What Is Core Banking?

February 25, 2026

Summary

Core Banking in 60 Seconds

- The definition of core banking solution: a centralized system that processes deposits, loans, payments, and ledger entries in real time.

- A core banking solution is the operational backbone of any bank or regulated fintech.

- Modern cores are API-first, modular, and increasingly cloud-native.

- Core doesn’t equal frontend app. Core is not a payment processor. Core ≠ BaaS provider — though all three connect to it.

- Cloud based core banking systems are actively replacing monolithic legacy infrastructure across the industry.

- Architecture decisions made today define long-term scalability, regulatory flexibility, and cost structure.

Most articles define core banking as “software that allows banks to manage accounts and transactions.” That’s technically correct — and strategically useless.

If you’re launching a digital bank, upgrading legacy infrastructure, or evaluating vendors, a dictionary answer won’t help you make the decisions that will define your margins, your regulatory posture, and your product roadmap for the next decade.

The stakes are not abstract. The global core banking software market was valued at $16.79 billion in 2025 and is projected to reach $64.96 billion by 2032 at a CAGR of 18.6%, according to Fortune Business Insights. Banks and fintechs that delay core modernization aren’t just falling behind on technology. They’re falling behind on the operating model.

The urgency compounds when you look at the cost of inaction. Banks currently spend 70–78% of their IT budgets simply maintaining legacy systems — leaving almost nothing for innovation. That maintenance burden costs global banks an estimated $36.7 billion annually, a figure projected to reach $57 billion by 2028.

This guide answers the questions that actually matter: What is core banking in practice? What does modern core banking solution technology look like under the hood? How does core banking system architecture impact scalability, compliance, and unit economics? And when should you build, buy, or orchestrate?

What Is Core Banking? A Clear Definition for Business and Technical Readers

What is core banking? At its most essential, core banking refers to centralized banking infrastructure that serves as the operational record of truth for a financial institution. The core bank system enables banks and fintechs to:

- Open and manage customer accounts

- Transfer and settle funds across channels

- Process deposits and withdrawals in real time

- Issue and service loans, including repayments and amortization

- Track real-time balances with full auditability

- Execute transactions with ledger integrity

The core banking system maintains the general ledger — the master record of every financial obligation, entry, and reconciliation event. It is the source of truth that ensures a customer sees the same balance whether they log in via mobile, visit a branch, or call customer support.

Here is the core banking solution definition that matters in a product context:

A core banking solution is a centralized, real-time processing system that records and manages financial products, transactions, and customer accounts across a banking institution. It is what separates a licensed bank from a wallet app.

This definition of core banking solution draws a clear boundary: a wallet app can move money. A licensed bank, built on a proper core banking system, can hold it, lend it, and account for it with regulatory precision.

What Is a Core Banking Solution vs. a Core Banking System?

These terms appear interchangeably in vendor marketing, analyst reports, and engineering documentation. The nuances matter when you’re scoping a build, evaluating an RFP, or briefing a board.

| Term | Meaning | Example |

|---|---|---|

| Core banking | The concept of centralized banking operations | The strategic capability a licensed institution has |

| Core banking system | The actual software platform running the operations | Temenos, Mambu, Thought Machine, Finastra |

| Core banking solution | A packaged or custom implementation delivered to a specific institution | A neobank built on Mambu with a custom orchestration layer |

| Core banking solution technology | The technical stack powering the solution: architecture, APIs, cloud infrastructure | API-first, event-driven, cloud-native, modular microservices |

Understanding these distinctions allows you to ask sharper questions of vendors and engineers alike. When you ask what are core banking solutions, you’re asking about the market. When you ask what is core banking system architecture, you’re asking about infrastructure design. Both questions require different answers.

Core Banking Services — What Does a Core Actually Handle?

There is a persistent misconception in the market: that the core banking system does everything. It does not. Understanding the precise scope of core banking services is critical for architecture decisions, vendor selection, and integration planning.

Core banking services the core directly manages:

- Account lifecycle management — opening, closing, dormancy, product assignment

- General ledger — double-entry bookkeeping, reconciliation, balance integrity

- Transaction processing — credits, debits, reversals, real-time posting

- Interest calculation and accrual — daily, monthly, compound logic

- Loan origination and servicing — drawdowns, repayments, amortization schedules

- Regulatory reporting — audit trails, compliance exports, suspicious activity hooks

- Fee and limit configuration — product-level rules for charges and thresholds

What the core connects to — but does not replace:

- KYC and identity verification vendors (e.g., Veriff, Onfido)

- Card processors (e.g., Marqeta, GPS)

- Payment gateways and rails (SEPA Instant, SWIFT, Faster Payments, ISO 20022)

- CRM and customer engagement platforms

- AML and fraud detection engines

- Customer-facing mobile and web applications

A common and costly mistake: conflating the payment processor with the core bank system. They are not interchangeable. The payment processor moves money. The core records it, reconciles it, and ensures the ledger remains accurate. Confusing these two layers leads to architectural decisions that are extraordinarily expensive to reverse.

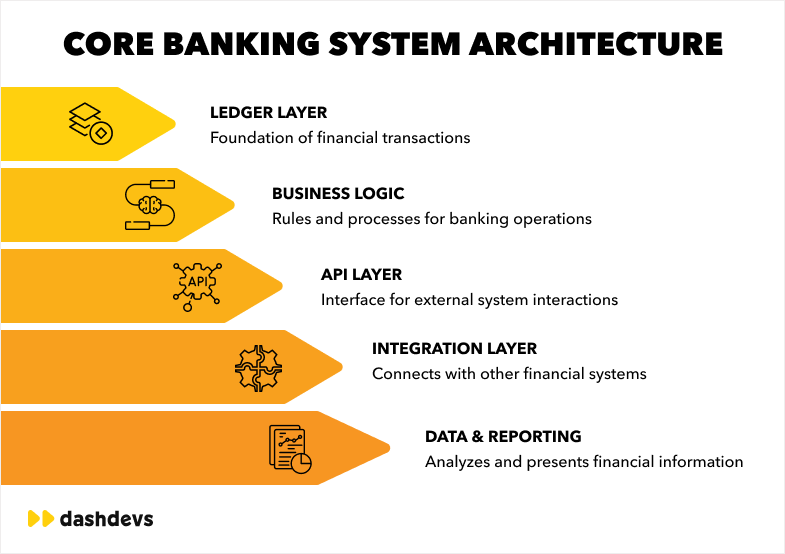

Core Banking System Architecture: A Technical Deep Dive

For CTOs, fintech architects, and technical decision-makers, understanding the layered structure of core banking system architecture is not optional — it is the basis of every infrastructure decision that follows. Architecture choices made at launch are extraordinarily expensive to reverse. Here is how modern core banking infrastructure breaks down:

Layer 1 — The Ledger Layer

The foundation of every core banking system is the ledger. This is where all financial state lives. A properly architected ledger layer implements double-entry bookkeeping at scale, maintaining debit/credit symmetry for every transaction. Balances are updated in real time — not batch-reconciled overnight. The ledger must be tamper-evident, auditable, and capable of handling millions of concurrent entries without integrity failures. In cloud based core banking systems, the ledger is event-sourced, meaning every state change is a recorded event, enabling complete auditability and replayability.

Layer 2 — The Business Logic Layer

This layer defines the rules governing financial products: how interest accrues, how fees are applied, how overdraft policies work, how product limits are enforced. In monolithic legacy systems, this logic is typically hardcoded — making product changes a months-long engineering effort. In modern, modular cores, this layer is configurable by product teams without engineering intervention. This distinction alone can mean the difference between launching a new loan product in three weeks or three quarters.

Layer 3 — The API Layer

The API layer is what makes the core connectable. A modern core banking solution technology stack exposes well-documented REST or event-driven APIs that enable integration with mobile apps, third-party providers, BaaS platforms, and partner systems. The quality, completeness, and uptime of the API layer is one of the most important differentiators between modern and legacy cores. Poor API design here cascades into product limitations across every downstream system.

Layer 4 — The Integration Layer

This is where the core connects to adjacent systems: CRM, AML/KYC engines, payment rails, card processors, and identity verification providers. The integration layer defines the operational perimeter of the core and determines how quickly new capabilities can be added. Well-designed integration layers use event-driven architecture and asynchronous messaging to prevent single points of failure. Poorly designed ones create brittle, synchronous dependencies that fail under load.

Layer 5 — The Data and Reporting Layer

The reporting layer handles compliance exports, regulatory submissions, analytics, and audit trail generation. For regulated institutions, this layer is not optional. Modern core banking systems provide real-time data pipelines; legacy systems produce reports through overnight batch processing, creating regulatory blind spots that become audit findings.

Legacy vs. Cloud Based Core Banking Systems

The shift from legacy on-premise cores to cloud based core banking systems is the defining infrastructure trend in financial services today. The SaaS-based segment alone is projected to grow from $13.20 billion in 2025 to $46.03 billion by 2032 at a CAGR of 19.5%, according to Fortune Business Insights — the fastest-growing deployment model in the market.

| Dimension | Legacy Core | Cloud-Based Core Banking System |

|---|---|---|

| Architecture | Monolithic, tightly coupled | Modular, loosely coupled microservices |

| Deployment | On-premise hardware | Cloud-hosted, multi-region by default |

| Processing | Overnight batch cycles | Real-time transaction processing |

| Product changes | Months of engineering work | Configurable in days or weeks |

| Scalability | Fixed capacity, expensive to scale | Auto-scaling on demand |

| Integration | Limited APIs, proprietary connectors | Open API-first, event-driven |

| Time to market | 18-36 months for new products | 3-6 months for new products |

| IT budget consumed | 70-78% on maintenance alone | Opex-based, pay-as-you-scale |

| Data security cost | Higher: legacy breach avg $6.08M (IBM 2024) | Lower: modern architecture + automated patching |

The operational implications are severe. Banks running outdated cores spend an average of 10 times more on operations compared to institutions using next-generation systems. A phased migration to a modern cloud-based platform has been shown to save 38% of costs within 18 months while enabling 62% faster time-to-market for new products.

Meanwhile, 43% of financial institutions still operate core systems built more than 20 years ago. Among US banks, 60% of those nearing their core provider contract renewal report dissatisfaction — yet only 20% ultimately make the switch, reflecting how deeply the fear of migration risk keeps institutions locked into underperforming infrastructure.

Fintech Core: A Third Path Between Buy and Build

When the conversation turns to what is core banking solution in practice, it almost always splits into two extremes: buy an off-the-shelf vendor core and accept its constraints, or build a fully custom core from scratch and absorb the cost and timeline. Both paths have serious trade-offs. A third path exists.

Fintech Core, developed by DashDevs, is a modular, API-first orchestration layer built to power digital banks, EMIs, and embedded finance products without forcing teams into monolithic vendor lock-in. It is not a UI layer. It is not simply a payment gateway. And it is not a rigid legacy core replacement.

It is a composable core banking solution technology framework that enables:

- Ledger orchestration without rebuilding the ledger from scratch

- Product configuration without hardcoding business logic

- Integration with BaaS providers while preserving product control

- Payment rails connectivity across multiple jurisdictions

- KYC/AML automation embedded directly into core onboarding flows

- Compliance-ready workflows with built-in audit trail generation

In terms of core banking system architecture, Fintech Core operates across multiple layers simultaneously: it integrates with underlying ledger engines or sponsor banks while maintaining transaction integrity, exposes all services through RESTful APIs, and connects to KYC providers, card schemes, AML vendors, and CRM systems through clean integration adapters. For institutions that want to explore the broader vendor landscape, DashDevs’s Top 10 Core Banking Solutions guide provides a structured comparison of leading platforms by architecture type, deployment model, API capabilities, and licensing flexibility.

Fintech Core is not for companies choosing between build and buy. It’s for companies who have realized that neither extreme serves their actual product and compliance requirements — and need an orchestration layer that gives them both speed and control.

This matters particularly for fintechs operating under BaaS arrangements. Your core banking solution technology must align with your BaaS partner’s architecture — otherwise you will encounter scalability bottlenecks the moment your transaction volume scales. Fintech Core was explicitly designed to sit above BaaS providers while preserving product control and regulatory auditability. For a full analysis of how to evaluate BaaS partners in relation to your core infrastructure, see DashDevs’s BaaS Provider Selection Checklist.

The comparison table below illustrates how Fintech Core compares to the two conventional options:

| Criteria | Fintech Core (White-Label) | Custom Build | SaaS Vendor |

|---|---|---|---|

| Price | $$ | $$$$$ | $-$$$$ |

| Time to Market | ~3 months | 12+ months | ~6 months |

| Customization | High + source code access | Full control | Limited |

| Vendor Lock-in | None | None | High |

| IP Ownership | Yes (with licensing) | Full | No |

| Regulatory Compliance | Out-of-the-box | Must be built in | Varies by vendor |

| Scalability | Highly scalable | Scalable | Limited |

| Pre-built Integrations | Yes (KYC, AML, payments, cards) | None | Limited choice |

How Core Banking Connects to BaaS — A Critical Strategic Distinction

One of the most persistent sources of confusion in the fintech ecosystem is the relationship between what is core banking and what is Banking-as-a-Service. Most content treats them as separate topics. They are not — and understanding how they connect is essential for any founder or CTO scoping their infrastructure stack.

The relationships between the key entities in a BaaS-enabled stack look like this:

- The licensed bank or EMI holds the regulatory license and owns — or directly operates — the core banking system.

- The BaaS provider exposes API access to banking capabilities, often sitting on top of or connected to a core.

- The fintech or startup consumes those APIs to deliver banking experiences to end customers without holding their own license.

The critical insight: when you choose a BaaS partner, you are — by extension — making a decision about the core banking system architecture that underpins your product. If that core has batch-processing limitations, your product inherits them. If it lacks modular product configuration, your growth is constrained by it.

Choosing a BaaS provider is not just a vendor decision. It is an architecture decision that will shape your product roadmap for years. Evaluate it accordingly.

Core Banking in Practice: DashDevs Implementation Examples

Understanding what is core banking solution in the abstract is useful. Seeing it implemented across real products is more useful. Here is how DashDevs has applied core banking engineering principles across multiple real-world builds, each illustrating a distinct architectural decision.

DashDevs engineered a compliance-first digital banking platform for the Saudi Arabian market, built on custom core orchestration: API-first backend architecture, real-time ledger management, and regulatory-ready reporting. The platform was designed to support product configuration without backend engineering changes — a critical requirement for launch velocity in a heavily regulated jurisdiction.

The Nexus Platform was designed as reusable, modular infrastructure for building digital banks faster. By standardizing core components — account management, ledger, API gateway, integration adapters — the platform allows new bank builds to inherit production-tested architecture rather than rebuilding from scratch. Every new digital bank built on Nexus starts ahead of where a greenfield build would begin.

This UK-based challenger bank project — one of the UK’s first neobanks — required core banking system architecture that integrated cleanly with the UK’s EMI regulatory framework. The work illustrated a key architectural reality: regulatory compliance is not a feature you add to a core bank system. It must be embedded in the data model and reporting layer from day one. Retrofitting compliance onto a core not designed for it is one of the most common — and most expensive — mistakes in fintech engineering.

An ESG-focused fintech product where sustainability metrics were integrated directly into the financial processing layer. Core banking logic extended beyond balances and transactions — incorporating carbon tracking and ESG product behaviour into how the core bank system processed and recorded financial activity. This is programmable core banking at its clearest: a demonstration of what becomes possible when the business logic layer is genuinely configurable rather than hardcoded.

The award-winning MuchBetter project demonstrated how wallet infrastructure can be cleanly layered over core logic, maintaining separation between the customer-facing product experience and the underlying ledger and transaction processing systems. This architecture allows the product layer to iterate rapidly while the financial backbone remains stable and auditable.

A financial operations tool layered on top of core infrastructure to automate invoice processing, vendor payments, and cash flow optimization for SMEs. This project demonstrates how core banking services power adjacent financial products well beyond consumer banking. The accounts payable layer consumed real-time ledger data and transaction APIs directly — illustrating how a well-designed core bank system becomes an enabler for an entire ecosystem of financial products.

Core banking without identity is incomplete. This engine orchestrates KYC providers, risk scoring, compliance workflows, and account approval triggers — including integration with identity verification providers like Veriff — directly into core onboarding flows. By embedding identity automation at the core layer rather than treating it as a frontend afterthought, onboarding becomes both compliant and scalable. The result is automated, auditable identity verification that feeds directly into account opening workflows.

When Do You Actually Need a Core Banking Solution?

Not every fintech needs a full core banking implementation. The decision depends on your regulatory position, your product scope, and whether you are holding customer funds under your own license.

You need a core banking system if:

- You are launching a licensed bank or EMI

- You issue IBANs or hold deposits in your own name

- You manage customer funds on your own balance sheet

- You need real-time reconciliation across a high volume of accounts

- You are operating in multiple jurisdictions with distinct reporting requirements

You may not need a full core if:

- You are embedding payments into an existing product through a BaaS provider

- You are operating entirely under a sponsor bank’s license and infrastructure

- Your financial product scope is narrow enough to be served by a specialized ledger solution

The strategic question is not ‘do we need a core?’ It is ‘what level of core ownership and control do we need to achieve our regulatory and product objectives?’ Those are very different questions with very different cost implications.

Build vs. Buy vs. Orchestrate a Core Banking Solution

This is the decision that defines a fintech’s cost structure and product velocity for years. There is no universally correct answer — but there is a framework for reaching the right one.

Option 1: Build a Custom Core

Building a proprietary core gives you complete architectural control and eliminates vendor dependency. It also requires a world-class engineering team, 18 to 36 months of focused development, and significant ongoing investment. Full core transformation programmes typically cost between $20 million and $100 million over three to five years depending on institution size — a commitment that only makes sense when your business model requires capabilities that no vendor can deliver.

Option 2: Buy a Vendor Core

Commercial core banking platforms — Temenos, Mambu, Thought Machine, Finastra — have become significantly more capable over the past decade. Cloud-native vendor cores can now deliver 80 to 90% of what most digital banks need, with faster time to market than a custom build. The trade-offs are vendor dependency, licensing costs, and the risk that your vendor’s roadmap diverges from your product requirements. For most early-stage and growth-stage digital banks, this is the right starting point.

Option 3: Orchestrate a Hybrid Architecture (Fintech Core Model)

The orchestration model is how the most sophisticated fintechs are approaching core banking today. Rather than choosing between building everything or buying everything, you compose: a vendor core or ledger engine for the financial backbone, custom-built services for differentiating product logic, and an orchestration layer connecting them. This approach delivers the scalability of a modern vendor core, the flexibility of custom logic, and the compliance structure of a production-tested ledger. Fintech Core from DashDevs is a practical implementation of this composable architecture — allowing institutions to launch in approximately 3 months at a fraction of the cost of a full custom build, without the lock-in of a rigid SaaS vendor.

What Makes a Modern Core Banking Solution Future-Proof?

The core banking solution technology that will define the next decade shares a specific set of architectural characteristics. Evaluating vendors or scoping a build against these criteria is a strategic exercise with long-term financial consequences.

- API-first by design — every capability exposed through documented, versioned APIs

- Event-driven architecture — real-time data propagation, not batch synchronization

- Real-time ledger — no overnight batch windows, no stale balances, no reconciliation lag

- Modular product configuration — new financial products without engineering releases

- Cloud-native infrastructure — elastic scaling, multi-region availability, zero-downtime deployments

- Embedded compliance — audit trails, regulatory reporting, and data residency in the data model

- Open integration standards — no proprietary connectors, clean separation between core and adjacent systems

The market data underlines this direction: banks that have moved to modern payment platforms see a 42% increase in payments-related revenue and can launch products 90% faster than those constrained by legacy infrastructure.

The cores winning in 2025 are not just software systems. They are platforms for financial product innovation. The ones that will define 2030 are those that have embedded compliance automation and AI-driven operations as native capabilities — not afterthoughts bolted onto a legacy core.

How to Choose the Right Core Banking Solution: A Strategic Checklist

Vendor selection for a core banking system is not like buying SaaS tools. The decision has a multi-year implementation horizon and significant switching costs. DashDevs’s Top 10 Core Banking Solutions guide provides a structured vendor comparison across architecture type, deployment model, API capabilities, and licensing flexibility. Here are the criteria that actually matter in your evaluation:

- License type — does the vendor have proven experience supporting your specific regulatory framework (EMI, full bank, broker-dealer)?

- Geography — does the core banking solution support multi-currency, multi-jurisdiction operation and the specific reporting standards of your target markets?

- Product complexity — can the system support your specific loan structures, account types, and interest models without heavy customization?

- Scalability — what is the proven transaction volume ceiling, and how does the architecture handle 10x growth?

- Cost model — is pricing based on accounts, transactions, or a flat platform fee? How does the economics change at scale?

- Compliance framework — what is the out-of-the-box compliance capability, and what requires custom development?

- Vendor roadmap — where is the vendor investing product development? Does it align with where your product is heading in three years?

- Data ownership — who owns your customer and transaction data? What are the portability terms if you migrate?

Future of Core Banking Technology: Outlook and Predictions for 2026 and Beyond

The core banking industry is not just growing — it is being structurally redefined. The platforms considered cutting-edge in 2020 are already showing their limitations. Here is where the industry is heading, and what it means for strategic decisions being made right now.

1. Composable Banking Becomes the Dominant Architecture

The era of monolithic cores — even cloud-native ones — is giving way to composable core banking solution technology. Rather than one vendor owning the entire stack, banks and fintechs are assembling best-of-breed components: a ledger from one vendor, a loan engine from another, payment rails from a third, and a custom orchestration layer connecting them. 10x Banking’s 2024 study found that 55% of institutions cannot support real-time payments due to legacy limitations, directly forfeiting an estimated $8 trillion in projected 2025 instant payment volume. By 2027, composable banking architecture is expected to be the standard approach for any institution launching a greenfield digital bank.

2. AI-Driven Reconciliation and Compliance Automation

Reconciliation is currently one of the most labor-intensive operations in banking. AI-driven engines are beginning to automate exception detection, pattern identification, and resolution at scale. Similarly, regulatory reporting is moving from manual compilation to automated near-real-time submissions. Institutions that have invested in modern core banking system architecture — with clean data models and real-time event streams — will implement these capabilities significantly faster than those still on batch systems. Notably, banks that have modernized report a 40% reduction in operational costs and 60% acceleration in new product launches within two to three years of migration.

3. Embedded Finance Deepens the API Requirement

As embedded finance matures — banking products surfacing inside non-banking applications — the API layer of the core banking solution becomes increasingly critical. The market data is unambiguous: 76% of banking customers now prefer digital-first services, and 70% of financial institutions cite security and compliance improvements as a key reason for switching to modern platforms. The institutions that can offer clean, well-documented, high-uptime APIs will capture the embedded finance opportunity. Those with fragile integration layers will be systematically excluded from it.

4. Real-Time Payment Rails Raise the Baseline

The global expansion of real-time payment infrastructure — UK Faster Payments, SEPA Instant in Europe, India’s UPI, and the ongoing ISO 20022 migration — is making batch-processing cores structurally incompatible with market expectations. The Financial Brand’s 2025 Retail Banking Trends report found that 62% of banks planned to offer real-time payments in 2025, up from 49% in 2024 — a gap that represents direct product inferiority for institutions still on legacy batch infrastructure. By 2030, real-time ledger capability will be a baseline requirement, not a premium feature.

5. Ledger-as-a-Service Emerges as a Distinct Infrastructure Category

One of the most significant structural shifts underway is the emergence of ledger-as-a-service as a standalone infrastructure category. Rather than bundling ledger capabilities inside a monolithic core, specialized ledger providers are offering best-in-class double-entry bookkeeping as a service — consumed by banks, fintechs, and embedded finance providers alike through clean APIs. This unbundling mirrors what happened to payment processing in the 2010s. Institutions that recognize this shift early will build faster, at lower cost, and with greater architectural flexibility than those locked into monolithic vendors.

6. Regulatory Technology Converges with Core Banking

RegTech has historically operated as a separate layer — compliance tools sitting alongside the core and pulling data from it. The next evolution is the convergence of regulatory capability directly into the core data model. Financial sector data breaches now cost an average of $6.08 million per incident — 28% higher than the cross-industry average — creating overwhelming pressure to embed security and compliance natively rather than as an add-on. The global core banking market’s projected growth to $64.96 billion by 2032 is driven in no small part by this regulatory convergence pressure.

Strategic Implication: Core Is Operating Model, Not Just Infrastructure

The most important reframe for financial services leaders is this: core banking is not an infrastructure decision delegated to the CTO. It is a strategic decision that belongs in the boardroom. Your core banking system architecture determines the speed at which you bring new products to market, the unit economics of your operations, the jurisdictions you can serve, and the partners you can connect to. Get it right, and your core becomes a compounding asset. Get it wrong, and it becomes the constraint that limits every other ambition in the business.

The fintechs and banks that will define the next decade are not those with the biggest budgets. They are those who made the right core banking architecture decisions in 2024 and 2025 — when the choices were still affordable and the switching costs were still manageable.

Conclusion — Core Banking Is Strategy, Not Just Software

The definition of core banking matters far less than the architecture decisions it forces. What is core banking, ultimately? It is the foundational decision that defines your regulatory posture, your product velocity, your margin structure, and your ability to compete in a market moving faster than ever before. The global core banking software market is growing at 18.6% CAGR — not because banks are upgrading for the sake of it, but because the cost of delay has become quantifiable and visible in every income statement.

The question is not whether to modernize. It is whether to build, buy, or orchestrate — and whether you have the architecture and engineering expertise to execute the decision correctly. DashDevs has delivered core banking implementations for digital banks, EMIs, e-wallet providers, and fintech platforms across multiple jurisdictions.

Explore Fintech Core, review our case studies, or talk to our fintech architects to assess your core readiness.

Share article