

| Replace legacy core at a tier-1 bank | Enterprise core banking system | Temenos, Finacle, FIS, Oracle FLEXCUBE | Multi-year program |

| Build lending or deposits on APIs | Composable SaaS core | Mambu, Thought Machine | Months with clear scope |

| Open banking / middleware modernization | Open API banking stack | Finastra, Finacle | Depends on legacy depth |

| US community bank or credit union | Regional core + payments bundle | Fiserv, FIS | Quarters |

| Global SI-led transformation | Services-heavy core platform | TCS BaNCS, Finacle | Program-led delivery |

| Embedded finance inside non-bank app | BaaS + orchestration layer, not full core | See top BaaS companies | Fastest when partner bank holds license |

Quote-worthy rule: The right core banking platform is the one your team can integrate, reconcile, and operate — not the one with the longest feature checklist.

Legacy Core vs Modern Core Banking: Architecture Comparison

| Dimension | Legacy core banking system | Modern digital core banking platform |

|---|---|---|

| Deployment | On-prem or managed private cloud | Cloud-native, API-first |

| Product changes | Core change requests, long cycles | Configurable products via APIs |

| Integration | Batch files, point integrations | Event-driven, webhook-ready |

| Ledger model | Often monolithic | Modular or smart-contract-based |

| Best for | Stable incumbents with IT capacity | Neobanks, greenfield digital banks |

| Risk profile | Migration complexity | Vendor maturity and regulatory fit |

Understanding this split helps CTOs avoid forcing a neobank roadmap onto an enterprise core — or vice versa.

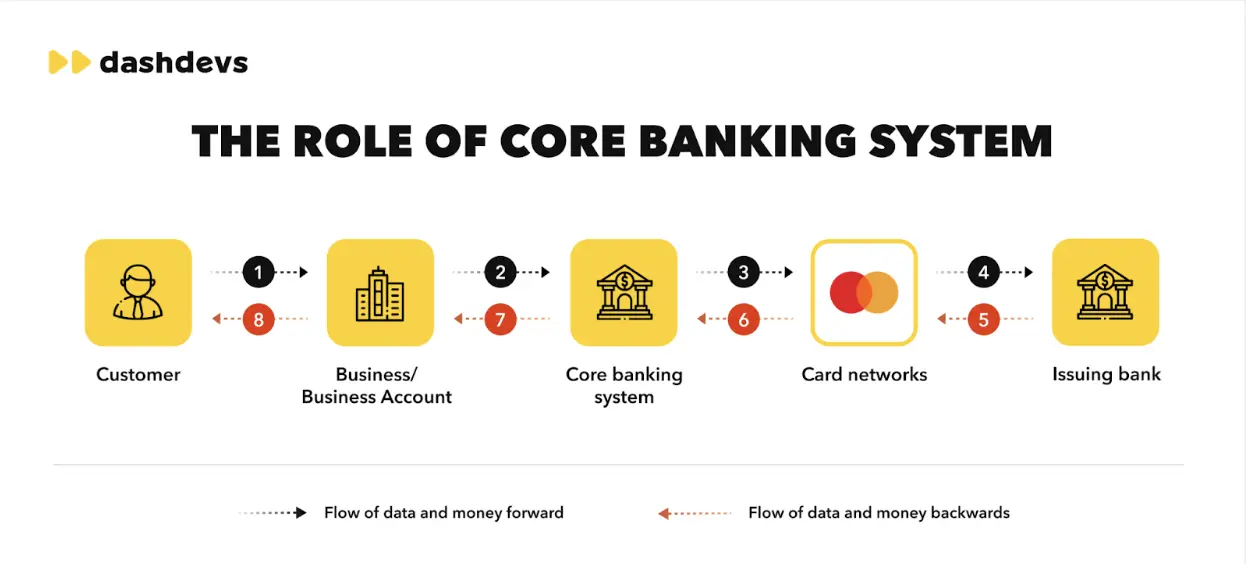

Core Banking Software: Explained

Core banking software is an integrated technology platform that manages and automates essential banking operations — onboarding, accounts, payments processing, general ledger, and reporting.

So what are core banking solutions in practice? They are licensed-grade banking software solutions — often delivered as cloud-based SaaS — that combine ledger, accounts, payment rails, and compliance workflows so product teams do not recreate banking infrastructure from scratch. What fits your roadmap may differ from another team’s: incumbents replace legacy core banking systems, while fintechs often assemble a digital core banking platform from APIs and modules.

Think of core banking software as a B2B structure that integrates with your application and handles the back end of banking services for end customers. A well-designed multi-account ledger system sits at the center — without reliable ledger logic, mobile banking UX cannot scale.

For banking software for banks and fintech builders alike, the same modules recur: KYC/AML, account management, transaction processing, FX, card issuing integration, general ledger, reporting, and an integration hub. Integrated banking solutions only work when those modules share one source of truth for balances and settlement.

Top 10 Core Banking Solutions and Products in 2026

The vendors below are leading core banking software providers and core banking platforms — useful whether you are modernizing a bank core, launching a neobank with a dedicated neobank app development company, or embedding accounts via BaaS. Rankings reflect breadth, reliability, and integration fit — not a single score.

Important note: Module composition varies by vendor. Analytics, international rails, or retail coverage may be add-ons. Payment processors and gateways often plug into core banking systems as native or third-party modules — see our guide on payment processors and payment gateways.

Each profile below includes best fit, differentiator, and implementation note so comparisons feel operational — not interchangeable.

1. Fintech Core (DashDevs)

Provider type: Modular fintech infrastructure (not a standalone licensed bank core)

Best for: Digital wallets, super-apps, crypto-fiat hybrids, and teams that validated product-market fit and now need speed.

Fintech Core is modular fintech white label software with pre-connected modules — designed for companies that cannot afford 12–18 month integration cycles before launch.

Differentiator: Productized architecture with fiat + crypto modules, partner ecosystem, and configurable UI layers — closer to launch-ready software banking solutions than a blank core license.

Implementation note: Works best when you need orchestration across PSPs, wallets, and compliance vendors — not when you must operate as a standalone licensed bank without partners.

Key modules:

- Real-time multi-currency transaction processing

- Pre-integrated fiat and crypto partner ecosystem

- Digital wallet and optional card expansion paths

- Risk, compliance, and KYC integrations

- Cloud-based, modular expansion for liquidity and cards

2. Mambu

Provider type: Composable SaaS core banking platform

Best for: Digital-first banks, lenders, and product factories that configure loans and deposits via APIs rather than core rewrites.

Mambu (founded 2011, Berlin) popularized the “composable banking” model — banks assemble products from configurable building blocks instead of customizing monolithic code.

Differentiator: Fast product configuration for lending and deposit products; strong fit for greenfield digital bank brands in multiple regions.

Implementation note: You still need clear ledger and compliance ownership — Mambu accelerates product layers but does not replace sponsor-bank or licensing strategy.

Key strengths: API-driven architecture, cloud-native scaling, modular onboarding, integrated payments.

3. Finastra

Provider type: Universal banking software with open-banking middleware strength

Best for: Incumbents modernizing retail/corporate stacks and institutions investing in open banking connectivity.

Formed in 2017 (Misys + D+H merger), Finastra spans core, payments, and fusion middleware — often selected when banks need both legacy coexistence and API exposure.

Differentiator: Broadest open API ecosystem among incumbents; strong when transformation means connecting old and new cores — not only greenfield launch.

Implementation note: Programs are integration-heavy; scope data migration and parallel run early. Finastra shines in multi-product financial institutions, not minimal MVP wallets.

Key strengths: Multi-currency processing, risk/compliance modules, universal banking coverage, legacy digital transformation tooling.

4. Finacle

Provider type: Enterprise core from Infosys (EdgeVerve)

Best for: Tier-1 and regional banks pursuing large-scale core banking system replacement with SI support.

Finacle serves 100+ countries with deep retail, corporate, and universal banking coverage — often chosen when the buyer already runs on Infosys services.

Differentiator: Global model-bank templates and analytics layer; strong in Asia, Middle East, and Africa modernization programs.

Implementation note: Expect program governance, data cleansing, and multi-year milestones — not startup-style weekly releases.

Key strengths: Omnichannel experience, AI/analytics add-ons, extensive API catalog, multi-currency real-time processing.

5. FIS

Provider type: Global financial technology conglomerate with core + payments

Best for: Large banks and processors needing breadth across retail, commercial, wealth, and payments in one vendor relationship.

FIS (founded 1968) combines core processing with adjacent payments and banking technology — appealing when procurement prefers fewer vendor contracts.

Differentiator: End-to-end banking IT solutions under one roof; strong US and global enterprise footprint.

Implementation note: Breadth can mean complexity — define which FIS products you actually need (core vs payments vs digital) before contract scope inflates.

Key strengths: Cloud-enabled core, omnichannel retail/commercial, integrated risk tools, analytics and AI add-ons.

6. Temenos

Provider type: Established enterprise core for 3,000+ financial institutions

Best for: Banks and community banks seeking proven modern core banking with model bank accelerators.

Temenos (Geneva, 1993) remains one of the most deployed core banking software vendors worldwide — known for Transact and rich functional coverage.

Differentiator: Depth of pre-built banking products (deposits, lending, wealth) with cloud-native and cloud-agnostic deployment options.

Implementation note: Modular licensing helps, but functional breadth requires disciplined phase planning — avoid enabling every module on day one.

Key strengths: Real-time processing across verticals, analytics/personalization, extensive API framework, global regulatory templates.

7. Thought Machine

Provider type: Cloud-native core engine (Vault Core)

Best for: Banks building greenfield digital brands or replacing legacy cores with smart-contract-style product configuration.

Thought Machine (London, 2014) targets institutions that want Vault Core’s event-driven ledger and continuous delivery — not incremental wrapper APIs on old batch cores.

Differentiator: Smart contract-based product configuration and high resilience for enterprise scale; strong engineering reputation among top core banking software companies.

Implementation note: Requires mature engineering culture; benefits appear when product teams own configuration velocity — not when ops expects turnkey retail banking on week one.

Key strengths: Real-time core engine, multi-currency support, open APIs, continuous delivery model.

8. Fiserv

Provider type: US-centric core and payments bundle

Best for: US community banks, credit unions, and regional institutions prioritizing payments + core from a single banking core providers relationship.

Fiserv combines core processing with payments, digital banking, and merchant services — common in North American mid-market banking.

Differentiator: Trusted operational footprint in US community banking; strong when existing Fiserv payments relationships simplify core negotiation.

Implementation note: Less common as first choice for global neobank MVPs; evaluate cross-border and API depth against your expansion roadmap.

Key strengths: Digital banking engagement tools, cloud or on-prem deployment, compliance tooling, real-time payments integration.

9. Oracle FLEXCUBE

Provider type: Enterprise core within Oracle ecosystem

Best for: Large regional and global banks already standardized on Oracle infrastructure.

Oracle FLEXCUBE targets institutions that want deep retail/corporate coverage inside Oracle’s enterprise stack — not lightweight fintech orchestration.

Differentiator: Tight coupling with Oracle middleware, database, and analytics investments; strong for banks optimizing existing Oracle spend.

Implementation note: Best value when Oracle is already strategic; greenfield fintechs rarely need full FLEXCUBE scope.

Key strengths: Omnichannel banking, scalable regional/global deployment, compliance and risk modules, integrated mobile capabilities.

10. TCS BaNCS

Provider type: SI-led global core platform (Tata Consultancy Services)

Best for: Large transformation programs where delivery capacity matters as much as software.

TCS BaNCS supports retail, corporate, and universal banking with cloud-ready architecture — often sold alongside TCS implementation services at scale.

Differentiator: Global delivery model plus bank core system providers coverage for complex, multi-country rollouts.

Implementation note: Success depends on TCS program governance; treat as transformation partnership, not plug-and-play SaaS.

Key strengths: Multi-channel processing, cloud-ready deployment, risk/compliance integration, API-driven extensions.

Note: Providers are unordered — provider #1 is not “best.” All are top core banking providers on the global market. For build and integration support beyond vendor selection, see fintech software development services from DashDevs.

Core Banking Software Providers Compared: Vendor Snapshot

If you are comparing core banking providers side by side — whether you call them core banking software companies, core banking solution providers, or core banking software vendors — the table below summarizes footprint, pricing style, and positioning. Cloud-based SaaS dominates newer entrants; legacy stacks often still sell modular licenses.

| Vendor | HQ | Founded | Employees | Pricing model | Key strength |

| DashDevs (Fintech Core) | London, UK | 2011 | 100+ | Subscription (SaaS) | Fast time-to-market for wallets and modular fintech products |

| Mambu | Berlin, Germany | 2011 | 1,000+ | Subscription (SaaS) | Composable products for digital banking |

| Finastra | London, UK | 2017 (merger) | 10,000+ | License + subscription mix | Open banking and universal banking breadth |

| Finacle | Bangalore, India | 1999 | 2,800+ | Subscription (SaaS) + services | Global enterprise core with Infosys delivery |

| FIS | Jacksonville, FL, US | 1968 | 50,000+ | SaaS or license | Full-stack banking and payments for large FIs |

| Temenos | Geneva, Switzerland | 1993 | 4,600+ | Modular license | Model-bank depth for 3,000+ institutions |

| Thought Machine | London, UK | 2014 | 500+ | Subscription (SaaS) | Smart-contract-style product configuration |

| Fiserv | Brookfield, WI, US | 1984 | 44,000+ | SaaS or license | US community bank and payments bundle |

| Oracle FLEXCUBE | Mumbai, India | 1997 | 9,000+ | Modular license | Enterprise Oracle-stack integration |

| TCS BaNCS | Mumbai, India | 2004 | 40,000+ (TCS) | SaaS + services | SI-led global core transformation |

Operational takeaway: Pricing model signals implementation style — SaaS cores favor product teams; license + SI models favor program offices.

How to Choose a Core Banking Provider

Evaluation Criteria for Core Banking Platforms

Choosing the right core banking solution starts with use case and regulatory scope — not vendor logo recognition.

Shortlisting core banking software providers comes down to how core banking solution technology matches your geography, product, and operating model. Use the criteria below when you evaluate banking core solutions:

| Criterion | What to validate | Common pitfall |

|---|---|---|

| Functionality | Required modules: ledger, payments, cards, lending | Buying full core for MVP scope |

| Integration cost | API maturity, sandbox, documentation | Underestimating SI hours |

| Regulatory fit | Licenses, regions, reporting outputs | Demo in one country, launch in three |

| Scalability | Throughput, multi-currency, product expansion | Single-product fit only |

| Support model | B2B SLAs and escalation paths | End-user support gaps |

| Total cost | License + implementation + change requests | Low license, high customization bill |

Additional checks for banking core providers:

- Niche fit: Confirm the vendor serves your segment — neobank, corporate, community bank, or embedded finance.

- Location coverage: Verify compliance software for banks in each target market.

- Reputation: Use analyst reviews, reference calls, and production uptime — not marketing claims alone.

- Operational efficiency: Ask how releases, reconciliation, and incident response work after go-live.

DashDevs fintech consulting teams often help founders score vendors against architecture and launch timeline before contract signature.

Who Needs Core Banking Software?

Companies adopting core banking systems — or core banking software solutions that include a licensed core — usually fall into two buckets: fintech-native builders and non-bank brands embedding finance. Both need the same core banking product building blocks:

- Customer onboarding and AML/KYC

- Account management

- Transaction processing and real-time settlement

- Currency exchange

- Card issuing

- General ledger and financial accounting

- Reporting and audit trails

- Integration hub for third-party services

Fintech businesses

Typical fintech companies may lead with lending, personal finance, or payments — not full banking. Core banking products still matter when they add accounts, wallets, or card programs.

Square (Block) integrated business banking — accounts, savings, and loans — into its merchant ecosystem, reducing dependence on external processors and improving operational efficiency for sellers.

Non-fintech businesses

Non-fintech brands use core banking solution providers indirectly through BaaS. Shopify Balance gives merchants faster fund access via banking partnerships — not an in-house core build.

Uber Money provides drivers real-time earnings access, wallets, and debit products. Grab Financial Group expanded across Southeast Asia into payments, lending, and insurance through regional fintech and BaaS partners.

Shared reasons for adoption:

- New revenue streams from financial services

- Better customer experience and retention

- Faster time to market for financial features

- Scalability across markets

- Richer behavioral data for product decisions

For scaling hurdles in banking transformation, see 5 challenges of digital transformation in banking.

Final Take

As of 2026, core banking solutions remain the backbone of digital transformation — helping businesses scale, improve customer experience, and unlock revenue through embedded finance. Demand for API-driven core banking platforms and cloud deployment keeps rising, so vendor choice is a long-term architecture decision — not a one-off procurement event.

When you evaluate core banking software vendors, weigh functionality, integration effort, API maturity, regulatory coverage, scalability, and support. Whether you need a full core banking system or a lighter orchestration layer on a partner bank, alignment with your product roadmap matters more than brand recognition alone.

With 15+ years in fintech delivery and 100+ launched products, DashDevs helps teams integrate core banking solutions into regulation-compliant, investor-ready platforms — from vendor selection through production ledger design.

Share article